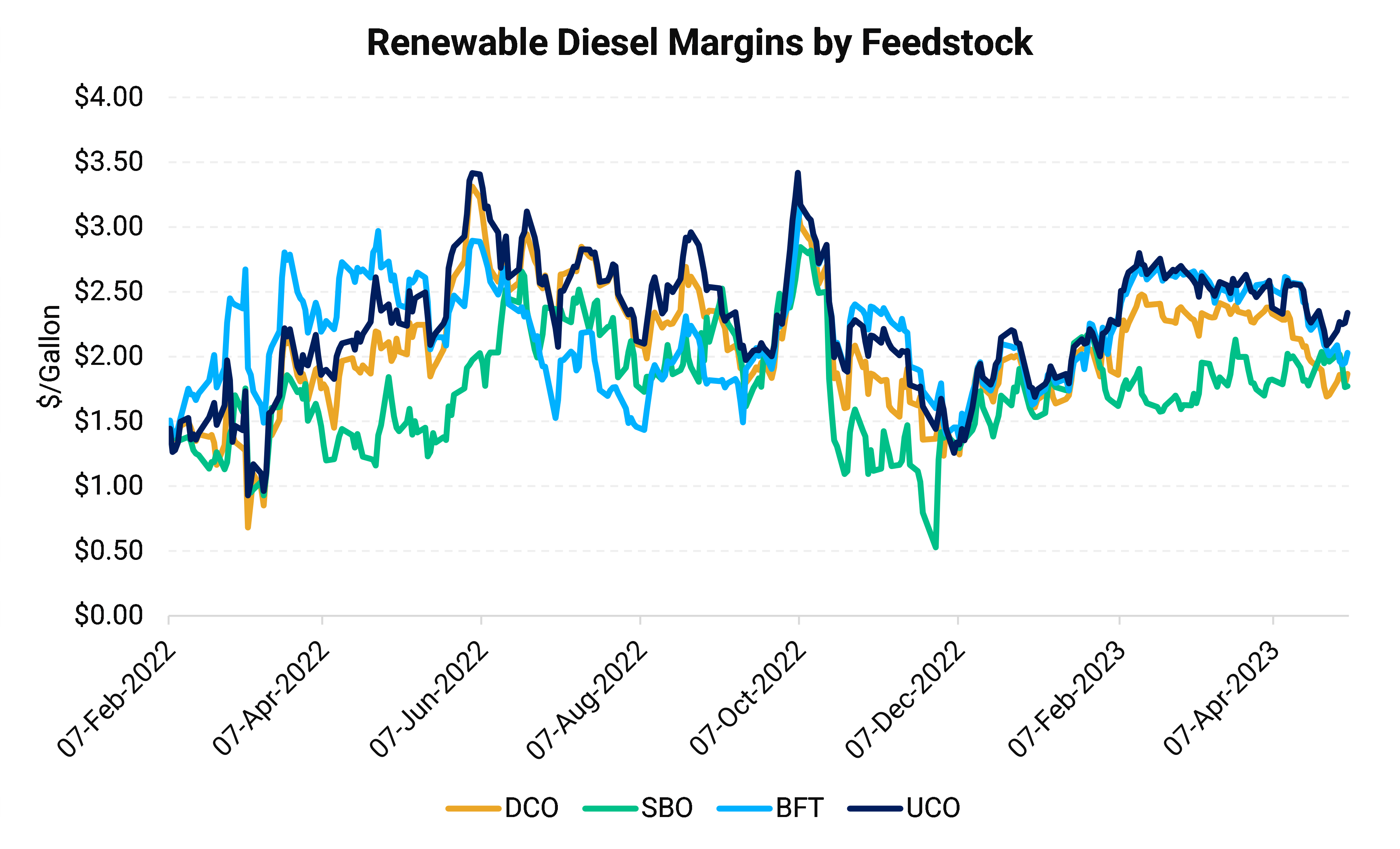

Renewable Diesel Margins Mixed on Persistent Diesel Losses & Credit Strength

US Gulf coast RD margins lacked direction as feedstock prices were mixed amid persistent weakness in Nymex ULSD. A rebound in LCFS supported low carbon intensity (CI) feedstocks, while modest strength in D4 RINs underpinned the margin environment.

UCO margins gained $0.06/gallon, or 2.70%, to average $2.26/gallon, remaining the top returning feedstock. UCO margins reached as high as $2.34/gallon last week, marking a two-week high.

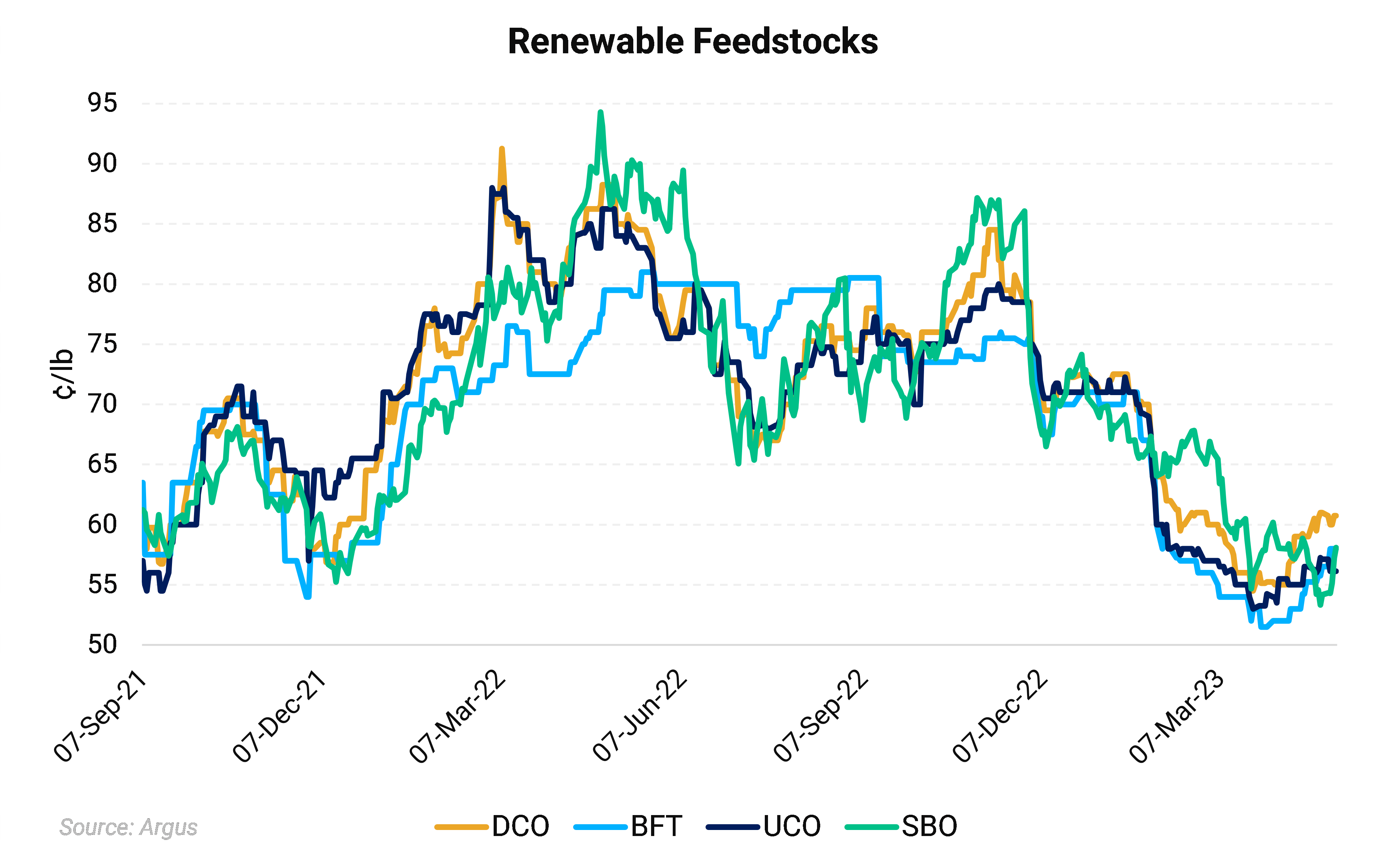

DCO margins gained $0.04/gallon, or 2.09%, to $1.83/gallon, the lowest returning feedstock after weeks of heavy losses. DCO margins remained under SBO returns for a second consecutive week as the feedstock gained 2¢/lb, or 3.59%, on the week.

BFT posted the heaviest losses on the week at $0.13, or 6.11%, yet remained the second highest returning feedstock.

Spot soybean oil margins decline $0.09/gallon to average $1.90/gallon as spot SBO prices posted gains of 1.34¢/lb, or 2.46%, week-over-week.

To recap: The week ended April 28 saw more pronounced losses in RD margins as a continuous uptrend in feedstock prices as met by hefty losses in Nymex ULSD prices. The end of a three-week rally in LCFS credits, alongside weaker RINs failed to limit losses in returns. UCO remained the top returning feedstock despite strong gains across the feedstock arena. Biodiesel margins deteriorated as losses in Nymex ULSD outpaced falling SBO futures.

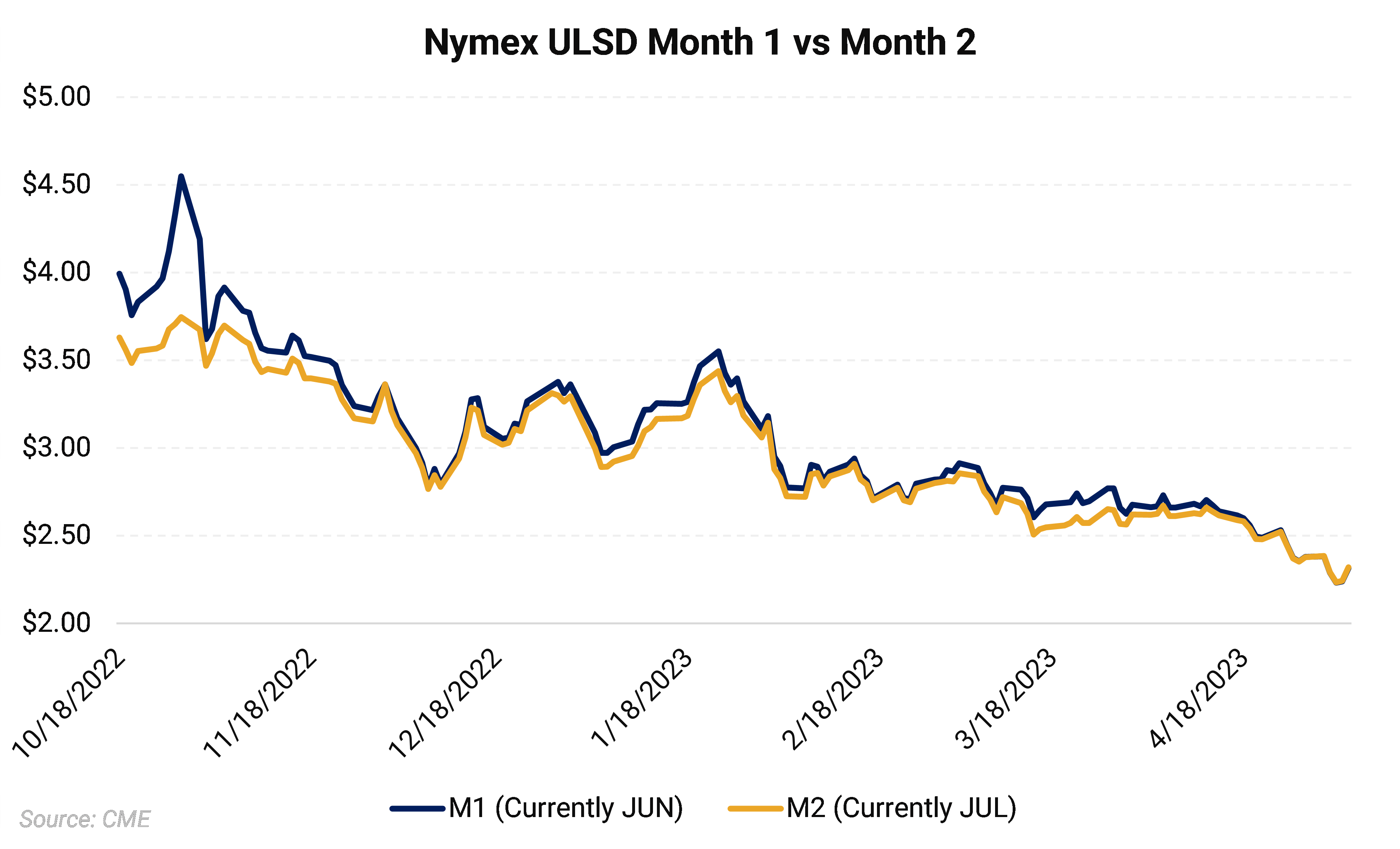

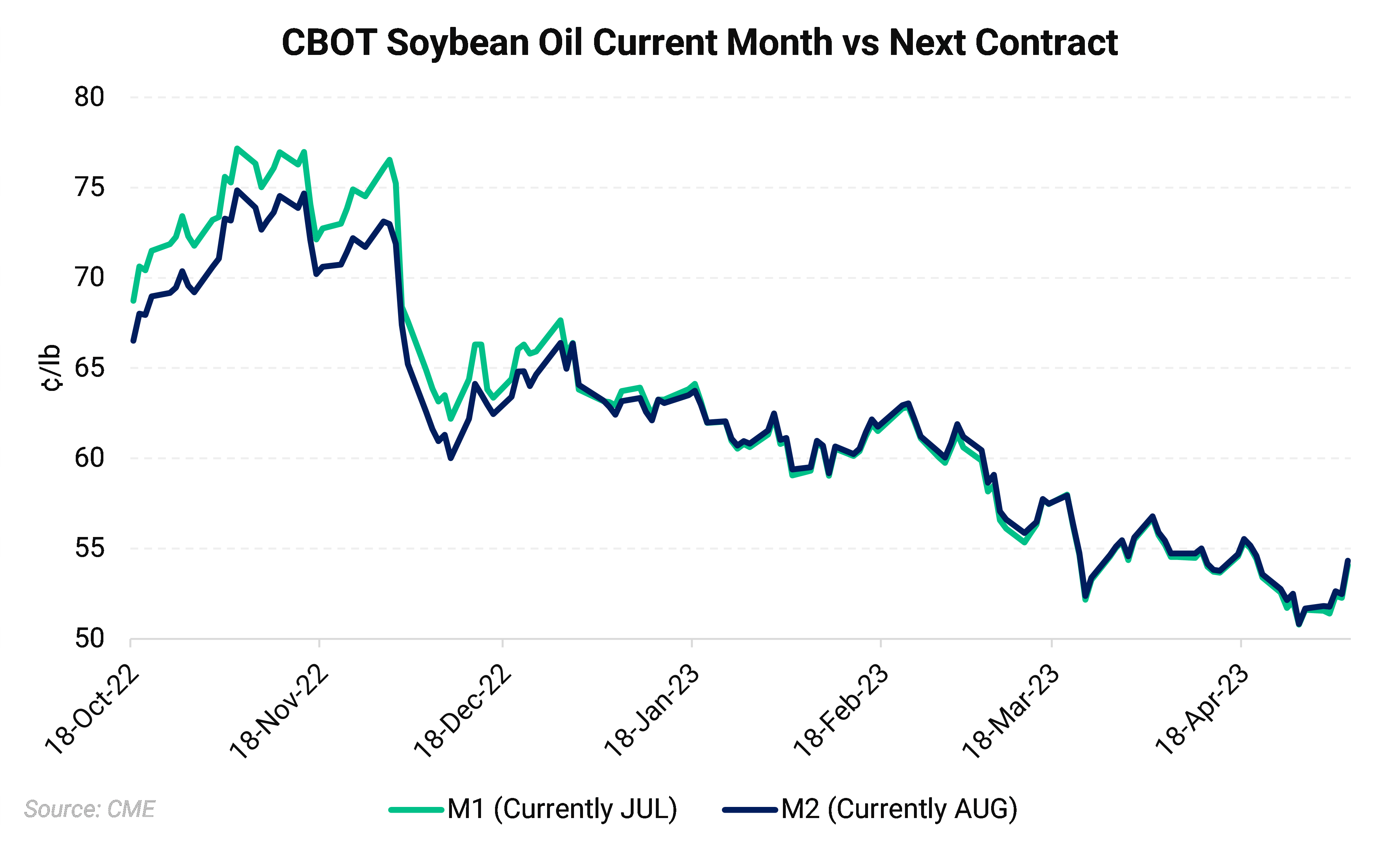

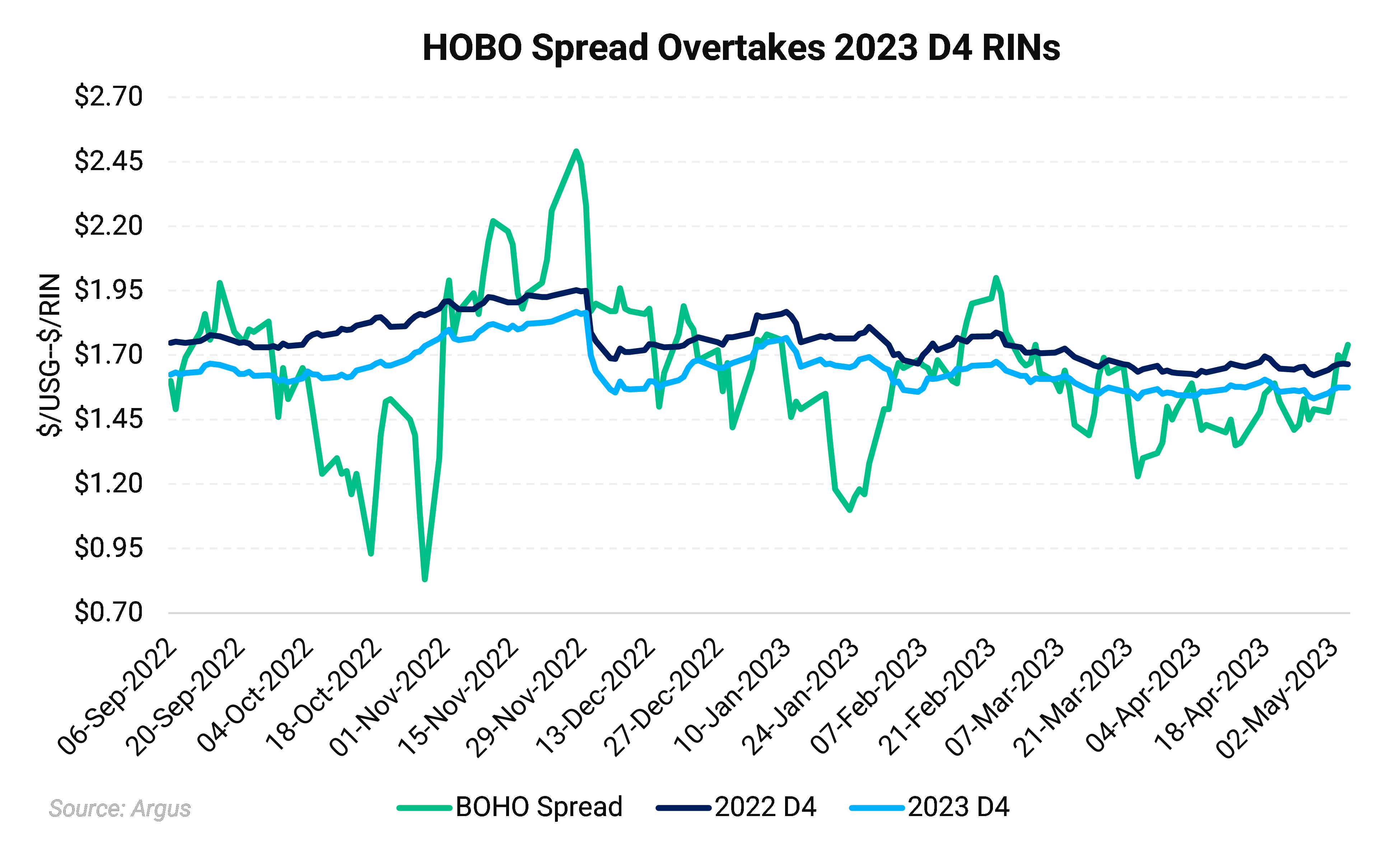

The week ended May 5 saw mixed margins as feedstocks made mixed moves alongside diesel losses. Stronger LCFS prices shored up low-CI feedstock returns, while modest D4 gains underpinned the margin environment. Biodiesel margins deteriorated further as strength in the newly prompt July SBO contract coupled with double-digit losses in Nymex diesel, bringing the BOHO spread to the widest point in over two months.

Biodiesel margins, as measured by the soybean oil-to-heating oil (BOHO) widened $0.17/gallon, or 12%, as fresh losses in the front-month Nymex ULSD contract were met by front-month strength in SBO. The BOHO spread averaged $1.63/gallon last week but reached as wide as $1.74/gallon marking the widest level in over two months.

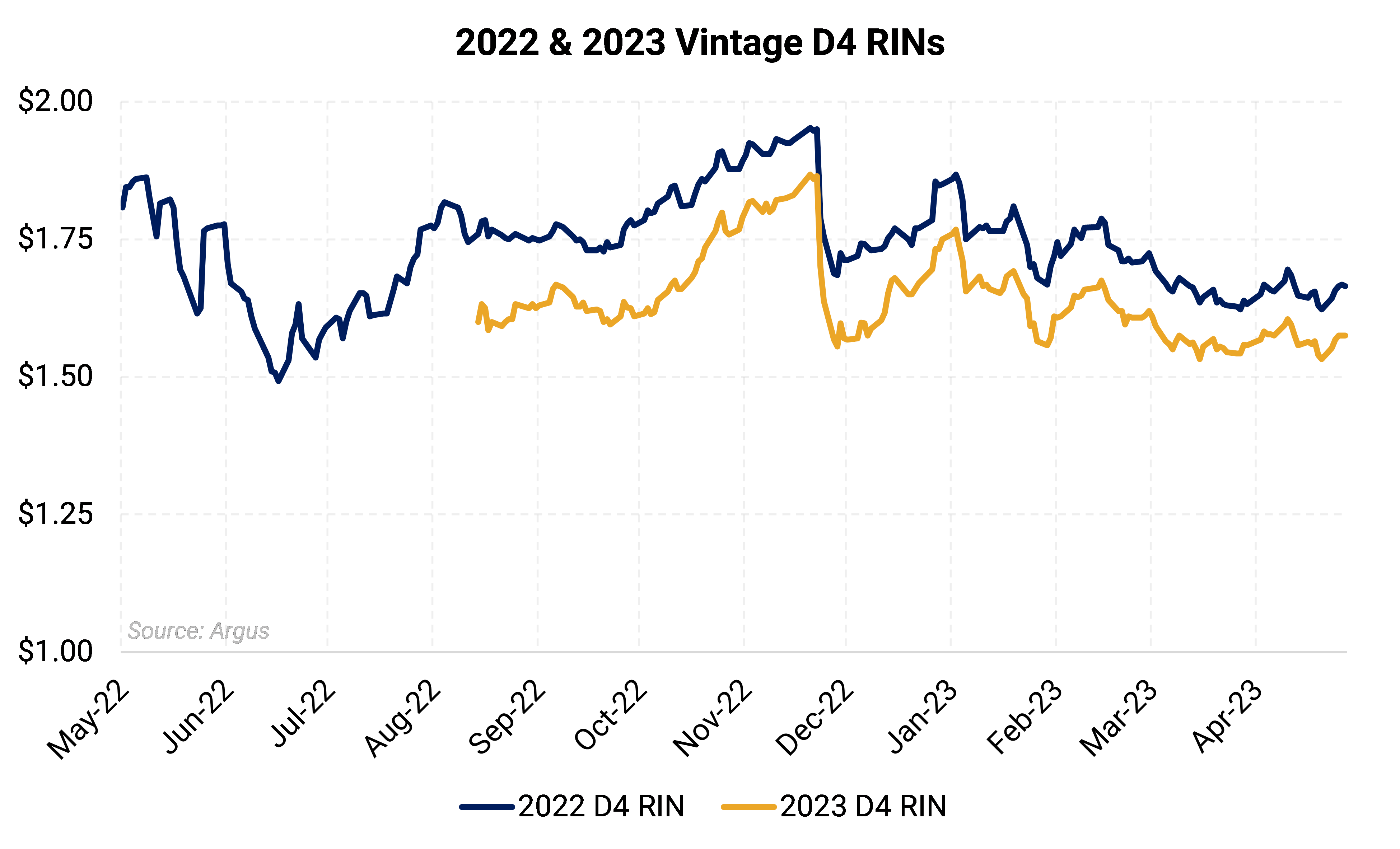

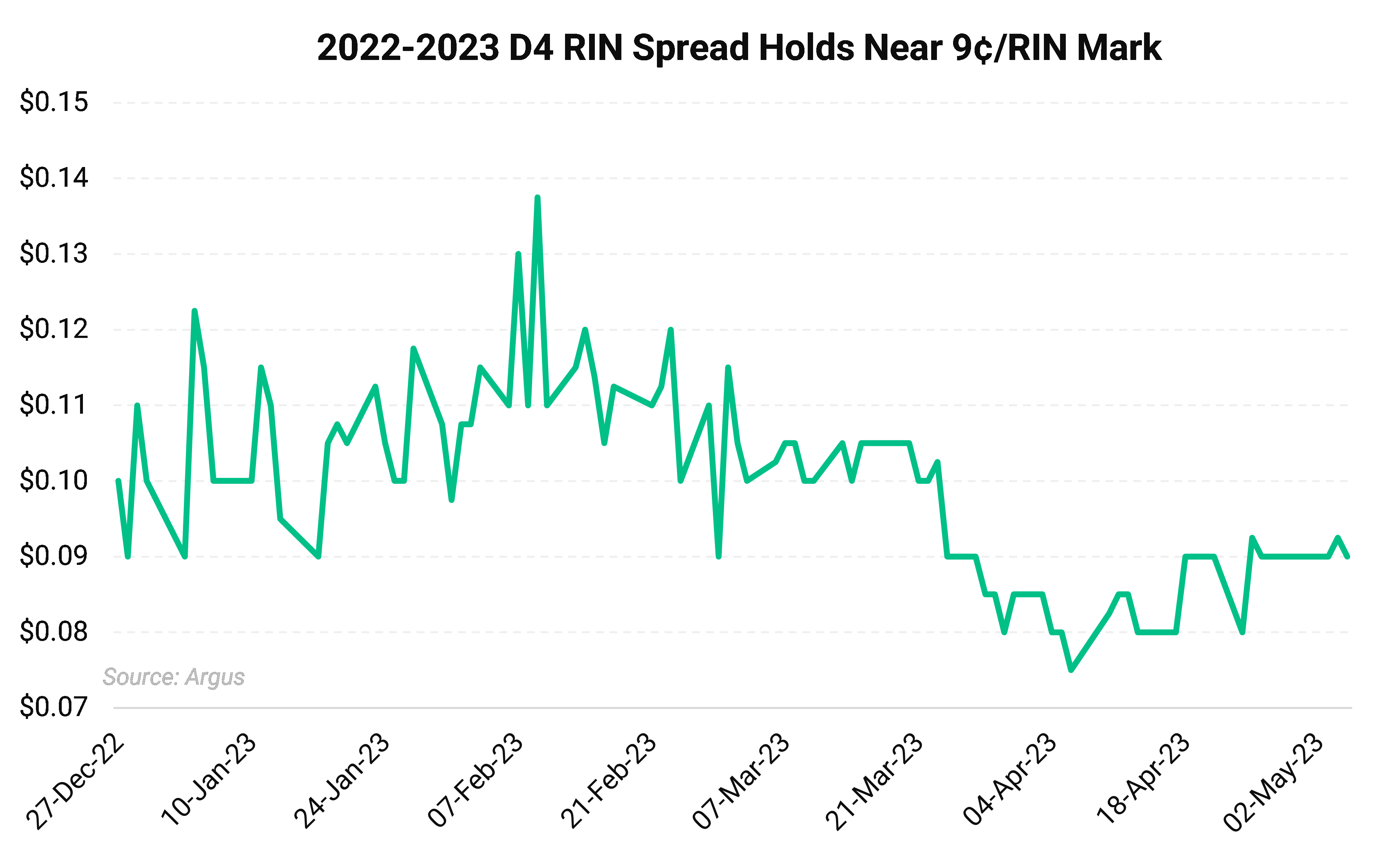

The 2023 vintage D4 RINs gained 1.7¢/RIN over the course of the week, leaving the BOHO spread running nearly $0.17/gallon over 2023 D4 RIN values (see below).

The wider the BOHO spread, the weaker the margin as the main input cost for biodiesel producers, soybean oil, is more costly than the petroleum-based diesel fuel it competes with, compressing margin though the D4 RIN can contribute significantly toward making up for BOHO weakness.

The BOHO spread is a simplistic breakdown of the pulse of the biodiesel industry and is in widespread use by the industry. The BOHO spread does not account for operational costs which can vary drastically from plant to plant, nor the additional margin value afforded by credits and/or the sale of byproducts such as glycerin.

D4 RIN prices recovered a modest 1.7¢/lb, or 1.07%, as buying returned to the marketplace for the first time in over half a month. The market is still largely in a holding pattern awaiting a mid-June deadline for the finalization of the EPA’s set rule, while the weeks leading up to the announcement are likely to see press leaks and rumors stir up market activity.

EPA Administrator Michael Regan issued comments at a House Agriculture Committee hearing last week indicating the EPA is likely to cave to both industry and lawmaker pressure to increase the advanced biofuel mandate in the final ruling expected in June.

News that United Refining was denied its SRE hardship waiver by the Third Circuit court added bullish undertones to the RIN complex as the move adds additional demand to the marketplace. Trade organization Growth Energy entered comments in support of enforcing SREs in its case against the EPA. A full denial of all SREs would represent more than 1.6 billion RINs.

Prior to this month’s moves, the approval by a federal court of a SRE for Calumet Special Products 30,000 b/d refinery in Montana provided bearish undertones to RIN markets.

SREs were carved out in the Renewable Fuel Standard (RFS) for refiners producing 75,000 b/d or less which could prove compliance with the RFS—i.e., purchasing RINs—resulted “undue economic hardship.”

The EPA retroactively overturned 69 Trump-Era SREs starting in April of last year by denying 31 SRE waivers for 2018 and then denying all SRE petitions for 2016 through 2020. Denying SREs is bullish for RINs markets as refiners must enter the marketplace to purchase RINs to cover compliance obligations which were originally waived.

A court ruling earlier this month halted compliance obligations for two refineries with existing SRE petitions taking issue with the retroactive nature of the SRE denial.

If approved the SRE ruling will prove very bearish for the wider RIN marketplace as participants will view the decision as a shift in the EPA’s approach to granting SREs. Notes from the court were strongly in favor of granting the SREs, as the court made it clear it intends to handle SREs as originally intended by the RFS—i.e., waive RFS compliance if undue hardship can be demonstrated—and to allow waivers which were issued in an “unlawful retroactive application.”

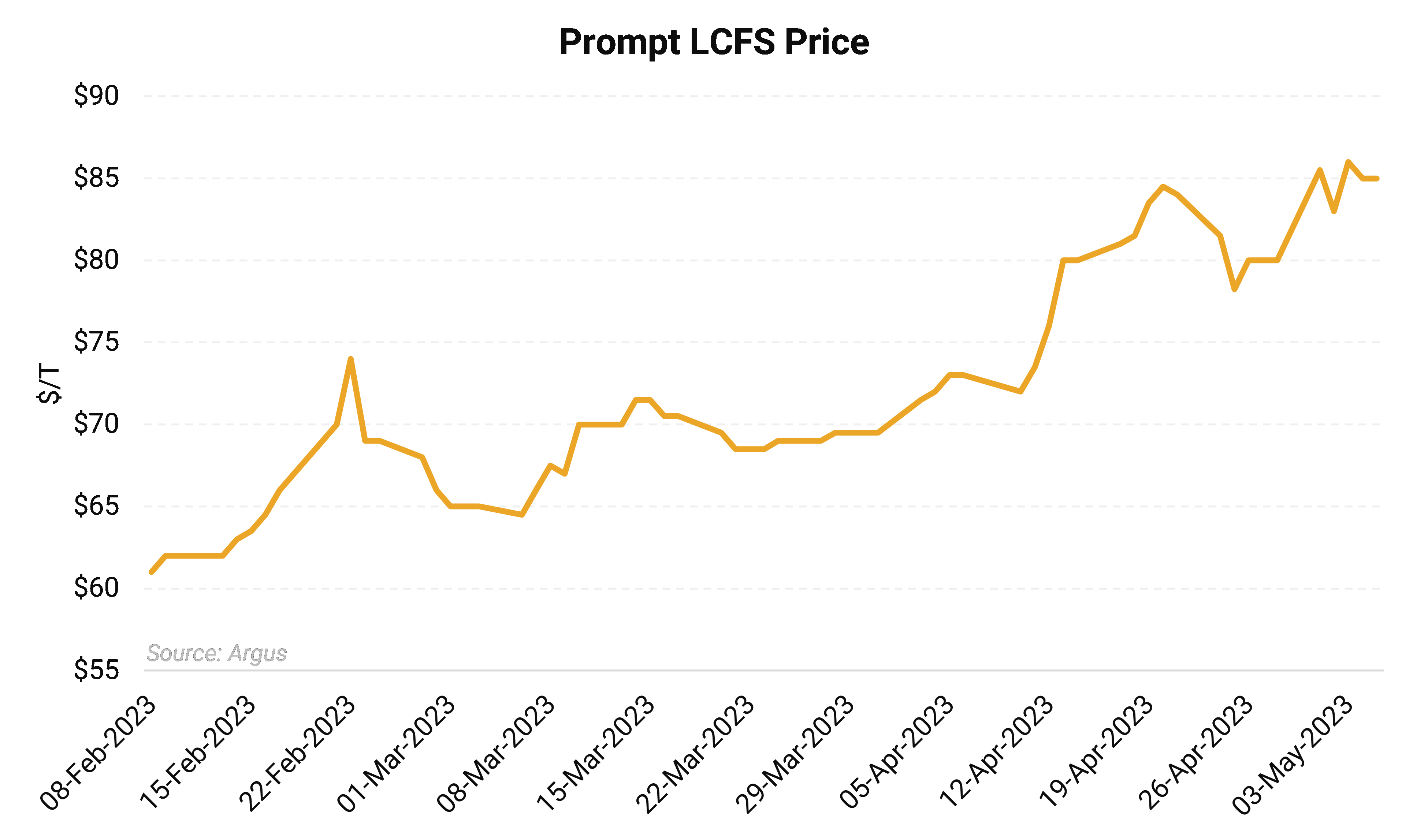

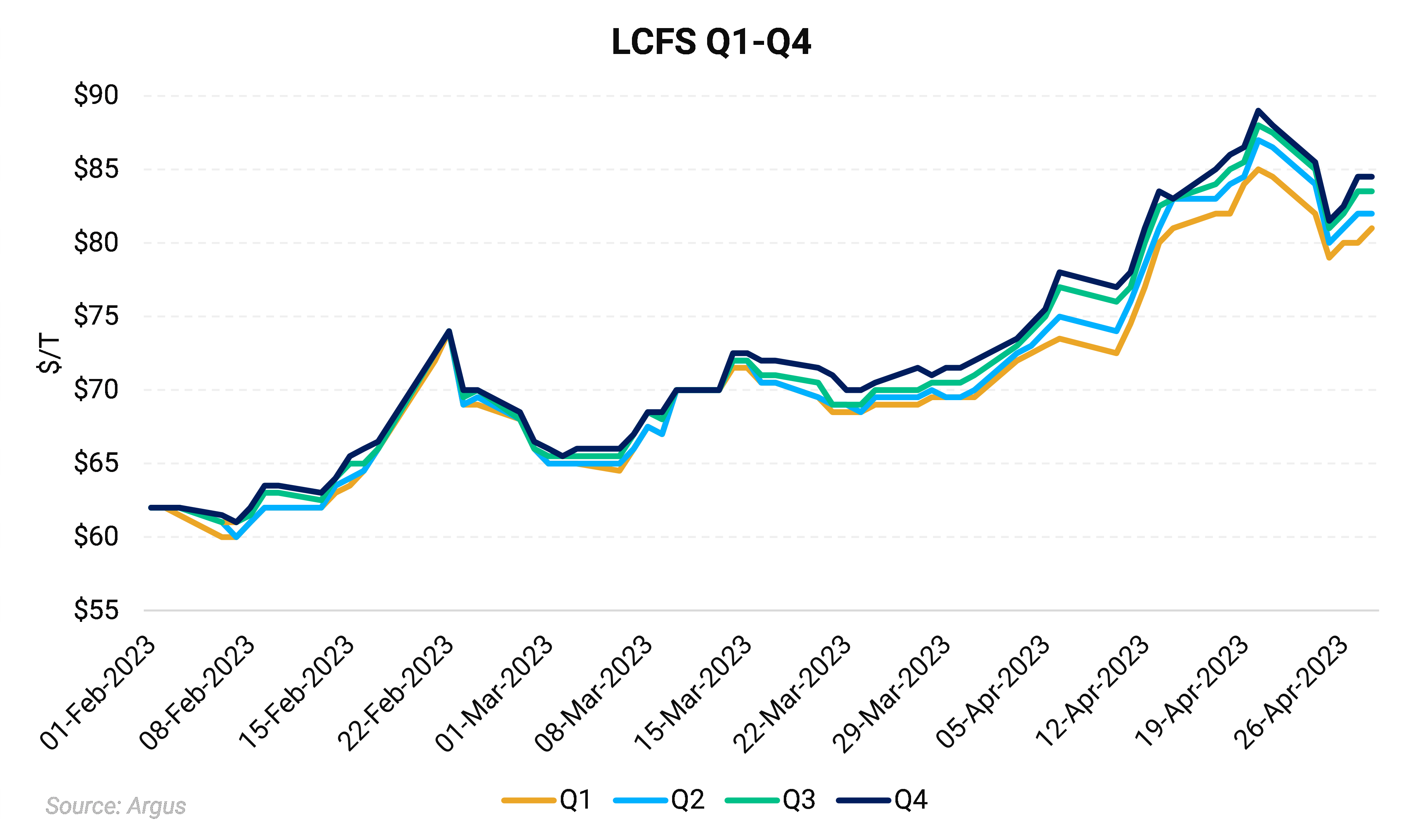

The California Low Carbon Fuel Standard (LCFS) market rebounded following last week’s pause. Prompt credits rose $4.95/t, on average last week. LCFS strength has been driven by trader buying and strength in futures markets as the credits become more attractive options ahead of the California Air Resource Board’s new, more stringent scoping plan.

The forward structure remained in contango, yet some carry rolled out of the spot market late in the week (see below).

LCFS prices add to margin value for product intended for California, which sets the clearing price for RD fuel in the US and Canada as California RD represents the maximum achievable price for the fuel. California consumes roughly +70% of RD produced in the US for this reason, while additional barrels are sent to Oregon which also has a LCFS program in place. Washington state credits have begun trading, with back-half 2024 WCFS credits valued around $105/t.

Renewable diesel and biodiesel margins reflect a complex interplay between conventional fuels, renewable feedstocks, logistics, environmental credits, and regulatory momentum. With at least 1.8 billion gallons of additional RD capacity slated to come online this year, the need for protection from margin erosion is paramount.

Hedging provides this insurance.

At the same time, established facilities conducting turnaround maintenance can benefit from locking in margins and feedstock costs. Less sophisticated facilities—for example, producers equipped to run only one or two high-cost feedstocks and lacking prime market access—stand to benefit most from AEGIS hedging and advisory functions by achieving the best price possible for their product alongside feedstock optimization strategies.

Renewable diesel and sustainable aviation fuel markets remain in revolutionary growth mode. The US Energy Information Agency projected RD capacity could more than double through 2025.

While returns narrow RD and SAF remain the highest returning products in the renewable space, rapid growth and regulatory changes will drive perpetual volatility.

AEGIS is here to help harness volatility to lock in predictable gains and prevent losses through innovative hedging strategies.

Important Disclosure: Indicative prices are provided for information purposes only and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee of the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as "edge," "advantage," "opportunity," "believe," or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.