To quickly access the page content, please click on the links below.

News Update

- California transportation data shows a decline. According to a 24 January data released by Federal Highway Administration, vehicle miles traveled across California’s rural and urban roads during the period of November 2021 has lagged behind the 2019 levels by 14pc. California's transportation fuel demand indicators have dropped, while the US overall closes in on or exceeds 2019 levels. Total US vehicle miles traveled in November surpassed 2019 levels by 2.8pc. CARBOB continued as the major generator of state Low Carbon Fuel Standard (LCFS) deficits in the first half of 2021. The slow recovery in California transportation demand helped low-carbon fuel credits to exceed deficits that resulted to lower credit prices in 2021. Oregon has recorded a comparatively quicker recovery in demand. November vehicle miles traveled in Oregon exceeded 2019 miles by 1pc. In Washington, total miles fell short of November 2019 levels by 2pc.

- California LCFS grid carbon to increase. The California Air Resources Board (CARB) proposed a 1.1pc to 76.6g CO2 per megajoule increase for the 2022 carbon intensity of average grid electricity used as a transportation fuel. Mounting residual oil and natural gas generation required to offset sinking hydroelectric capacity lifted the average grid carbon intensity. California has set targets for zero-emission vehicle (ZEV) adoption, including a goal that ZEVs make up all-new, in-state passenger vehicle sales by 2035. Most of California’s electric vehicle charging uses the CARB average score to calculate credits, the higher carbon intensity would lessen the volume of credits that vehicle charging can generate. Public comment on the proposed carbon intensity increase will continue to 11 March.

- California LCFS bank increases. California Low Carbon Fuel Standard (LCFS) credit generation outperformed deficits for a second consecutive quarter, making the largest increase in total program credits since 2016. According to data by the California Air Resources Board (CARB), the cumulative bank of LCFS credits increased in the third quarter of 2021 by 5.5pc to 8.4mn metric tons. Deficits associated with higher-carbon fuels increased by 6.6pc from the previous quarter, to 5.1mn t, but third-quarter credit generation rose by 11.4pc to 5.5mn t. Deficits associated with CARBOB increased by 4.5pc from the previous quarter and remained the largest source of all deficits under the program. Bio-CNG generated 31pc more credits than the previous quarter to account for 15pc of all credits generated in the third quarter. Renewable diesel-generated 16pc more credits than the previous quarter. Electric vehicle charging also rose, with total credits for all charging sources higher by 8.9pc to about 21pc of all credits generated during the quarter.

- LCFS trade volume for January sets a record. The California Low Carbon Fuel Standard (LCFS) total credits transferred for January 2022 rose to 3.4mn t, a 5pc increase from the previous month and a 56pc increase from January 2021, according to the California Air Resources Board. The trade volume for the period is higher by more than half compared to the previous year.

- Gevo commences startup of Iowa RNG project. US renewable fuels producer Gevo has started its dairy manure-based renewable natural gas (RNG) project in northwest Iowa called Gevo NW Iowa RNG. It is expected to produce 355,000 mmBtu of RNG per year. The produced RNG will be sold into California under agreements BP has in place with Clean Energy Fuels. The project is expected to generate between $9mn-16mn/yr beginning in late 2022 or early 2023.

- California utility sells 170K LCFS credits. California utility Pacific Gas & Electric (PG&E) on 7 February offered for sale its largest volume of Low Carbon Fuel Standard (LCFS) credits. The offering of about 170,000 credits is the utility's largest since December 2019. PG&E accepted offers until 1 pm ET on 8 February. The company keeps auction results private.

- Oregon commences to more aggressive CFP targets. Stakeholders on 27 January supported tougher cuts to the carbon intensity of Oregon's transportation fuels, as regulators continue working on extending its Clean Fuels Program (CFP) over the next 15 years. The rulemaking advisory committee assisting regulators to develop new low-carbon fuel standard targets for 2025 and beyond provided no formal recommendation yet. But a majority of the participants in the meeting favored more aggressive scenarios that would begin lowering the surplus of the state's low-carbon fuel standard (LCFS) credits no later than 2030. The rulemaking will be guided by the advisory committee and public comment later this winter. Staff plan to propose a rule this summer ahead of board consideration in September. Committee members will meet again on 31 March.

- Oregon CFP credits fell in 3Q. According to data released on 9 February by the Department of Environmental Quality, the cumulative bank of credits used to comply with Oregon's low-carbon fuel standard decreased by 7.8pc to about 679,000 metric tons during third quarter of 2021. Increasing gasoline demand and decreasing renewable diesel use helped draw down the bank of Oregon Clean Fuel Program (CFP) credits during the quarter. The state generated about 376,000 t of credits in 3Q 2021— 7.7pc lower than the previous quarter but an 18pc increase from 3Q 2020. Deficits rose by 5.7pc from the previous quarter and by 22pc from the same quarter of 2020, to about 434,000 t.

- Oregon CFP transfers for January set a record. Oregon's Department of Environmental Quality reported that about 186,000 metric tons of credits were transferred over 27 transactions for January 2022. Credit transfers for the period were the highest for any January since its inception in 2016.

- Washington state is in its final stage on fuel CI scoring. According to a staff statement on 27 January, the Washington Department of Ecology is on its last stage of signing an agreement for lifecycle analysis models that will support the state’s Clean Fuels Program (CFP). The agency is planning to discuss the model with stakeholders at a meeting in mid-March. Lifecycle analyses determine the carbon intensity of a specified fuel supplied to the state and also how the fuel was transported. The models support determinations of how many deficits or credits a given fuel would incur.

- New Mexico LCFS in House hearing. Members of the New Mexico state House of Representatives debated a proposed Clean Fuel Standard. The House Government, Elections & Indian Affairs Committee took public comment and began debate on 15 February. The New Mexico LCFS proposal that passed out of the Senate would require reducing the carbon intensity of New Mexico transportation fuels from 2018 levels by at least 20pc by 2030 and by at least 30pc by 2040. Governor Michelle Lujan Grisham supports the bill. Utilities and business groups supported the proposal in a public comment before the committee. Biofuels groups, urged passage of a program that would cut carbon intensity and entice green business investment in the state. Farm and ranch and oil and gas groups cautioned against higher fuel charges. Some environmental groups also opposed the bill, protesting the inclusion of carbon capture technology and the use of markets to reduce emissions.

Schedule

- April 1, 2022: California LCFS 4Q 2021 reporting deadline

- April 29, 2022: California LCFS 4Q 2021 data release

- June 30, 2022: California LCFS 1Q 2022 reporting deadline

- July 29, 2022: California LCFS 1Q 2022 data release

- September 20, 2022: California LCFS 2Q 2022 reporting deadline

LCFS Credit Pricing

- Credits Price as of February 22nd, 2022:

- California - Spot Delivery $00

- Oregon - Spot Delivery $ 126.50

LCFS Credit Transfer Activity for California

|

Time

|

Transfers

|

Total Volume

|

Avg $/credit

|

|

Jan -22

|

358

|

3,389,000

|

$ 167

|

|

Dec -21

|

269

|

3,217,000

|

$ 172

|

|

Nov -21

|

128

|

1,125,000

|

$ 174

|

|

Oct -21

|

434

|

3,782,000

|

$ 182

|

|

Sept -21

|

136

|

1,518,000

|

$ 183

|

|

Aug -21

|

100

|

709,000

|

$ 185

|

|

July -21

|

252

|

2,125,000

|

$ 188

|

|

June -21

|

190

|

1,873,000

|

$ 190

|

|

May -21

|

81

|

791,000

|

$ 190

|

|

Apr -21

|

345

|

3,455,000

|

$ 192

|

|

Mar-21

|

307

|

3,490,000

|

$ 198

|

|

Feb-21

|

87

|

1,019,000

|

$ 197

|

|

Jan-21

|

335

|

2,176,000

|

$ 199

|

|

Dec-20

|

260

|

2,997,000

|

$ 199

|

|

Nov-20

|

133

|

1,207,000

|

$ 196

|

|

Oct-20

|

336

|

2,237,000

|

$ 198

|

|

Sept -20

|

167

|

1,553,000

|

$ 196

|

|

Aug-20

|

111

|

857,000

|

$ 196

|

|

Jul-20

|

334

|

2,509,000

|

$ 199

|

|

June-20

|

129

|

1,059,000

|

$ 202

|

|

May-20

|

90

|

470,000

|

$ 195

|

|

Apr-20

|

344

|

4,098,000

|

$ 198

|

|

Mar-20

|

233

|

2,312,000

|

$ 199

|

|

Feb-20

|

84

|

581,000

|

$ 206

|

|

Jan-20

|

240

|

1,895,000

|

$ 200

|

|

Dec-19

|

217

|

2,216,000

|

$ 197

|

|

Nov-19

|

88

|

705,000

|

$ 195

|

|

Oct-19

|

243

|

1,990,000

|

$ 195

|

|

Sep-19

|

137

|

1,179,000

|

$ 195

|

|

Aug-19

|

89

|

929,000

|

$ 194

|

|

Jul-19

|

188

|

1,574,000

|

$ 193

|

|

Jun-19

|

114

|

875,000

|

$ 190

|

|

May-19

|

76

|

408,000

|

$ 185

|

|

Apr-19

|

131

|

1,299,000

|

$ 180

|

|

Q1 2019

|

373

|

2,972,000

|

$ 188

|

|

CY 2018

|

1725

|

13,334,000

|

$ 160

|

|

CY 2017

|

1226

|

8,875,000

|

$ 89

|

|

CY 2016

|

929

|

5,343,000

|

$ 101

|

|

CY 2015

|

578

|

2,852,000

|

$ 62

|

|

CY 2014

|

304

|

1,667,000

|

$ 31

|

|

CY 2013

|

202

|

887,000

|

$ 55

|

|

CY 2012

|

24

|

164,000

|

$ 17

|

LCFS Cost for Gasoline and Diesel

- Cost as of February 22nd, 2022 for Vintage 2022

- California

- Carbob (No Cl ethanol)- Vintage 2022 17.17 cents per USG

- Carbob (79.9 Cl ethanol)- Vintage 2022 16.07 cents per USG

- Oregon

- E10 gasoline- Vintage 2022 7.35 cents per USG

- B5 diesel – Vintage 2022 8.36 cents per USG

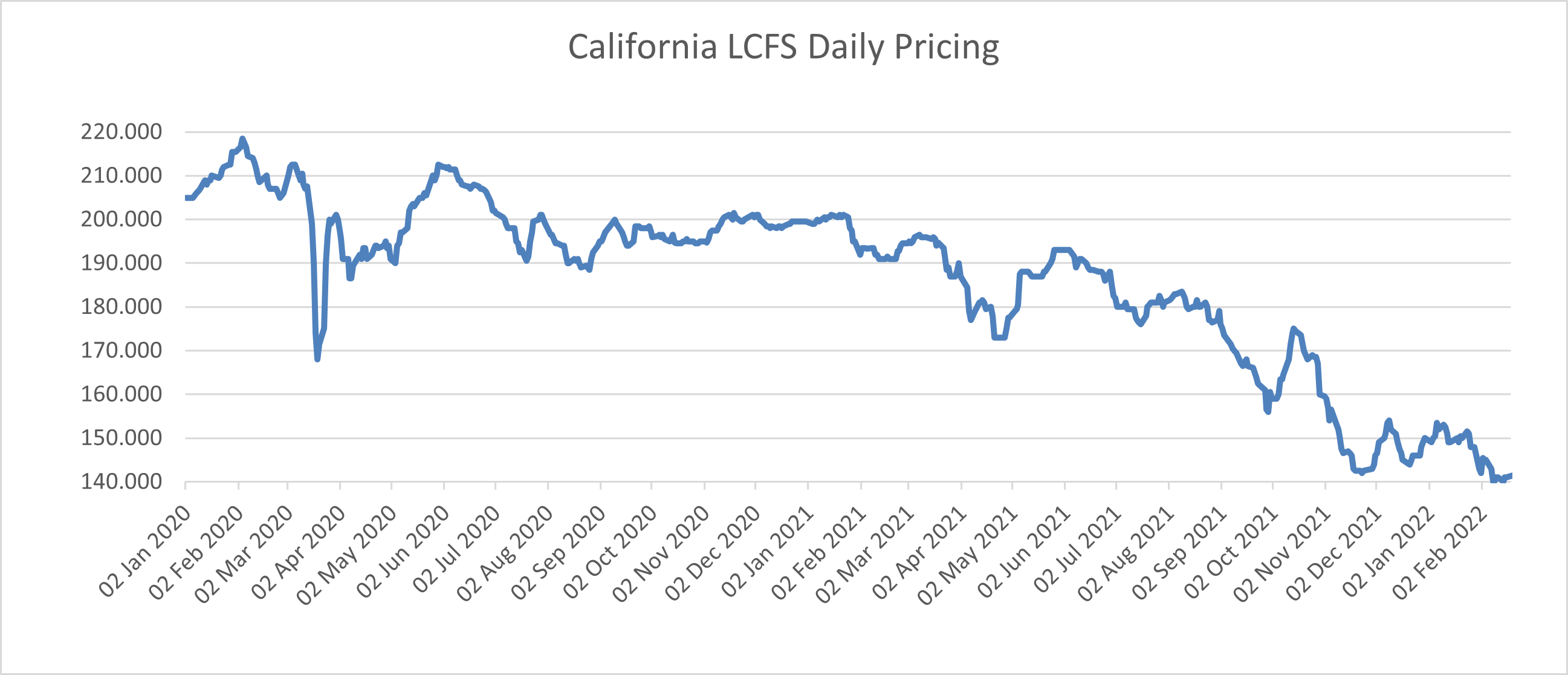

Figure 1. California LCFS USD/t Jan. 2020 - Present

|

2021 Average Daily Price: $176.53 2022 Average Daily Price: $146.97

2021 Highest Daily Price: $201.00 2022 Highest Daily Price: $152.50 |

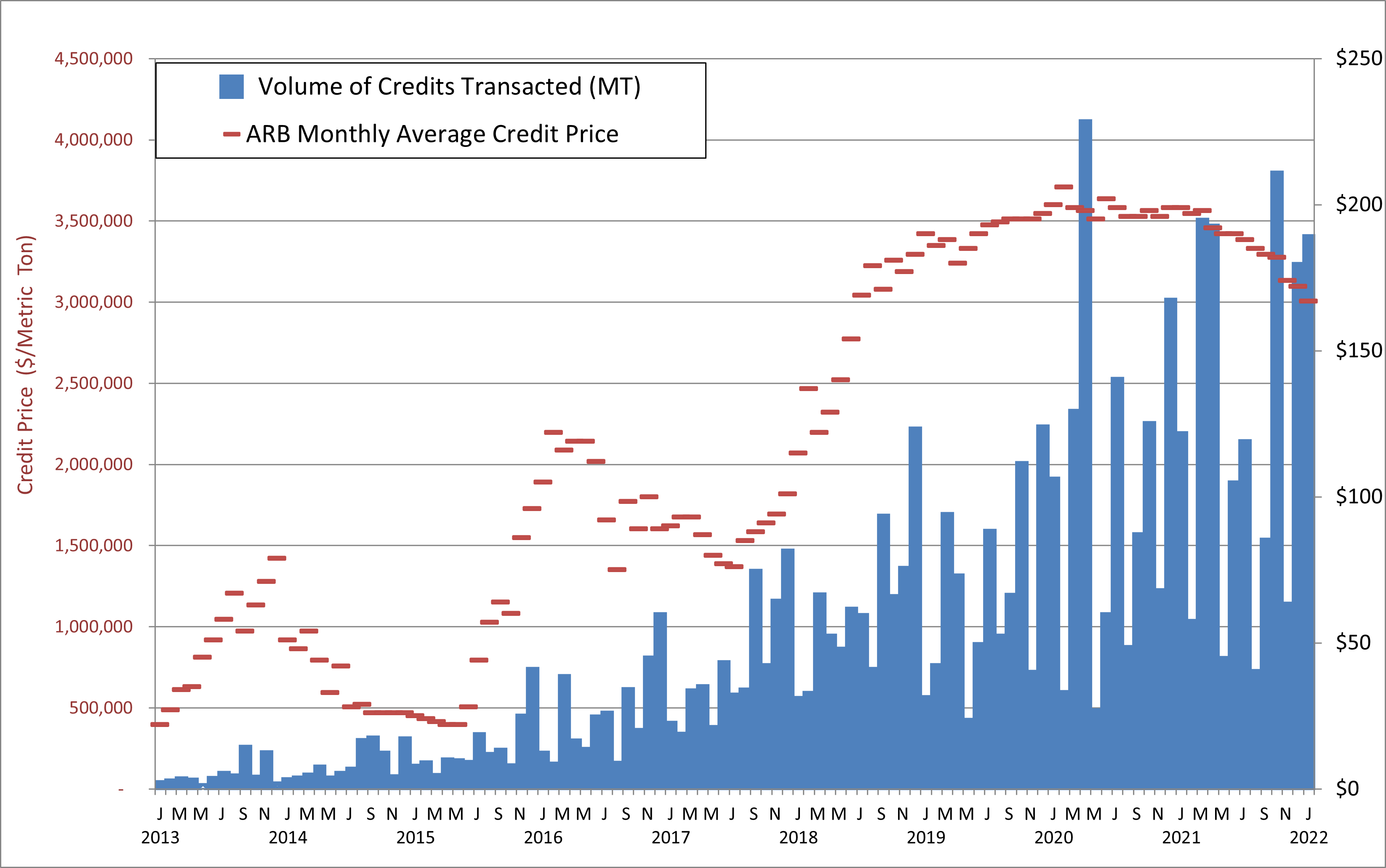

Figure 2. California Monthly LCFS Credit Price and Transaction Volume as Reported by ARB

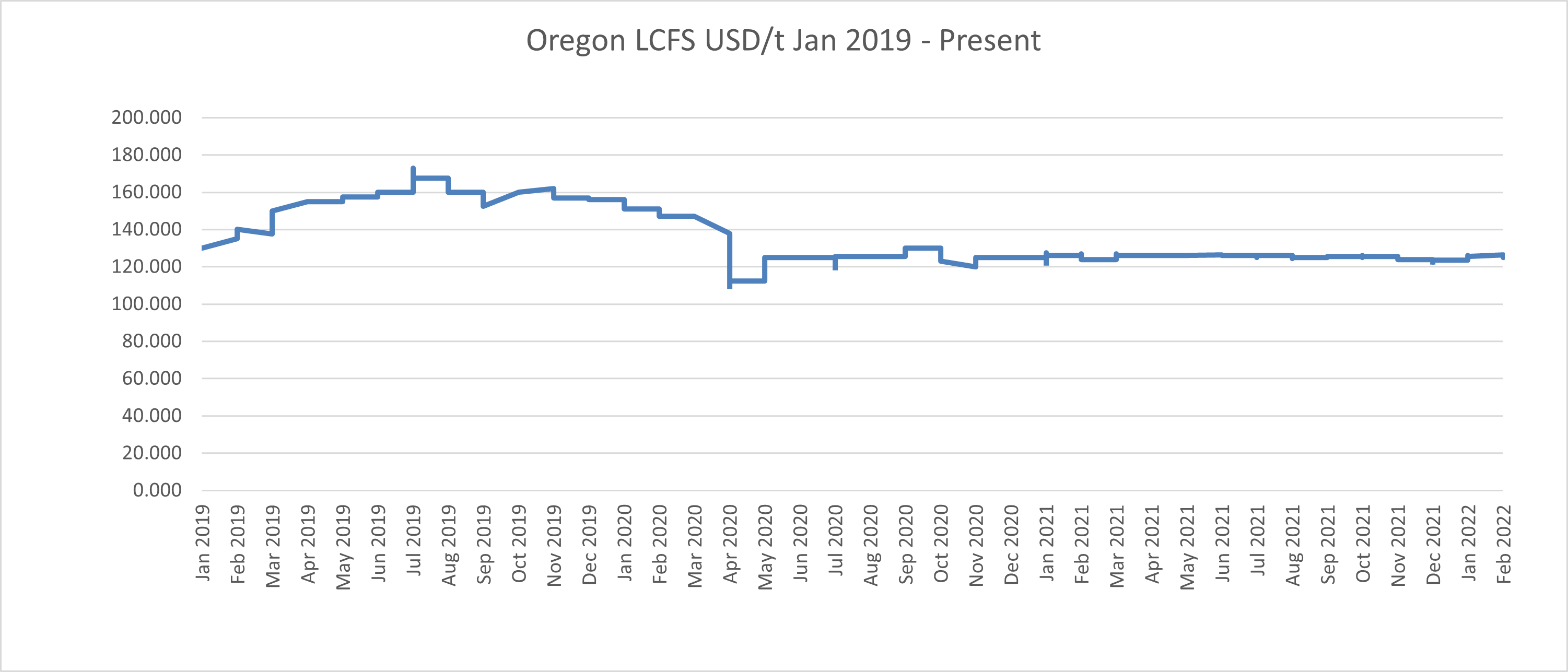

Figure 3. Oregon LCFS USD/t Jan. 2019 – Present

|

|

2021 Average Daily Price: $125.56 2022 Average Daily Price: $124.98

2021 Highest Daily Price: $127.50 2022 Highest Daily Price: $126.50

|

Questions? Contact our team for more information: environmental@aegis-hedging.com

CONFIDENTIAL – UNAUTHORIZED THIRD-PARTY DISTRIBUTION PROHIBITED

EACH CLIENT MUST RELY ON ITS OWN EVALUATION OF THE SUBJECT MATTER PRESENTED IN THIS DOCUMENT. THIS DOCUMENT IS NOT TO BE CONSTRUED AS INVESTMENT, LEGAL, OR TAX ADVICE OF ANY KIND.