Latest Insight

First Look: Oil heads for a second straight weekly loss as Iran downplays Israel's attack

To quickly access the page content, please click on the links below.

Climate Action Council Meeting 29th of September, 2022

|

TRADE DATE |

HUB |

PRODUCT |

STRIP |

SETTLEMENT PRICE |

PERCENTAGE DIFFERENCE FROM DEC 22 |

|

9/30/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-22 |

122.10000 |

100% |

|

9/30/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-23 |

99.25000 |

81% |

|

9/30/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-24 |

76.50000 |

63% |

|

9/30/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-25 |

80.15000 |

66% |

|

9/30/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-26 |

72.80000 |

60% |

|

9/30/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-27 |

75.10000 |

62% |

|

9/30/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-28 |

71.50000 |

59% |

|

9/30/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-29 |

66.85000 |

55% |

|

9/30/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-22 |

143.20000 |

100% |

|

9/30/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-23 |

123.05000 |

86% |

|

9/30/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-24 |

107.60000 |

75% |

|

9/30/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-25 |

98.35000 |

69% |

|

9/30/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-26 |

88.70000 |

62% |

|

9/30/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-27 |

93.00000 |

65% |

|

9/30/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-28 |

88.10000 |

62% |

|

9/30/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-29 |

87.15000 |

61% |

|

9/30/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-22 |

97.25000 |

100% |

|

9/30/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-23 |

70.50000 |

72% |

|

9/30/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-24 |

57.35000 |

59% |

|

9/30/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-25 |

54.00000 |

56% |

|

9/30/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-26 |

56.80000 |

58% |

|

9/30/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-27 |

60.95000 |

63% |

|

9/30/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-28 |

61.20000 |

63% |

|

9/30/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-29 |

61.95000 |

64% |

|

9/30/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-22 |

74.60000 |

100% |

|

9/30/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-23 |

55.85000 |

75% |

|

9/30/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-24 |

41.80000 |

56% |

|

9/30/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-25 |

41.35000 |

55% |

|

9/30/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-26 |

44.85000 |

60% |

|

9/30/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-27 |

45.85000 |

61% |

|

9/30/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-28 |

46.45000 |

62% |

|

9/30/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-29 |

47.20000 |

63% |

Buildout in New York’s clean energy. In order to meet the State’s clean energy goals, New York has to increase or refurbish zero-emission generation by 100,000MW. The New York Independent System Operator (NYISO) states that 111,000 – 124,000 MW of clean energy generation is needed to achieve the zero-emission grid goal by 2040. Around 80%, or 95,000 MW, will need to come from the new projects or modifications to the existing plants. Currently, New York's generating capacity is almost 37,500MW. The State’s goal is to achieve 70% renewable energy by 2030 and 100% by 2040. NYISO modeled a few scenarios which indicate New York will need 27,000 – 45,000 MW of “dispatchable emissions-free resources” like hydrogen, modular nuclear, and renewable natural gas. However, these kinds of sources are not commercially viable yet, even though they are essential for creating the zero-emission grid. Without these resources, the State might need to retain fossil fuel generation even after 2040 to secure the grid’s reliability.

New Jersey solar capacity growth. The New Jersey Clean Energy Program reported on September 28th that the State added 52.2MW in the new solar capacity in August. Therefore, improving the initial figures of 18.6MW and 26.1MW logged for June and July, respectively. However, it is still slightly less than the 53MW reported for April. Almost one-fifth of August capacity, around 9MW, went to the ADI initiative, the fixed-price portion of the State's new SREC-II incentive program. The remaining 43MW of the new capacity is fed into the State's transition incentive program, which issues transition renewable energy certificates (TRECs) at a base price of $152/MWh for a 15-year period and requires the State's four electricity distributors to buy the credits. No capacity went towards the legacy solar renewable energy certificate (SREC) program. The State has increased its solar fleet by 277 MW throughout 2022, to a total of 4,138 MW.

New Jersey calls for more offshore wind. The State is preparing for its third solicitation for offshore renewable energy certificates (ORECs) to follow its goal of 7,500 MW from ocean-based wind by 2035. The state Board of Public Utilities (BPU) is preparing a request for around 1,200 MW during the Q1 in 2023. In addition, the board is seeking information from the stakeholders regarding the various aspects like project design, performance guarantees to environmental fallout, and OREC pricing to help them develop a "solicitation guidance document ."The board plans to publish draft guidance after the second request for information, including work with PJM Interconnection on transmission planning aspects. The document should be issued around the end of November, followed by the month-long public comment period. The fourth and fifth solicitations are scheduled for Q2 of 2024 and 2026 and will aim for 1,200 MW and 1,342 MW, respectively. It is expected that all five solicitations will include wind farms and allow meeting the 7,500m MW goal by 2033. The board has already chosen the following:

New Jersey is aiming for 100% clean energy in 2050. Furthermore, Class I resources like wind and solar should become at least 50% of utility sales by 2030.

New Jersey’s Environmental Justice rules. After closing the public comment period on September 4th, the Department is reviewing the received feedback. All comments can be found here. The Department is still aiming to adopt the rule by December 31st, 2022. The full proposal can be found here.

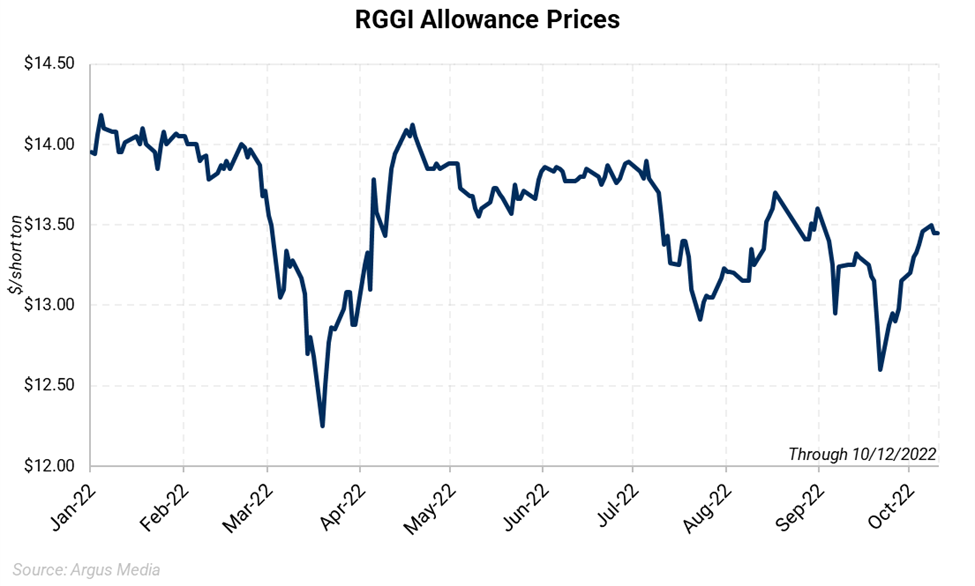

RGGI Auction 57. The Regional Greenhouse Gas Initiative (RGGI) concluded September’s 7th CO2 allowance auction at a price of $13.45/short ton, selling all 22.4 million allowances offered and generating approximately $301 million. Compliance-oriented entities purchased 78% of the allowances available, up from 66% in June’s 1st auction. According to the program, 54% of all allowances in circulation are held for compliance purposes. Bids ranged from the program's price floor of $2.44/st to $20.00/st, with bid volumes 2.6 times greater than available allowances. Allowances were awarded to 52 of the 66 bidders at the end of the auction. Four bidders purchased more than one million allowances, while 27 bidders purchased at least 200,000. The next RGGI auction is scheduled for December 7th, but which states will participate is unknown.

RGGI program review. Significant market uncertainty is seen in the RGGI program as Pennsylvania’s entrance is still blocked by the court order and as Virginia expressed the goal to exit by the following December. Consequently, stakeholders are providing their input and comment on regulations for States entering and exiting the program for the ongoing RGGI review.

Virginia starts the regulatory process to leave RGGI. On September 7th, Virginia’s Governor Youngkin’s administration filed a Notice of Intended Regulatory Action (NOIRA) to initiate the first steps towards revoking the trading rule and the State's status in RGGI. In addition, supporting information submitted by the State's Department of Environmental Quality (DEQ) provided a setup for a full Administrative Process Act (APA), which creates regulations to revoke initial rulemaking that included Virginia in the RGGI program. The reasons to exit RGGI included in NOIRA – higher electricity cost for the final consumers and RGGI allowance price increase of 146% since 2020 when Virginia joined the program. Furthermore, energy providers can currently charge ratepayers for the transition and expansion of clean energy infrastructure. NOIRA filling also emphasizes that the program in Virginia was implemented differently and does not follow the initial idea of distributing RGGI proceeds to the consumers to compensate for passed compliance costs, which naturally leads to higher electricity prices. Consequently, utilities are not seeking ways to reduce compliance costs or emissions. The DEQ is planning to receive public comments on NOIRA till October 26th.

RGGI Allowance balance.

AEGIS is working on a RGGI model which will be updated after the Q3 ’22 emissions data is released.

Here is brief snapshot of analysis:

After calendar year 2021, the bank of allowances stands roughly at 86.3 million allowances after starting the year at 95.5 million allowances. Emissions in the first half of ’22 vs first half of ’21 rose 2.4%. The bank is again expecting to drop and depending on the 2nd half of ’22 emissions it should drop between 7 -14 million allowances. This should leave the bank between 72.3 million and 79.3 million at the end of 2022. This yearly reduction of the bank is expected to continue through 2025. It may continue 2026 -2030 if they announce a 4th adjustment to the bank to take effect starting in 2026 once the 3rd adjustment to the bank is completed in 2025.

Questions? Contact our team for more information: environmental@aegis-hedging.com

CONFIDENTIAL – UNAUTHORIZED THIRD-PARTY DISTRIBUTION PROHIBITED