Latest Insight

First Look: Mountain Valley Pipeline requests to start commercial service in May

To quickly access the page content, please click on the links below:

|

|

||

|

|

||

|

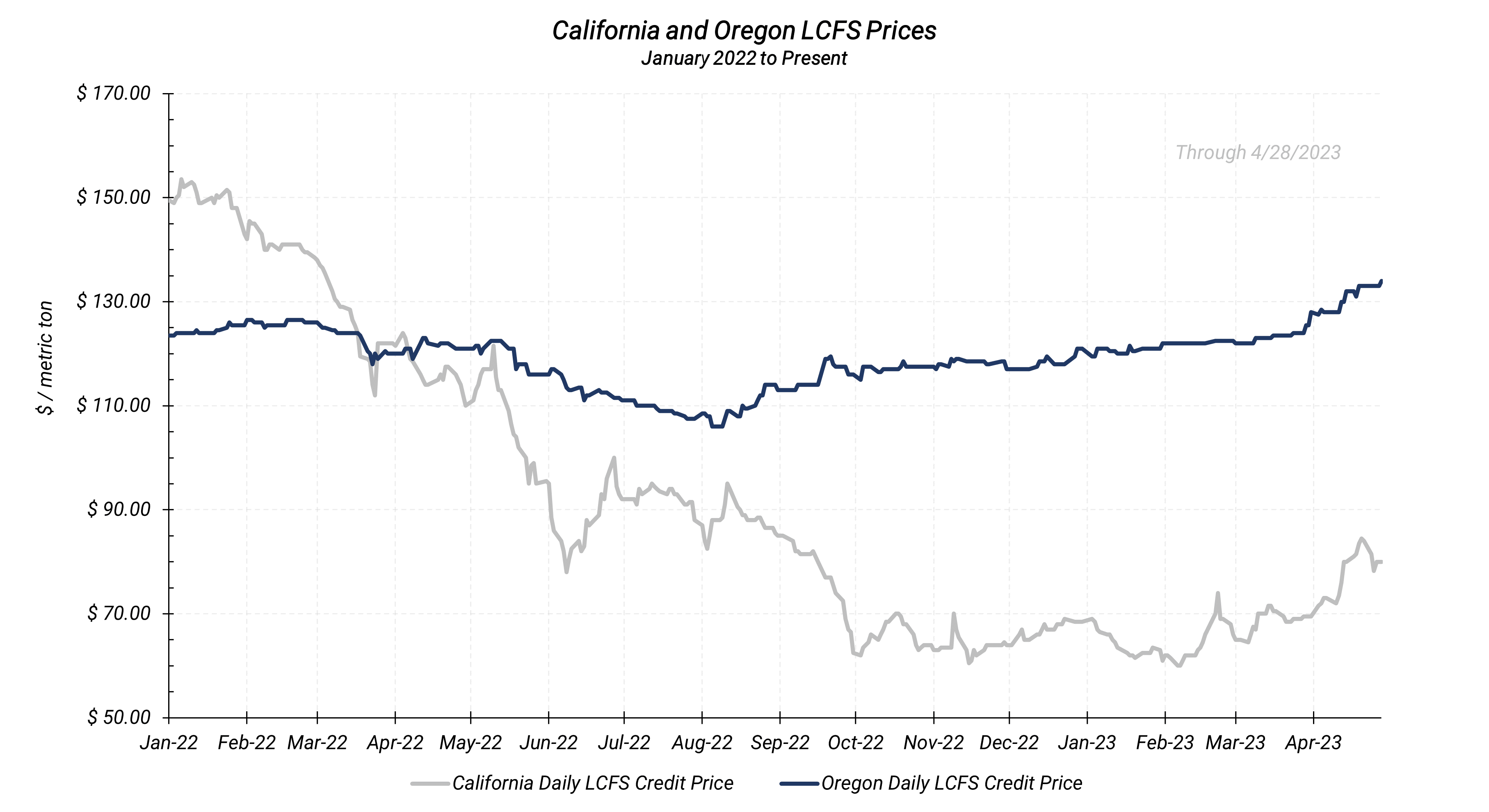

LCFS Spot Contract |

California LCFS |

Oregon LCFS |

|

Price April 28th, 2023 |

$ 88.00 |

$ 134.00 |

|

Avg. Weekly Price April 24th - April 28th, 2023 |

$ 79.95 |

$ 133.20 |

|

Average Monthly Price April 2023 |

$ 78.17 |

$ 130.95 |

|

|

|

|

|

LCFS Futures Contract |

Pricing |

|

|

Dec. '23 |

$ 84.90 |

|

|

Dec. '24 |

$ 92.10 |

|

|

Dec. '25 |

$ 97.65 |

|

The California Low Carbon Fuel Standard (LCFS) market halted a three-week rally as demand exited the marketplace and futures markets. Prompt credits lost nearly $3.00/t, on average last week. LCFS strength has been driven by trader buying and strength in futures markets in recent weeks.

The forward curve remained in contango though a flatter structure at midweek made for volatility over the course of the week.

|

||||

|

|

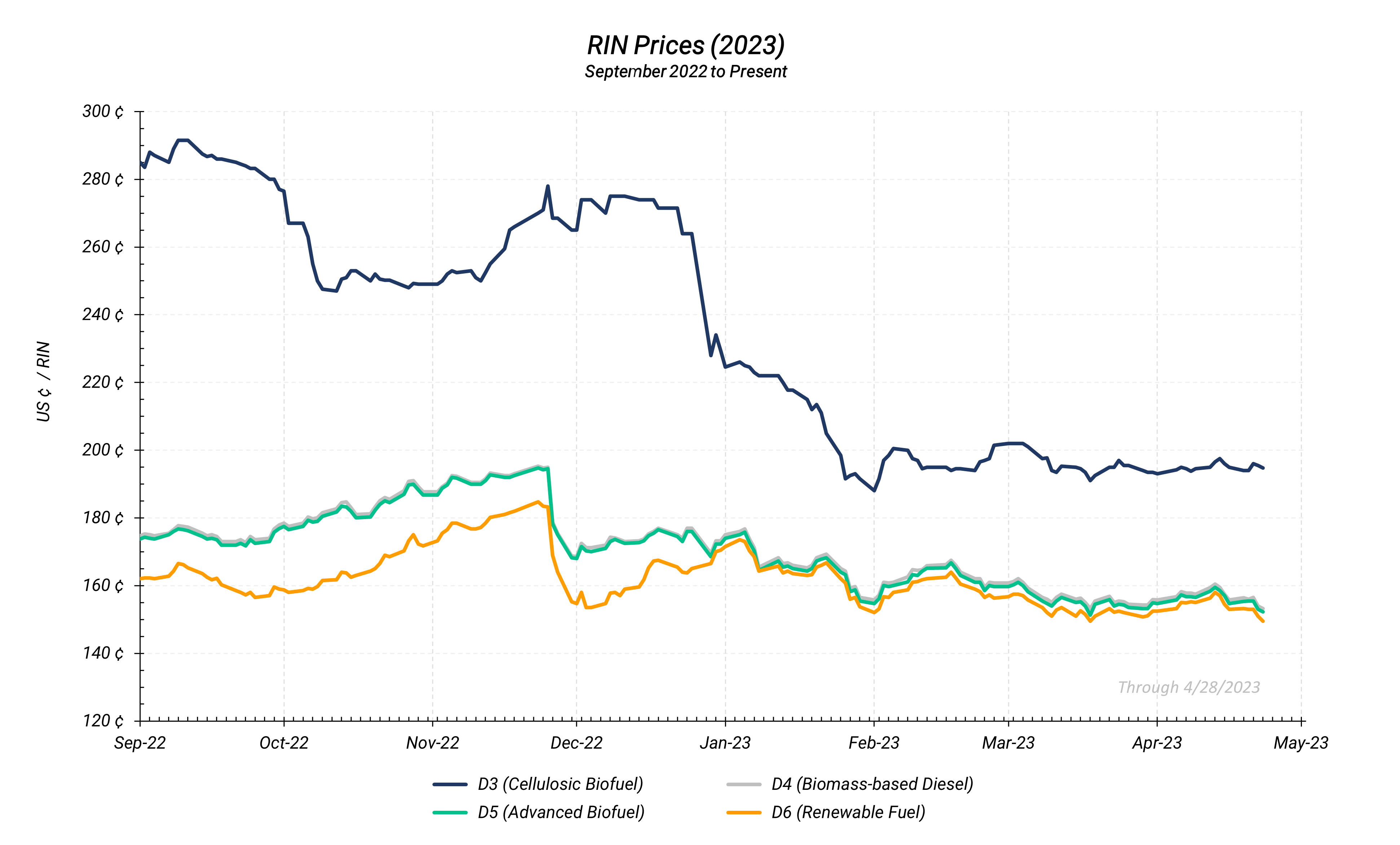

D3 |

D4 |

D5 |

D6 |

|

Price April 28th, 2023 |

$ 1.95 |

$ 1.53 | $ 1.52 | $ 1.50 |

|

Avg. Weekly Price April 24th - April 28th, 2023 |

$ 1.95 |

$ 1.55 | $ 1.54 | $ 1.52 |

|

Average Monthly Price April 2023 |

$ 1.95 |

$ 1.57 | $ 1.56 | $ 1.54 |

RIN prices lost ground as news that the Biden administration would allow summer sales of E15 along with record March D4 RIN generation of nearly 619 million RINs weighed on markets.

Debt ceiling negotiations saw non-farm state Republicans look to put advanced biofuel credits on the chopping block, while protecting SAF and carbon capture projects. President Joe Biden threatened to veto the bill, quashing the potential bullish headline impact.

EPA Administrator Michael Regan issued comments at a House Agriculture Committee hearing last wek indicating the EPA is likely to cave to both industry and lawmaker pressure to increase the advanced biofuel mandate in the final ruling expected in June.

News that United Refining was denied its SRE hardship waiver by the Third Circuit court added bullish undertones to the RIN complex as the move adds additional demand to the marketplace. Trade organization Growth Energy entered comments in support of enforcing SREs in its case against the EPA. A full denial of all SREs would represent more than 1.6 billion RINs

Prior to this month’s moves, the approval by a federal court of a SRE for Calumet Special Products 30,000 b/d refinery in Montana provided bearish undertones to RIN markets.

SREs were carved out in the Renewable Fuel Standard (RFS) for refiners producing 75,000 b/d or less which could prove compliance with the RFS—i.e., purchasing RINs—resulted “undue economic hardship.”

The chance of a pivot in the EPA's approach to SREs continued to provide underlying bearish sentiment. A reversal or dovish change in SRE policy would have an outsized impact on the D6 category.

Market activity is likely to remain curtailed ahead of guidance from the EPA expected in June.

Questions? Contact our team for more information: environmental@aegis-hedging.com