To quickly access the page content, please click on the links below:

|

|

||

|

|

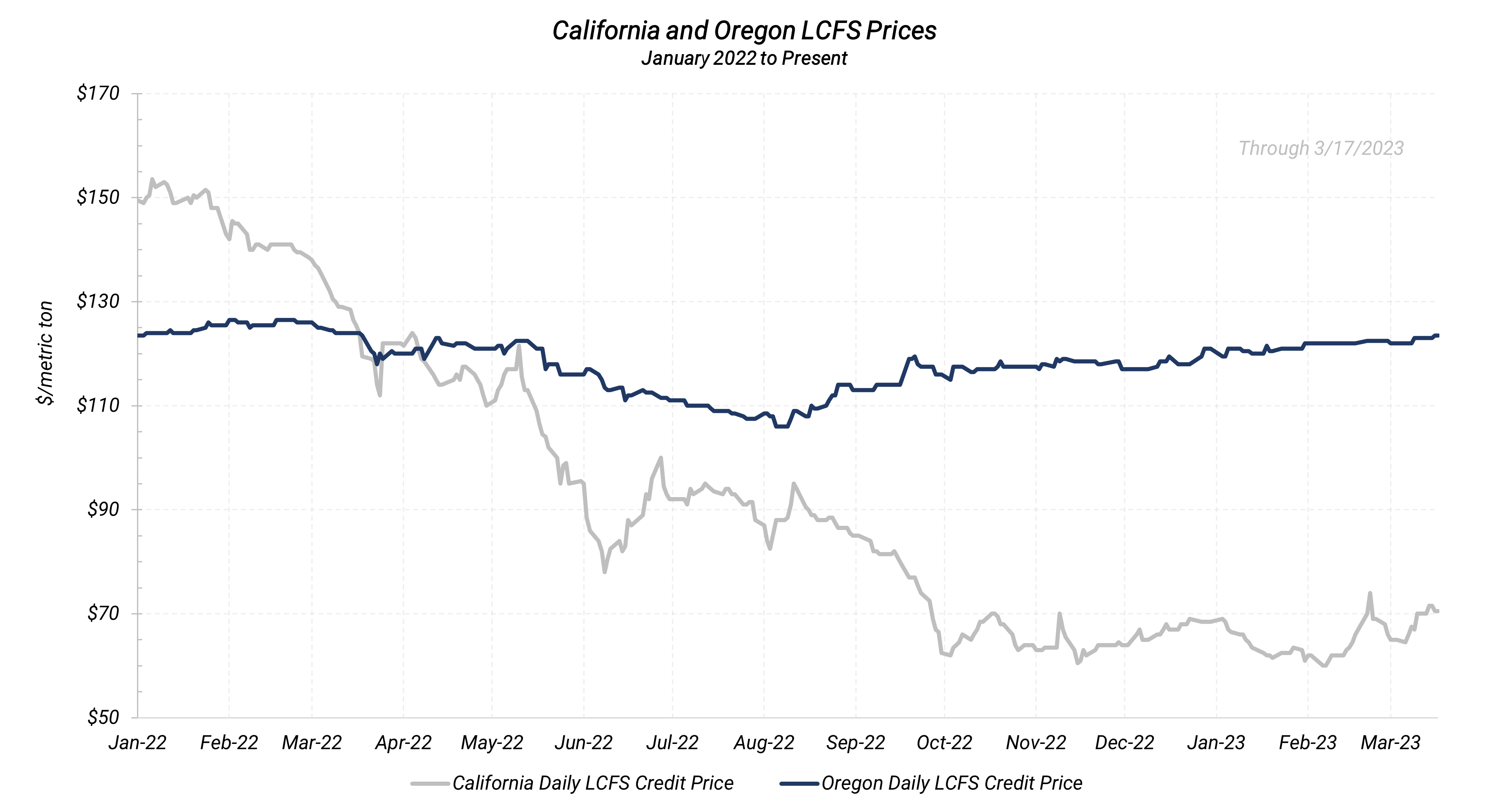

California LCFS |

Oregon LCFS |

|

Price March 17th, 2023 |

$ 70.50 |

$ 123.50 |

|

Average Weekly Price Mar. 13th - Mar. 17th, 2023 |

$ 70.80 |

$ 123.20 |

|

Average Monthly Price March 2023 |

$ 68.00 |

$ 122.62 |

The LCFS pressed higher for a second consecutive week amid trader buying. Prompt credit prices gained $3.8/t, or 5.7%, week-over-week. Issues surrounding some pending RD facilities could be spurring buying Further gains were limited by the structural oversupply of the LCFS marketplace.The forward structure formed a slight contango through Q4.

|

||||

|

|

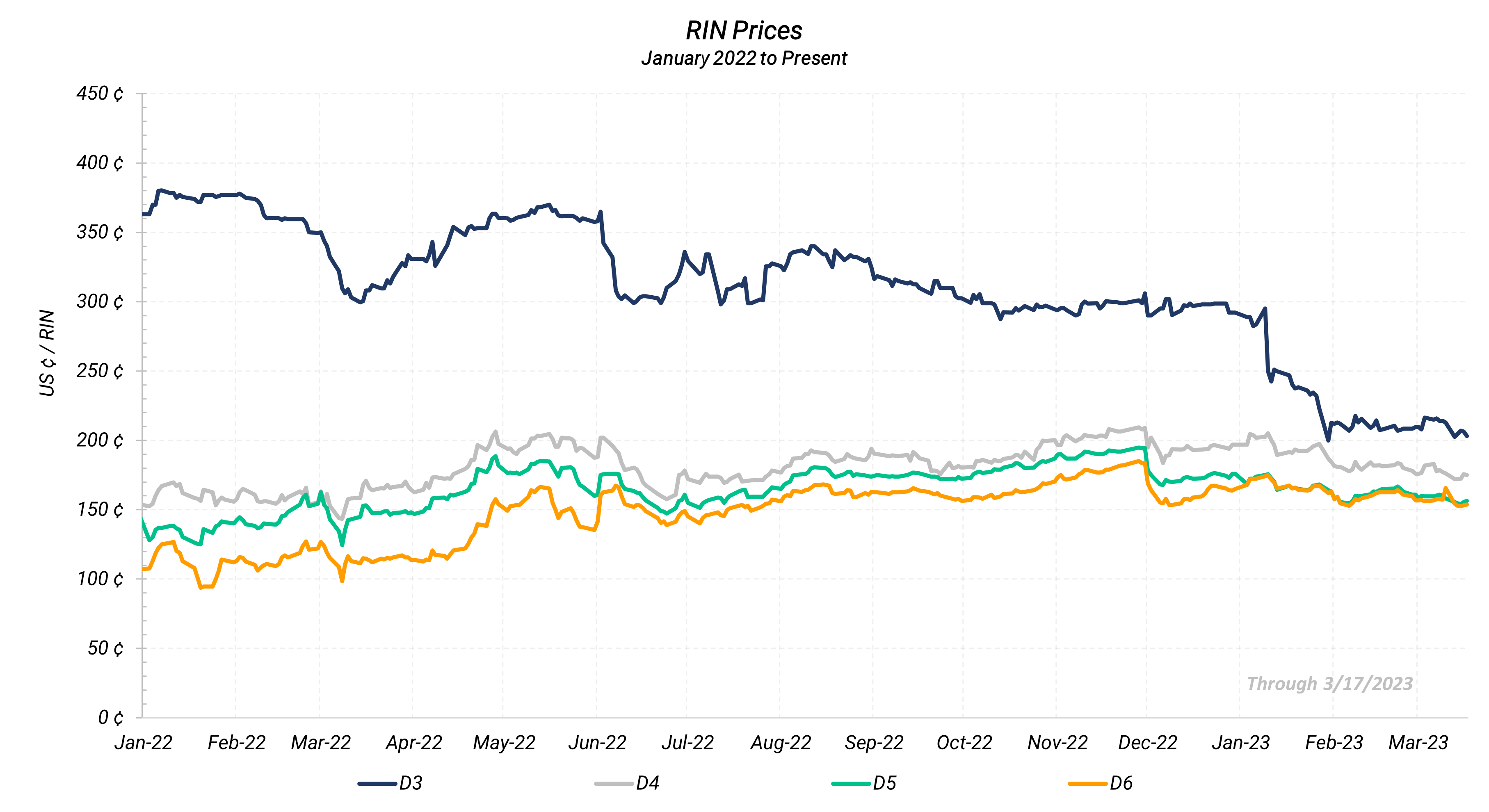

D3 |

D4 |

D5 |

D6 |

|

Price March 17th, 2023 |

$ 1.95 |

$ 1.58 | $ 1.57 | $ 1.54 |

|

Average Weekly Price Mar. 13th - Mar. 17th, 2023 |

$ 1.96 |

$ 1.56 | $ 1.55 | $ 1.53 |

|

Average Monthly Price March 2023 |

$ 1.99 |

$ 1.59 | $ 1.58 | $ 1.55 |

RIN prices traded lower on thin activity last week. D4 RINs fell 4.5¢/RIN, or 2.8%.

Fresh RIN production data showed D4 RIN generation remained robust at nearly 514 million credits. This, along with the issue of a new Small Refinery Exemption (SRE) petition for 2022 continued to provide a bearish undercurrent to the marketplace.

The chance of a pivot in the EPA's approach to SREs continued to provide underlying bearish sentiment and D6 RINs were marginaly lower. A reversal or dovish change in SRE policy would have an outsized impact on the D6 category. D3 RINs lost ground as higher February RIN generation numbers came out.

Questions? Contact our team for more information: environmental@aegis-hedging.com