To quickly access the page content, please click on the links below:

News Update

- California seeks LCFS balances from 5 companies. According to the California Air Resources Board (CARB), five companies - Ag Environmental Products LLC, American Biodiesel, Biodico Westside, Mutual Propane, and Sun Valley Energy - ended the compliance year without retiring enough credits to meet their 2021 California Low Carbon Fuel Standard (LCFS) obligations by about 1,600 credits combined. As a result, the government will hold a credit clearance market to allow corporations to purchase credits to make up the difference. Between 1 June and 31 July, the enterprises must make arrangements to satisfy their obligations from a pool of more than 24,000 credits given by nine participants.

- Gasoline sales in California increased in February, but trailing behind 2019. According to the most recent state tax data, gasoline sales in California increased in February but fell short of pre-coronavirus levels. The state recorded fuel taxes on around 908,000 b/d of gasoline for the month, an 11% increase from January and a 10% increase from February 2021. However, the volume remained 7 percent lower than the same month in 2019, the previous year before the Covid-19 virus struck, affecting travel and business and lowering fuel demand. CARBOB accounts for roughly 80% of all shortfalls under California's Low Carbon Fuel Standard (LCFS). Gasoline usage creates demand for credits that fuel suppliers must employ to offset the distribution of higher-carbon fuels.

- Phillips 66 was sued over biofuel trade data. A renewable fuels retailer in California has accused US refiner Phillips 66 of stealing trade secrets in order to boost its biofuels business. Phillips 66 allegedly engaged in acquisition talks with renewable fuel retailer Propel Fuels in 2017, collecting confidential knowledge on the smaller company's low-carbon fuel retail network, according to a lawsuit filed on March 22. Propel said in a lawsuit filed in Alameda County Superior Court in northern California that Phillips 66 abandoned the agreement talks and exploited the data to grow its own renewable fuels company in California. After engaging in merger talks with Propel in 2017, the refiner allegedly demanded access to Propel's proprietary models in order to explore locations for its own network of renewable fuels locations. Propel claims it first refused these requests but relented when Phillips 66 executives assured it that the refiner would not launch a renewable fuels venture without its participation. According to the lawsuit, Propel submitted data suggesting which Phillips 66 retail stations in California would be best positioned to offer renewable diesel and E85 — gasoline containing up to 85 percent ethanol — and the refiner quickly backed out of the arrangement. Phillips 66 refuted Propel's charges, saying it is one of several companies introducing renewable fuels into California's expanding market.

- Vehicle miles in California continue to rise. According to the Federal Highway Administration, vehicle miles driven on California highways exceeded pre-pandemic levels for the second consecutive month in March. Total mileage in the state increased by 2.5 percent to 28.9 billion miles in March, compared to the same month in 2019. The increase followed February mileage in the state exceeding 2019 levels by 6.2 percent. Mileage has increased faster than the state's anticipated CARBOB demand. Taxable gasoline sales for February, which were also announced this week, were 7 percent lower than in 2019. California has set strong targets for the uptake of electric vehicles. In 2021, battery, fuel cell, and plug-in hybrid vehicles accounted for approximately 2.8 percent of all light duty vehicles in the state.

- Drought may cause California CO2 levels to rise. According to an Energy Information Administration (EIA) supplemental report on electrical supply in California released this summer, falling lake levels in key reservoirs impair the state's ability to dispatch low-emission, complementary power to its growing portfolio of solar and wind energy. According to the administration, present drought circumstances might reduce hydroelectric supply by nearly half, from 15% to 8% of summer electricity generation. California may need to increase in-state and imported natural gas generation to meet half of its summer electric power needs, which would increase carbon dioxide emissions by 8%. Rising participation in an alternative Western power marketplace could help compensate for the loss. In 2019, California's power supply accounted for 14 percent of statewide greenhouse gas emissions and is subject to the state's cap and trade regulations. The carbon intensity of the electric supply also influences the credits generated by electric vehicle charging under the state's Low Carbon Fuel Standard (LCFS).

- PG&E plans to achieve carbon neutrality by 2040. Pacific Gas & Electric (PG&E) of California intends to achieve carbon neutrality by 2040 through investments in pipeline infrastructure, electric vehicle charging, and natural gas switching. The state's largest utility declared on June 8 that it would reach carbon neutrality five years sooner than the state's 2045 target. PG&E projected to supply 70 percent of RPS-eligible electricity by 2030, above its 60 percent mandate, and to meet 15 percent of its core natural gas demand with renewable natural gas (RNG). RNG also operates gas filling stations, generating a significant amount of state Low Carbon Gasoline Standard (LCFS) credits in comparison to the fuel supplied. To reduce customer use of higher-carbon sources, the company planned to "prepare the grid" for 12,000 GWh of electric vehicle charging load and transfer larger, more difficult-to-electrify customers to natural gas. To reduce the cost of such vehicles, PG&E's electrification approach would include allowing 2 million electric vehicles to join in making their batteries available as flexible load across the grid.

- Carmakers said California's standards are overly aggressive. Automakers have cautioned that they may struggle to reach higher electric vehicle supply targets proposed by California for the 2026 model year. Delivering on requirements that zero-emissions vehicles account for 35 percent of all new vehicle sales in the state in 2026 and 100 percent in 2035 would be extremely difficult, the Alliance for Automotive Innovation and other groups warned at a public hearing on the Advanced Clean Cars II rule on June 9. Regulations may be impossible to implement in another 17 states, including New York, Pennsylvania, and New Jersey, where governments have embraced California's criteria but residents have yet to adopt the required number of electric vehicles. Meanwhile, supporters urged the California Air Resources Board (CARB) to establish even harder standards, such as reaching 100 percent new sales by 2030. The Advanced Clean Cars II rule expands on regulations enacted a decade ago that required increasing supplies of low- and zero-emission vehicles between 2015 and 2025. The upgrade being considered this year would extend the restrictions with new, strong targets for ZEV sales to meet 100 percent of all new car sales by 2035. The proposed laws would also establish separate, stricter tailpipe emissions limits for the remaining internal combustion engine vehicles. Automakers can now average their fleet emissions by integrating ZEV vehicles.

- Volume of California LCFS transfers decreases in May. According to the California Air Resources Board, credit transfers under the California Low Carbon Fuel Standard (LCFS) exceeded year-ago levels in May, a generally low-volume month (CARB). CARB recorded around 861,000 metric tons of credits over 119 transactions in May, which was 9 percent and 47 percent more than the same month in 2021, respectively. Credit and volume transfer activity both fell record highs set in April. Transfer volumes typically fall to their lowest levels of the year following a frenzy of activity to meet the program’s annual end-of-April compliance deadline. Year-to-date transfer volume through May was 25% higher than the same period in 2021.

- Gevo's Iowa RNG will be marketed in California by BP. Gevo, a biofuels producer based in the United States, aims to sell renewable natural gas (RNG) produced in Iowa and marketed by BP in the California Low Carbon Fuel Standard (LCFS) market. According to the firm, Gevo's plant in northwest Iowa has begun production and is injecting RNG into the local pipeline. The project, which is expected to generate around 355,000 mmBtu/yr, gathers biogas from three nearby farms and converts it to RNG. BP's marketing teams will transfer the gas to California and sell it. Beginning in 2023, the project is estimated to produce between $16 million and $22 million each year. The revenue is determined by the value of credits obtained through the California LCFS program and the federal Renewable Fuel Standard (RFS). Gevo stated that it expects to receive RIN approval through the RFS as well as LCFS credits later this year or next year.

- Oregon argues in favor of suggested CFP targets. Few participants were pleased as Oregon regulators are nearing a formal proposal for setting tougher low-carbon fuel standard requirements. A proposed modification to the state's Clean Fuels Program calls for a statewide reduction in fuel carbon intensity of 20% by 2030 and 37% by 2035. The agency will formally propose the changes in July, with final approval expected in late September. Based on the reductions seen thus far under the program, renewable and alternative fuel producers argued for even higher benchmarks. Conventional fuel producers on the other hand, questioned whether the state could accomplish a significant increase after 2030. The department intends to assess the program's progress in 2029.

- Oregon CFP credit transfers are decreasing. According to the Oregon Department of Environmental Quality, credit transfer volume in the Oregon Clean Fuel Program fell in May but remained more than double that of the same month last year. Last month, participants reported moving over 67,000 metric tons of credits across 24 transfers. This was a decrease from the over 125,000 t of credits moved in April, but it was still greater than the approximately 29,000 t of credits moved in May 2021.

Schedule

- June 30, 2022: California LCFS 1Q 2022 reporting deadline

- July 29, 2022: California LCFS 1Q 2022 data release

- September 20, 2022: California LCFS 2Q 2022 reporting deadline

- October 31, 2022: California LCFS 2Q 2022 data release

LCFS Credit Pricing

Credits Prices as of June 16th, 2022:

-

-

- California - Spot Delivery $88.00

- Oregon - Spot Delivery $112.00

LCFS Credit Transfer Activity for California

|

Time

|

Transfers

|

Total Volume

|

Avg $/credit

|

|

May- 22

|

119

|

861,000

|

$ 125

|

|

Apr- 22

|

468

|

4,584,000

|

$ 153

|

|

Mar- 22

|

280

|

3,301,000

|

$ 158

|

|

Feb – 22

|

159

|

1,550,000

|

$ 163

|

|

Jan -22

|

358

|

3,389,000

|

$ 167

|

|

Dec -21

|

269

|

3,217,000

|

$ 172

|

|

Nov -21

|

128

|

1,125,000

|

$ 174

|

|

Oct -21

|

434

|

3,782,000

|

$ 182

|

|

Sept -21

|

136

|

1,518,000

|

$ 183

|

|

Aug -21

|

100

|

709,000

|

$ 185

|

|

July -21

|

252

|

2,125,000

|

$ 188

|

|

June -21

|

190

|

1,873,000

|

$ 190

|

|

May -21

|

81

|

791,000

|

$ 190

|

|

Apr -21

|

345

|

3,455,000

|

$ 192

|

|

Mar-21

|

307

|

3,490,000

|

$ 198

|

|

Feb-21

|

87

|

1,019,000

|

$ 197

|

|

Jan-21

|

335

|

2,176,000

|

$ 199

|

|

Dec-20

|

260

|

2,997,000

|

$ 199

|

|

Nov-20

|

133

|

1,207,000

|

$ 196

|

|

Oct-20

|

336

|

2,237,000

|

$ 198

|

|

Sept -20

|

167

|

1,553,000

|

$ 196

|

|

Aug-20

|

111

|

857,000

|

$ 196

|

|

Jul-20

|

334

|

2,509,000

|

$ 199

|

|

June-20

|

129

|

1,059,000

|

$ 202

|

|

May-20

|

90

|

470,000

|

$ 195

|

|

Apr-20

|

344

|

4,098,000

|

$ 198

|

|

Mar-20

|

233

|

2,312,000

|

$ 199

|

|

Feb-20

|

84

|

581,000

|

$ 206

|

|

Jan-20

|

240

|

1,895,000

|

$ 200

|

|

Dec-19

|

217

|

2,216,000

|

$ 197

|

|

Nov-19

|

88

|

705,000

|

$ 195

|

|

Oct-19

|

243

|

1,990,000

|

$ 195

|

|

Sep-19

|

137

|

1,179,000

|

$ 195

|

|

Aug-19

|

89

|

929,000

|

$ 194

|

|

Jul-19

|

188

|

1,574,000

|

$ 193

|

|

Jun-19

|

114

|

875,000

|

$ 190

|

|

May-19

|

76

|

408,000

|

$ 185

|

|

Apr-19

|

131

|

1,299,000

|

$ 180

|

|

Q1 2019

|

373

|

2,972,000

|

$ 188

|

|

CY 2018

|

1725

|

13,334,000

|

$ 160

|

|

CY 2017

|

1226

|

8,875,000

|

$ 89

|

|

CY 2016

|

929

|

5,343,000

|

$ 101

|

|

CY 2015

|

578

|

2,852,000

|

$ 62

|

|

CY 2014

|

304

|

1,667,000

|

$ 31

|

|

CY 2013

|

202

|

887,000

|

$ 55

|

|

CY 2012

|

24

|

164,000

|

$ 17

|

Source: https://ww2.arb.ca.gov/resources/documents/monthly-lcfs-credit-transfer-activity-reports

LCFS Cost for Gasoline and Diesel

Costs as of June 16th, 2022, for Vintage 2022:

-

- California

- Carbob (No Cl ethanol)- Vintage 2022 10.72 cents per USG

- Carbob (79.9 Cl ethanol)- Vintage 2022 10.03 cents per USG

- Oregon

- E10 gasoline- Vintage 2022 6.51 cents per USG

- B5 diesel – Vintage 2022 7.40 cents per USG

Market Update

- 5 out of the last 6 quarters have seen credits outpace deficits which has caused the bank of LCFS credits to grow from a low of 7.4 million in Q2 ’20 to 9.4 million in Q4 ’21. The trend is expected to continue when Q1 ’22 data is reported.

- California LCFS traded $77 in June which was within $2 per credit of a 5 year low of $75 back in July 2017. Prices have rebounded to $88 as of June 16th.

- ARB is analyzing future carbon intensity scores for fuels for future years which should see a reduction in number of LCFS credits issued per galloon of fuel delivered in California.

- As the program continues to beat the stated annual goals, ARB at some point may look to increase the pace of the goal and reductions in carbon intensity of fuels.

- The large blocks of LCFS credits generated by utilities with Electric Vehicle charging stations help keep a lid on pricing by routinely holding auctions for large blocks of 50,000 to 180,000 in one sale.

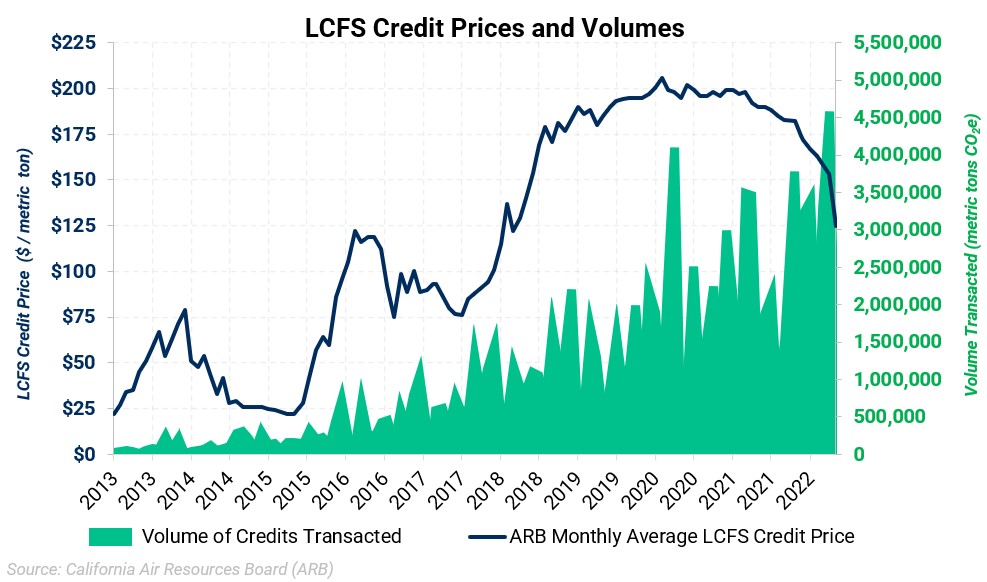

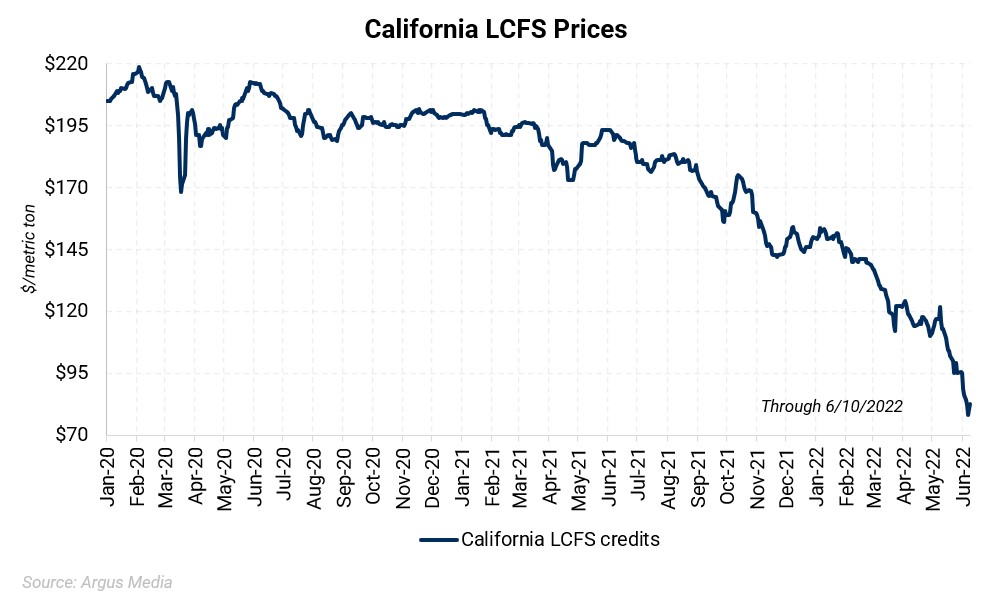

Figure 1. California LCFS USD/mt Jan. 2020 - Present

|

| |

2021 Average Daily Price: $176.53 2022 Average Daily Price: $123.36

2021 Highest Daily Price: $201.00 2022 Highest Daily Price: $153.50 (1/6/2022) |

Figure 2. California Monthly LCFS Credit Price and Transaction Volume as Reported by ARB

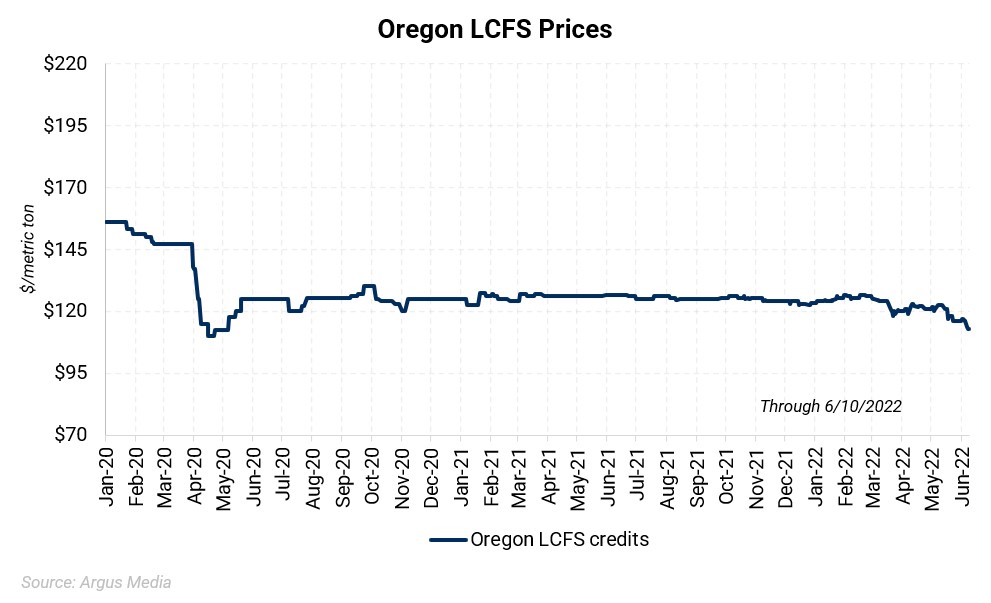

Figure 3. Oregon LCFS USD/mt Jan. 2019 – Present

|

|

|

|

|

2021 Average Daily Price: $125.32

|

2022 Average Daily Price: $121.86

|

|

2021 Highest Daily Price: $127.50

|

2022 Highest Daily Price: $126.50

|

Questions? Contact our team for more information: environmental@aegis-hedging.com

CONFIDENTIAL – UNAUTHORIZED THIRD-PARTY DISTRIBUTION PROHIBITED