Renewable Diesel & Biodiesel Margins Hit One-Month Highs

While the week ended 20 January was driven almost exclusively by Nymex ULSD gains, this week saw all factors move in concert toward supporting both RD and BD margins.

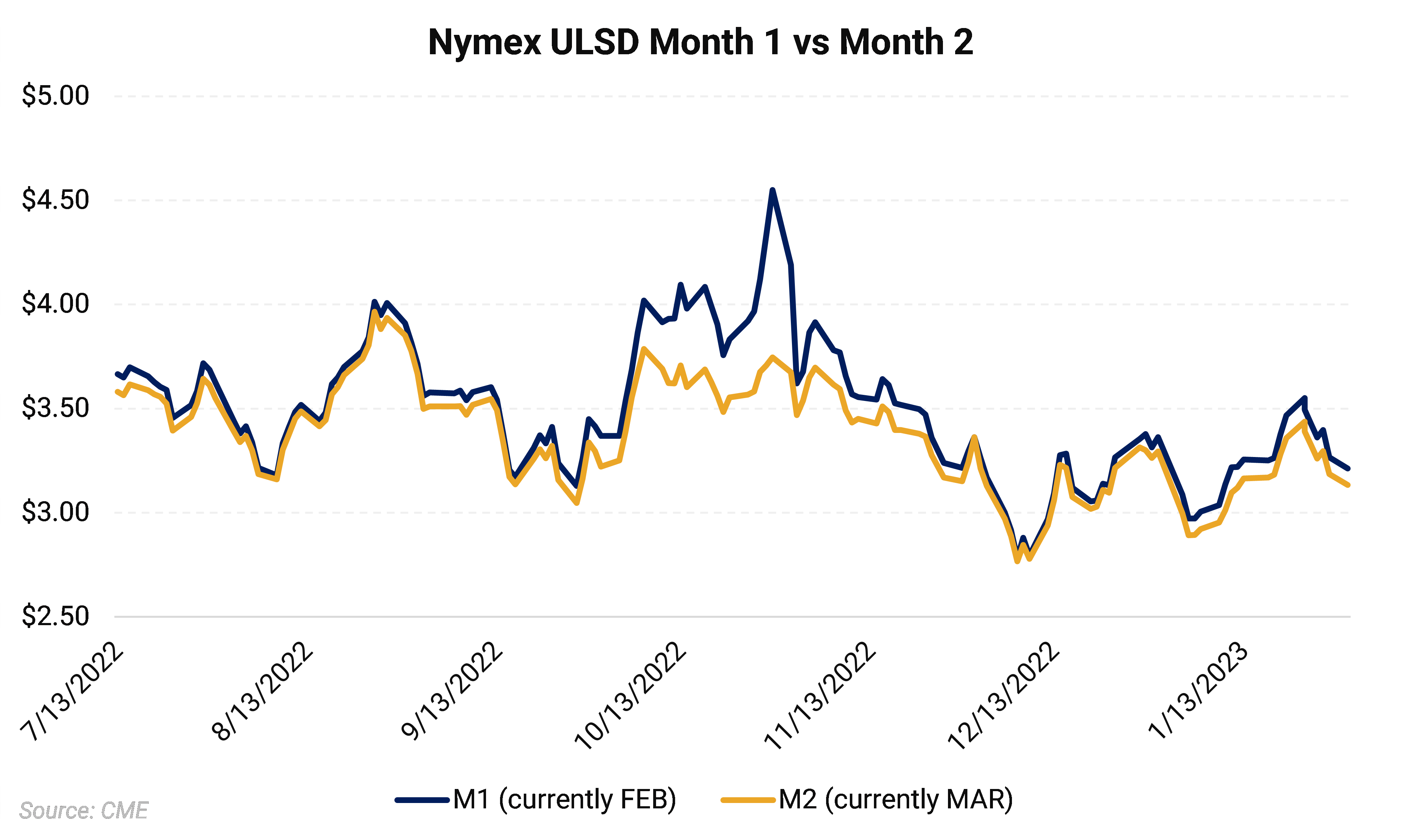

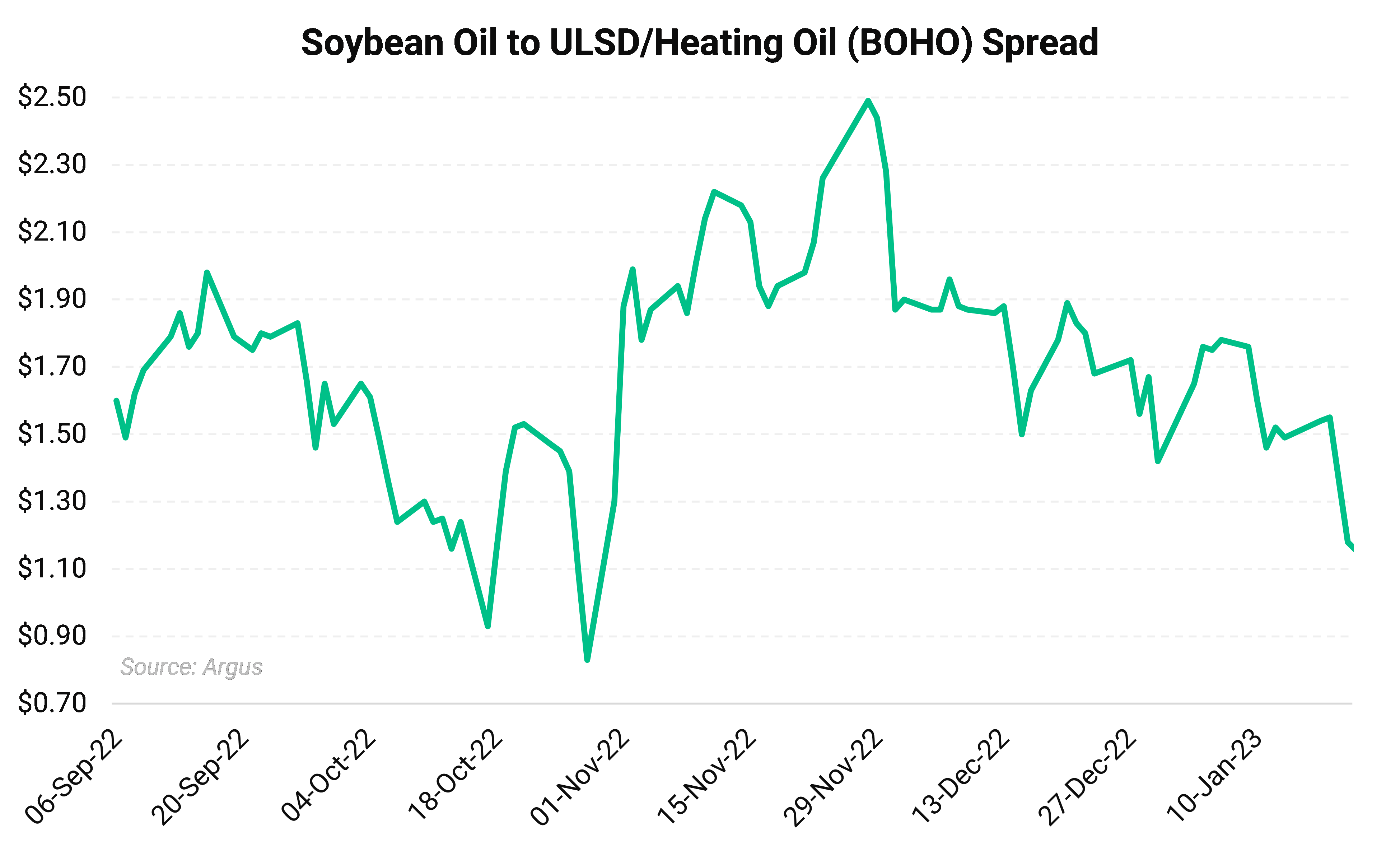

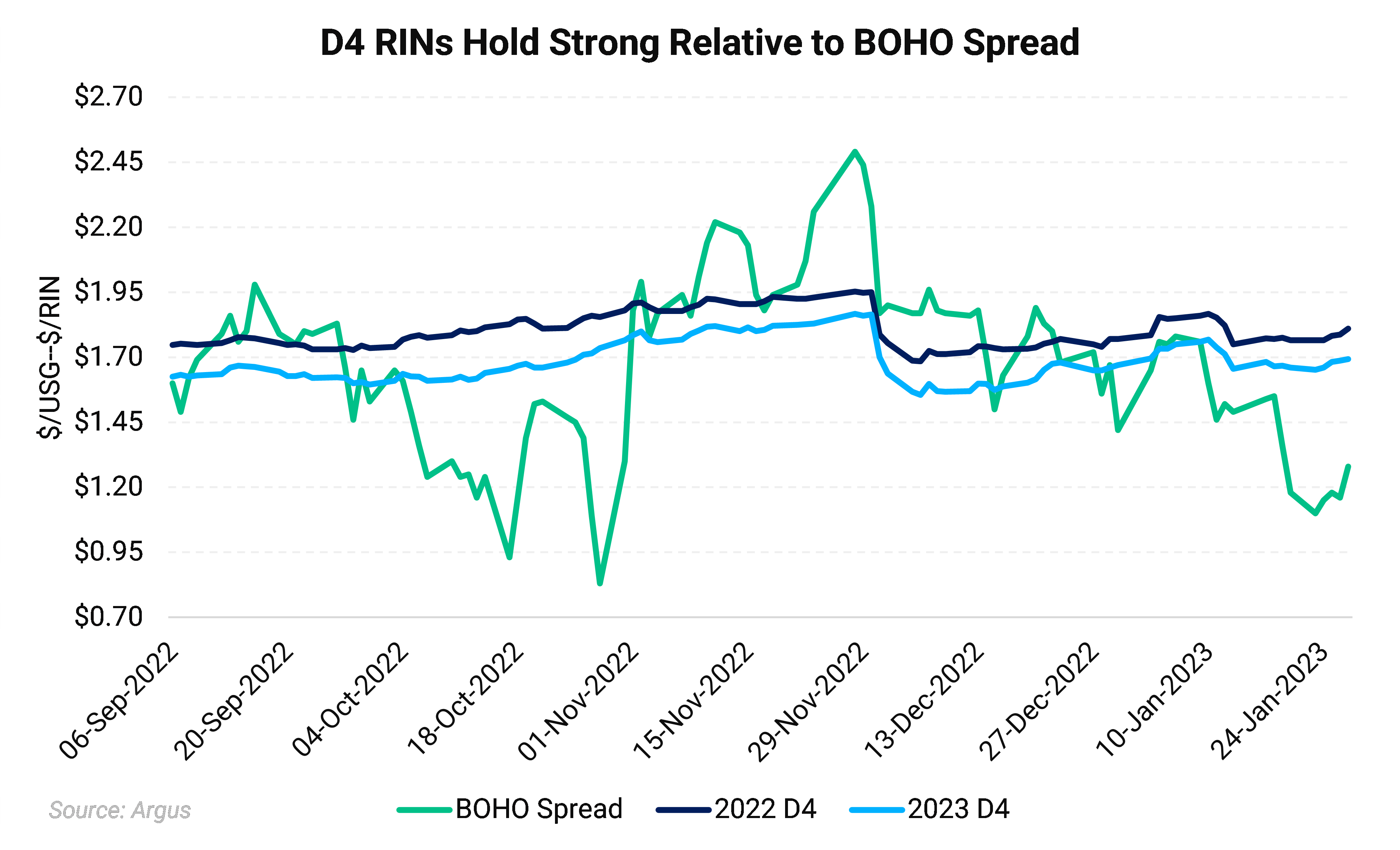

To start, Nymex ULSD gains slowed to under $0.07/gallon, or 1.9%, while March CBOT SBO contracts shed 1.92¢/lb, or 3.0%, week-over-week. This saw the BOHO spread contract to the narrowest level since late-October 2022.

Credit markets firmed modestly despite a strengthening margin environment which would typically down RIN values all else equal. As can be seen in the BOHO to D4 comparison chart below, D4 credits have decoupled from their more typical positive correlation to hold strong despite the strongest biodiesel margins in three months.

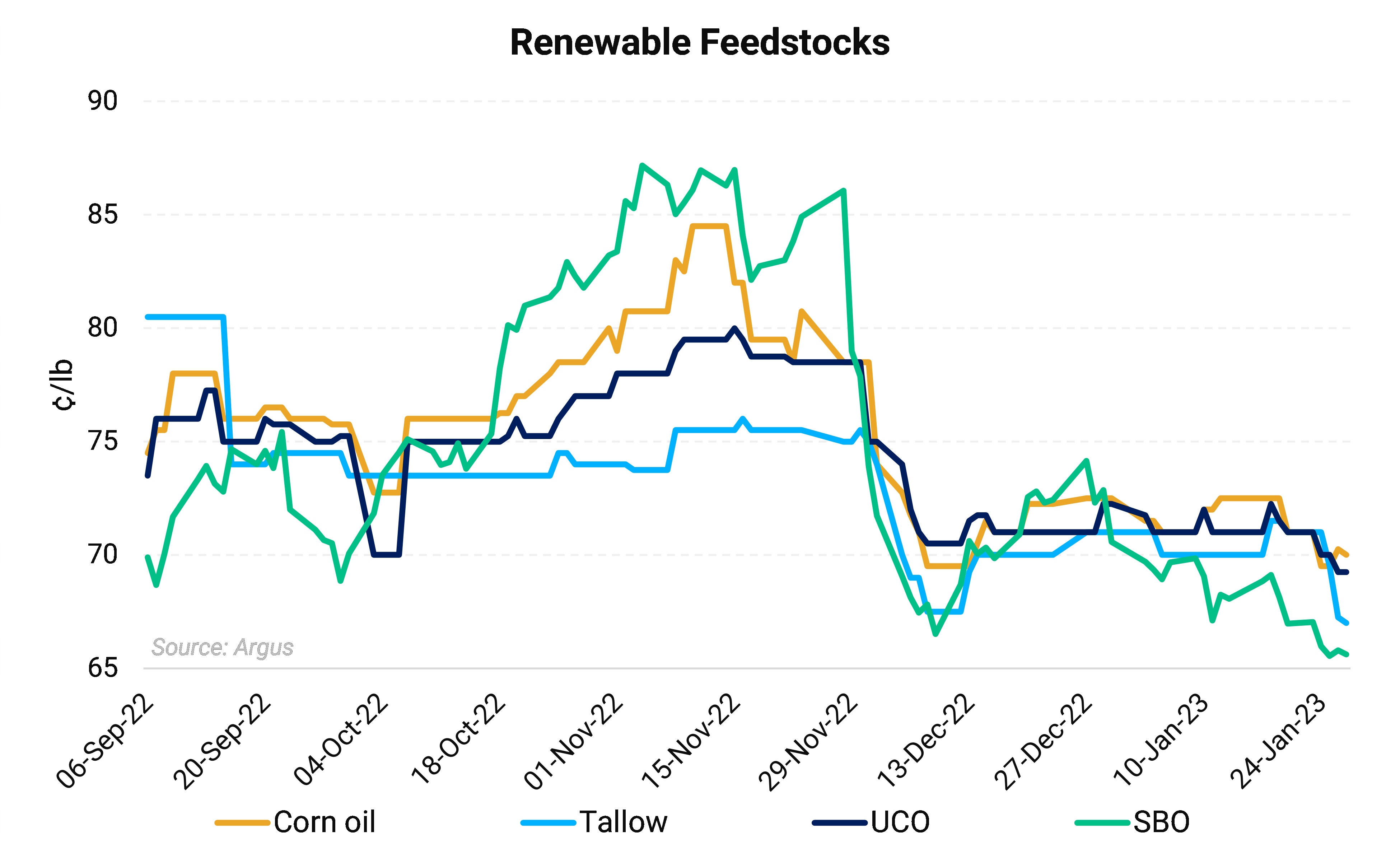

LCFS notched up $0.70/t, or 1.1pc on average, modestly boosting margins for lower carbon intense (CI) feeds like UCO and DCO.

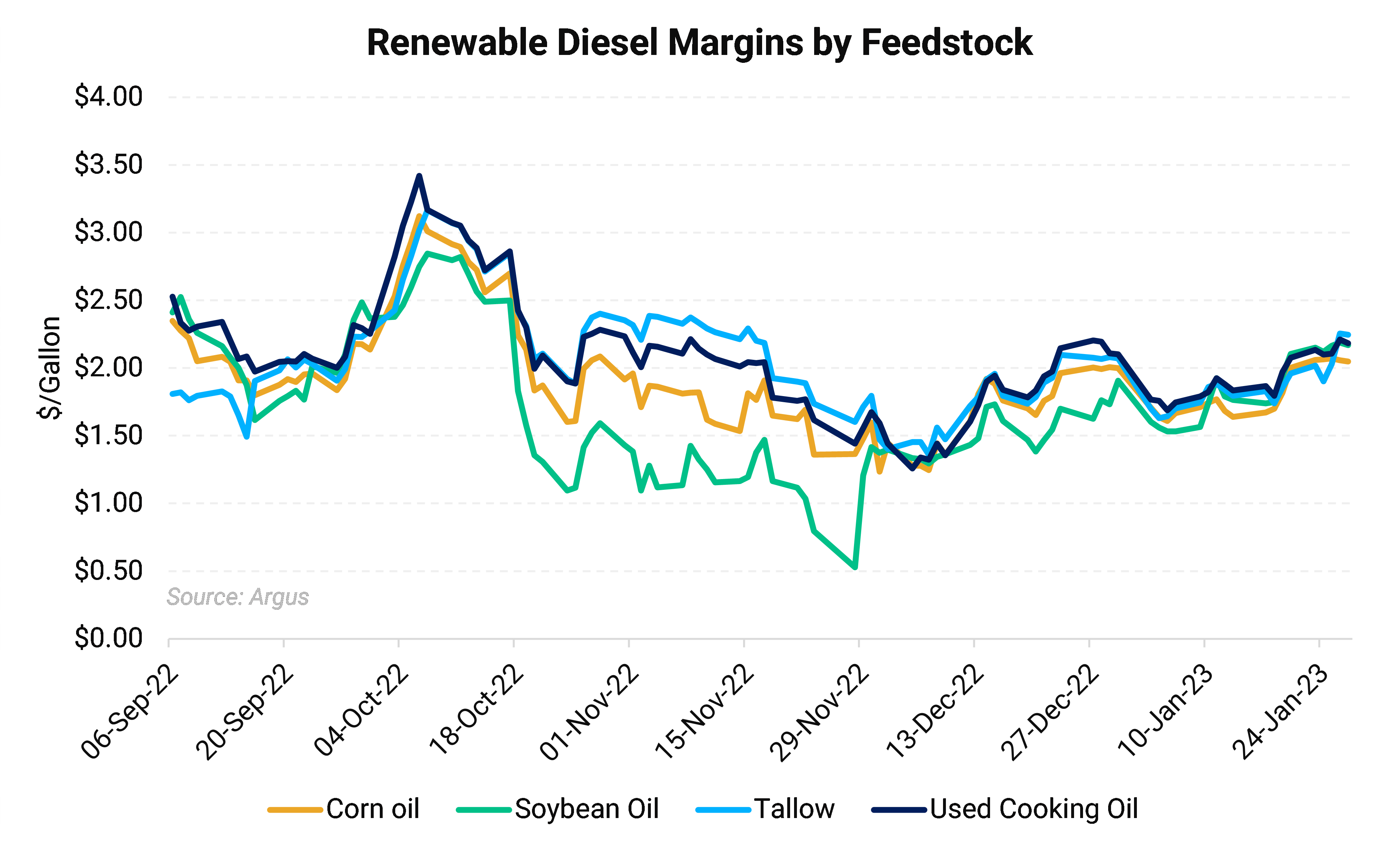

US Gulf coast renewable diesel, soybean oil-based margins reached the highest levels since mid-October 2022 last week, at $2.19/gallon. UCO was the second highest returning feedstock on average at $2.15/gallon, marking a one-month high.

Stubbornly high DCO prices continue to limit more return for RD producers at $2.06/gallon, up $0.26/gallon, or nearly 15% week-over-week, while a pullback in bleached fancy tallow (BFT) prices saw BFT margins exceed DCO on average at $2.09/gallon.

Feedstocks shed 1.5¢/lb to 2.3¢, with SBO leading the declines and UCO posting the smallest loss (see below).

Biodiesel margins, as measured by the soybean oil-to-heating oil (BOHO) spread, firmed $0.23/gallon, or nearly 17%, week-over-week as the front-month Nymex ULSD contract gained nearly 7¢/gallon over the same period, or 1.9%, while the March CBOT soybean oil contract fell 2.28¢/lb, or 3.6%.

The narrower the BOHO spread the stronger the margin as the main input cost for biodiesel producers, soybean oil, is more advantageously priced, while the petroleum-based fuel biodiesel is blended with strengthens—allowing for more margin.

The BOHO spread is a simplistic breakdown of the pulse of the biodiesel industry and is in widespread use by the industry. The BOHO spread does not account for operational costs which can vary drastically from plant to plant, nor the additional margin value afforded by credits and/or the sale of byproducts such as glycerin.

While the BOHO spread has more expensive feedstock costs outpacing ULSD for a loss of $1.28/gallon as of 27 January, producers recover the fixed $1.00/gallon blenders’ tax credit (BTC) as well as roughly $2.54/USG of D4 RIN value at current 2023 vintage pricing. Thus credit values offset the negative soybean oil-based biodiesel margin.

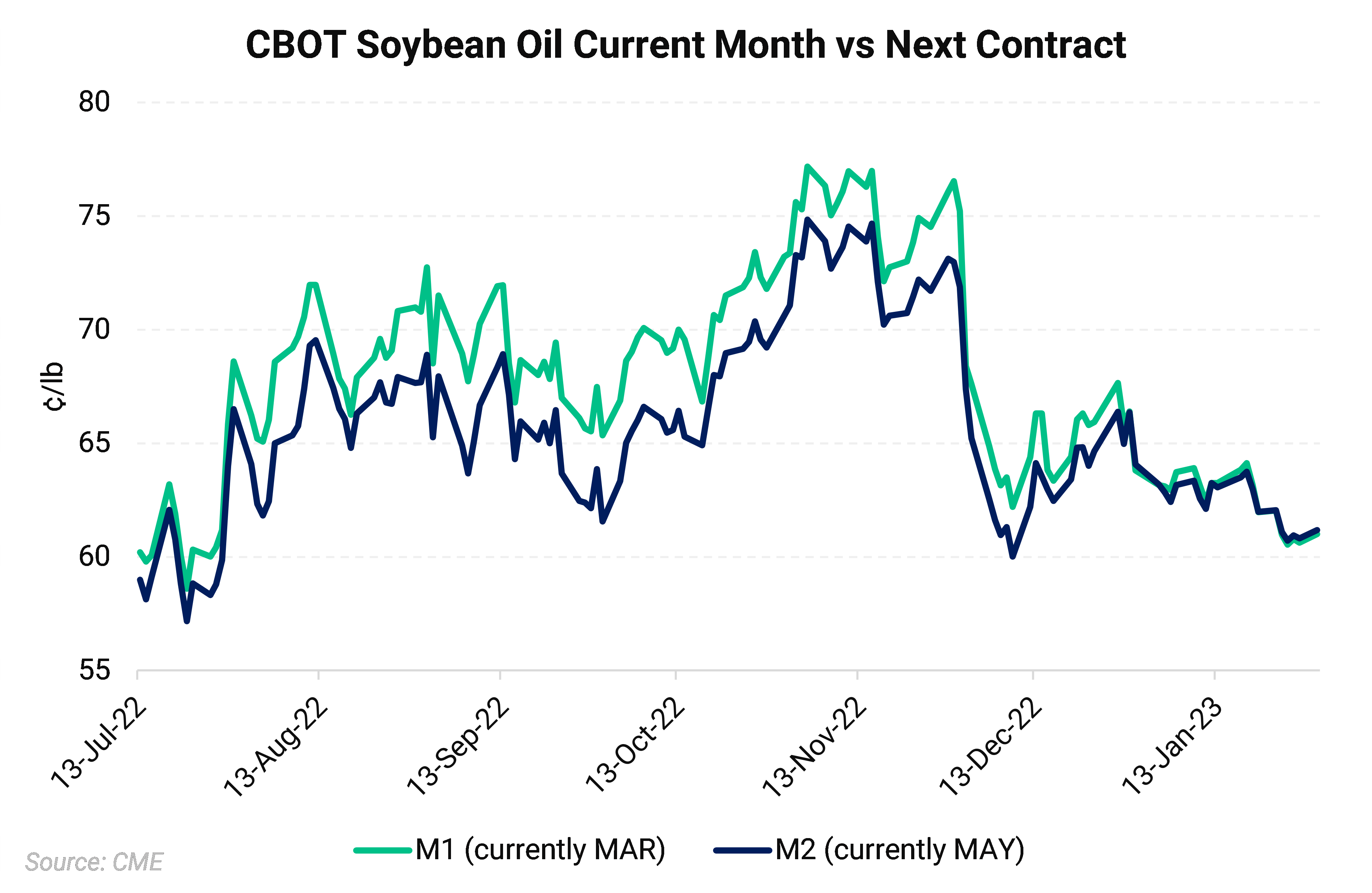

Prompt March CBOT soybean oil contracts were little changed week-over-week, edging up just 0.084¢/lb week-over-week. Spot soybean oil lost marginal value over the same period lifted average RD margins to the highest level since mid-October 2022. The actively traded March and May contract effectively reached parity on January 20.

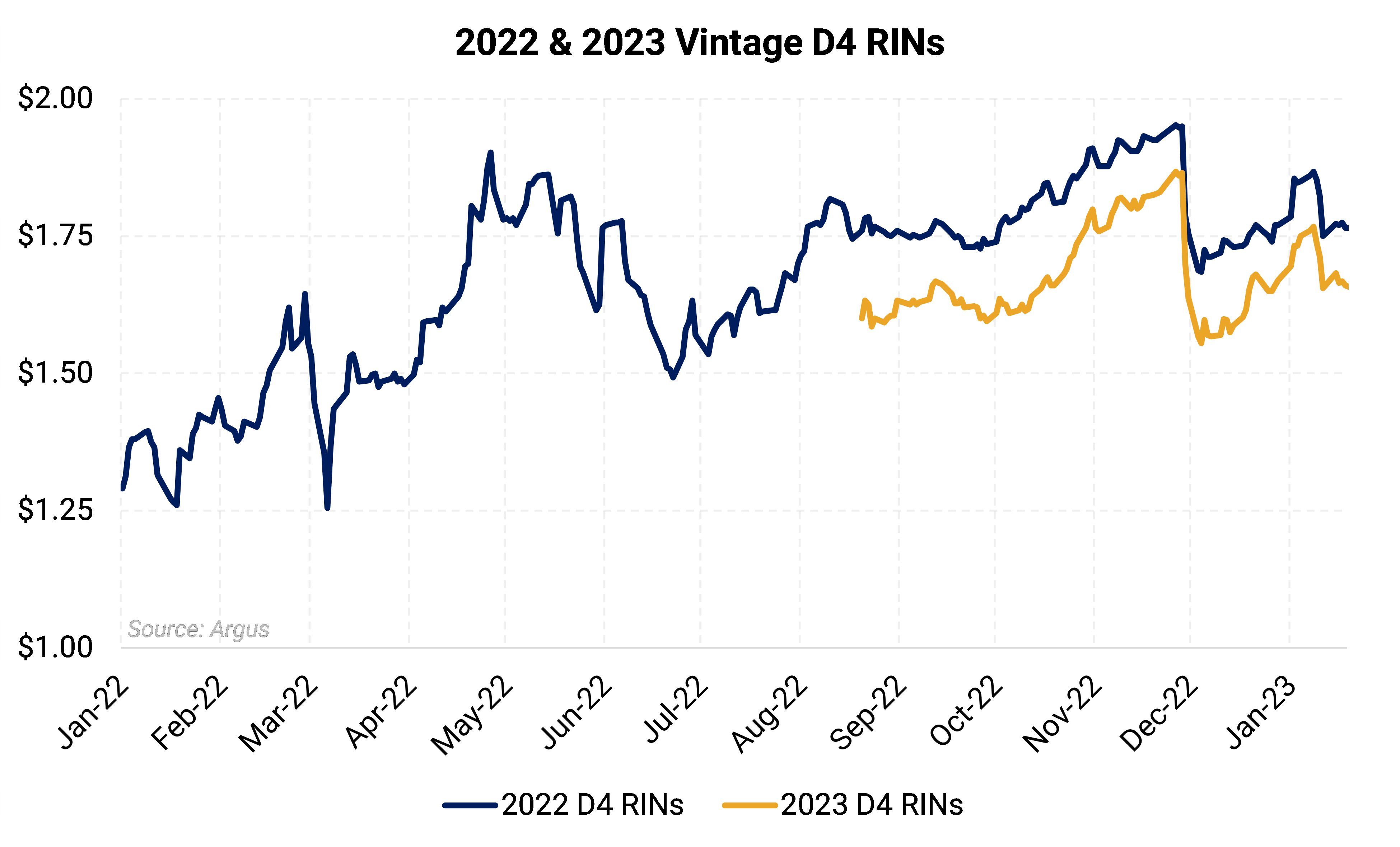

RINs provided modest lift to RD and BD margins this week. RIN markets retained strength given tighter 2022 RIN supply, while lower 2023-2025 proposed mandates and falling feedstock costs limited gains.

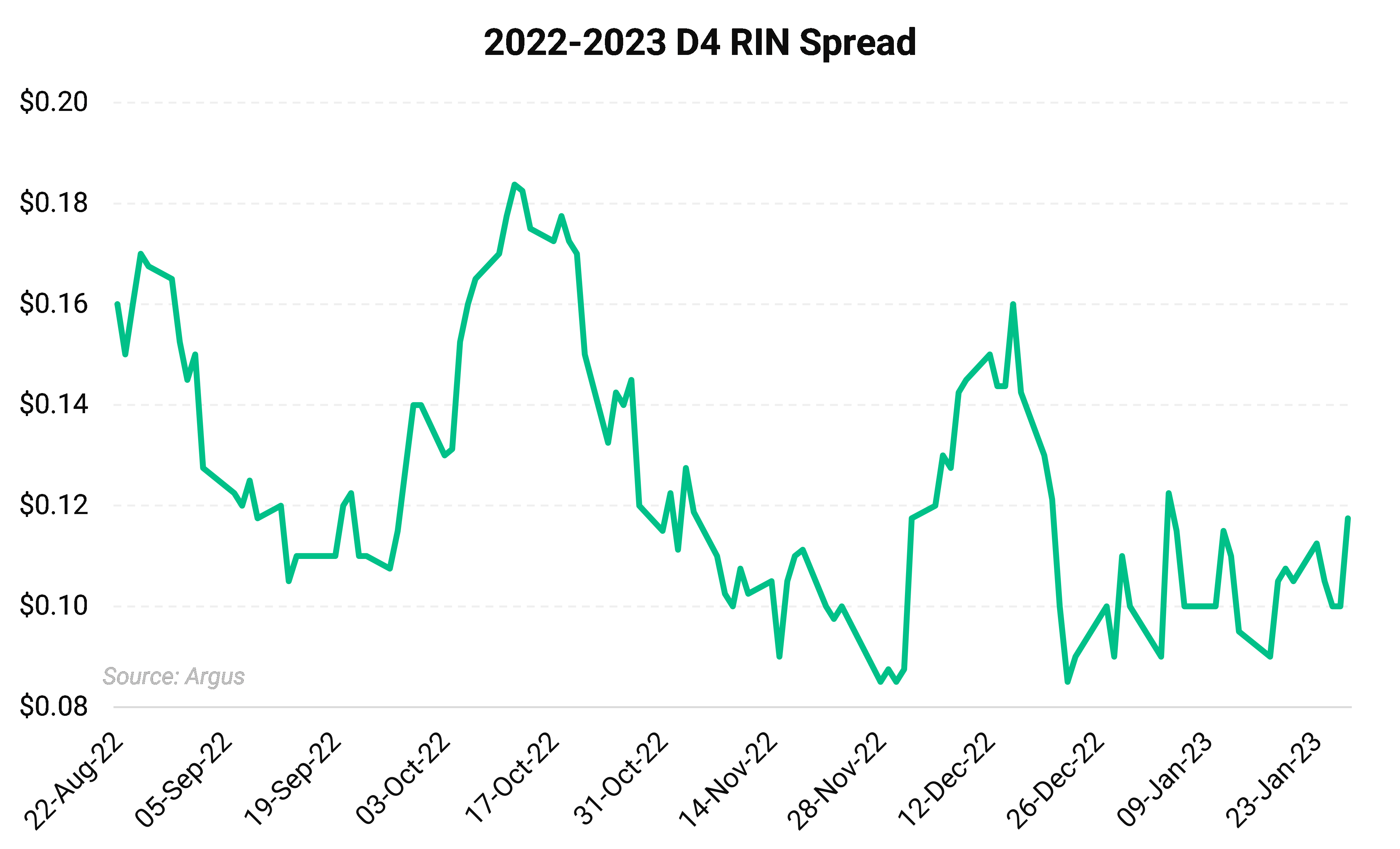

Biomass-based diesel 2022 vintage D4 RINs gained over $0.01/gallon from the week prior, while 2023 gains were more muted. This saw the 2022-2023 D4 spread widen out to just under $0.12/RIN (see below).

D4 RINs are a key component to both RD and BD margins. Each gallon of RD gains 1.7 D4 RINs per gallon, while biomass-based diesel gains 1.5 D4 RINs per gallon. RD produced from more carbon intensive feedstocks like palm oil can generate 1.6 D5 RINs. The ratios are known as equivalence values (EV) as all RINs are all set in ethanol equivalent gallons and then further adjusted to account for the reduction in greenhouse gas emissions using the EV.

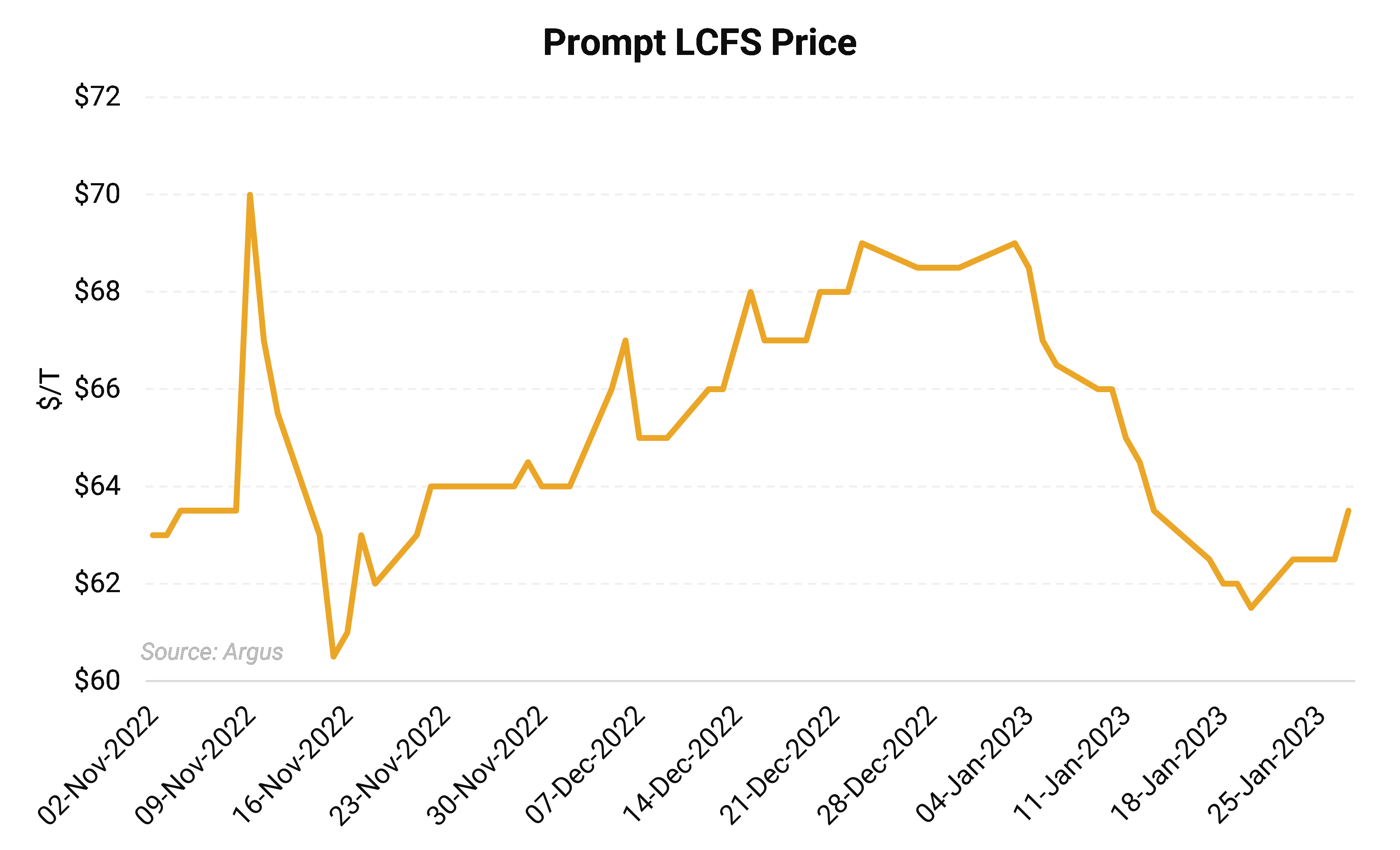

Prompt LCFS markets recovered modestly in thin trade last week reaching as high as $63.50/t for a gain of $0.70/t on average, or 1.1%, from the week prior. This halted a downward trend that began with the start of the new year, bottoming out on January 20 at $61.50 (see below).

LCFS prices have been bearish for the better part of two years as heavy renewable diesel and biodiesel consumption has led to a record surplus of LCFS RINs. Waning demand for gasoline—the only deficit-generating fuel—compounds the structural oversupply of the market.

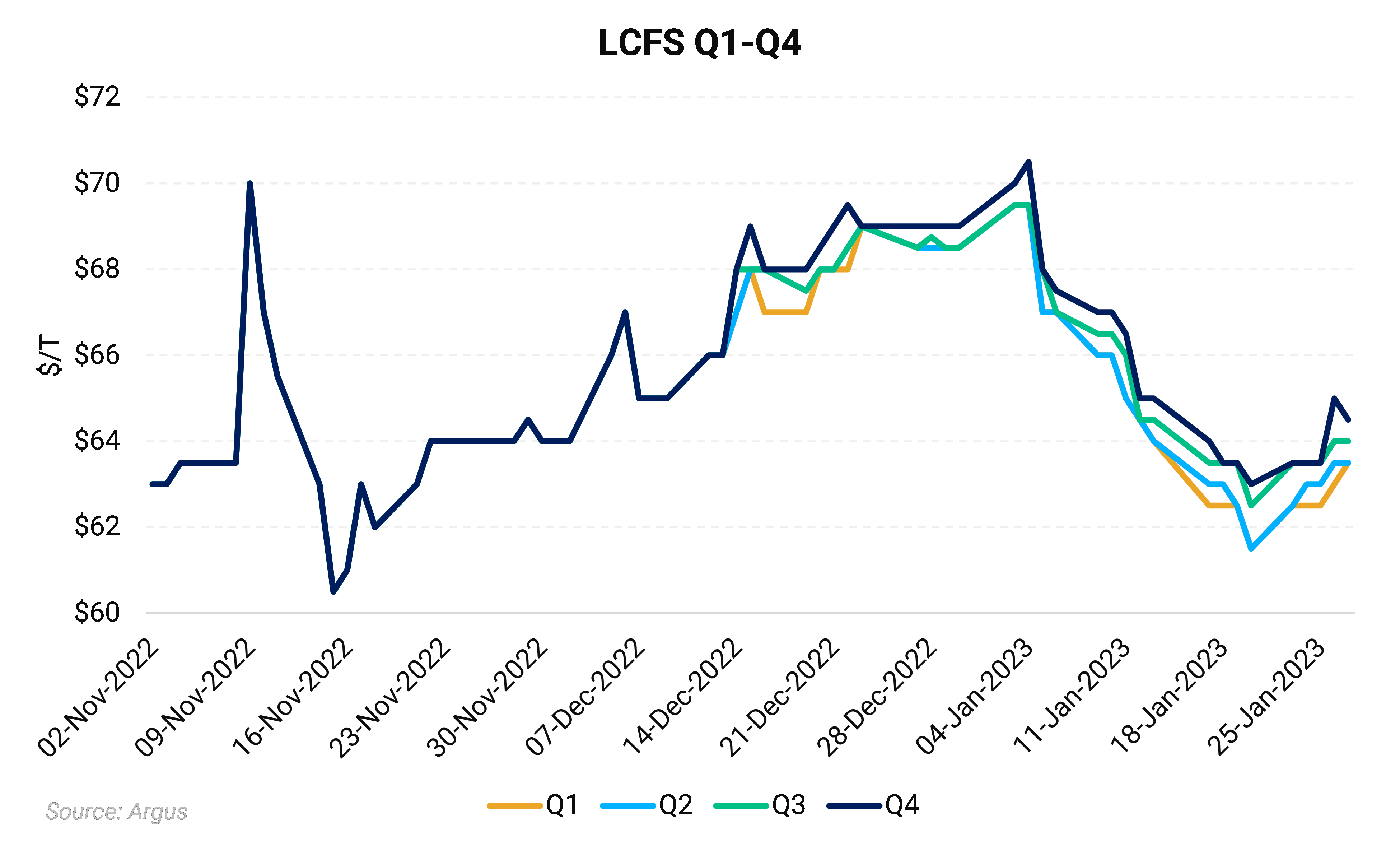

California Air Resources Board (CARB) has been at work on a new scoping plan to be implemented in the first quarter of 2024. The scoping plan would set stricter carbon targets, soaking up much of the oversupply and drawing the program more in line with the reality of the marketplace. The development of the scoping plan has built structure into the forward pricing for LCFS markets, with Q4 transfers pricing at premiums to nearer transfers (see below).

LCFS prices add to margin value for product intended for California, which sets the clearing price for RD fuel in the US and Canada as this is the maximum achievable price for the fuel. California consumes roughly +70% of RD produced in the US for this reason, while additional barrels are sent to Oregon which also has a LCFS. Washington state should soon follow.

The stark LCFS bear market could lower US prices enough to open arbitrages with Europe this year, particularly as the region becomes more diesel starved as Russian product sanctions take effect.

Renewable diesel and biodiesel margins reflect a complex interplay between convention fuels, renewable feedstocks, logistics, environmental credits, and regulatory momentum. With at least 1.8 billion gallons of additional RD capacity slated to come online this year, the need for protection from margin erosion is paramount.

Hedging provides this insurance.

At the same time, established facilities conducting turnaround maintenance can benefit from locking in margins and feedstock costs. Less sophisticated facilities—for example, producers locked into one or two high-cost feedstocks and lacking prime market access—stand to benefit most from AEGIS hedging and advisory functions by achieving the best price possible for their product.

Renewable diesel and sustainable aviation fuel markets remain in revolutionary growth mode. While returns narrow RD and SAF remain the highest returning products in the renewable space, rapid growth and regulatory changes will drive volatility.

AEGIS is here to help harness volatility to lock in predictable gains and prevent losses through innovative hedging strategies.

Important Disclosure: Indicative prices are provided for information purposes only and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee of the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as "edge," "advantage," "opportunity," "believe," or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.