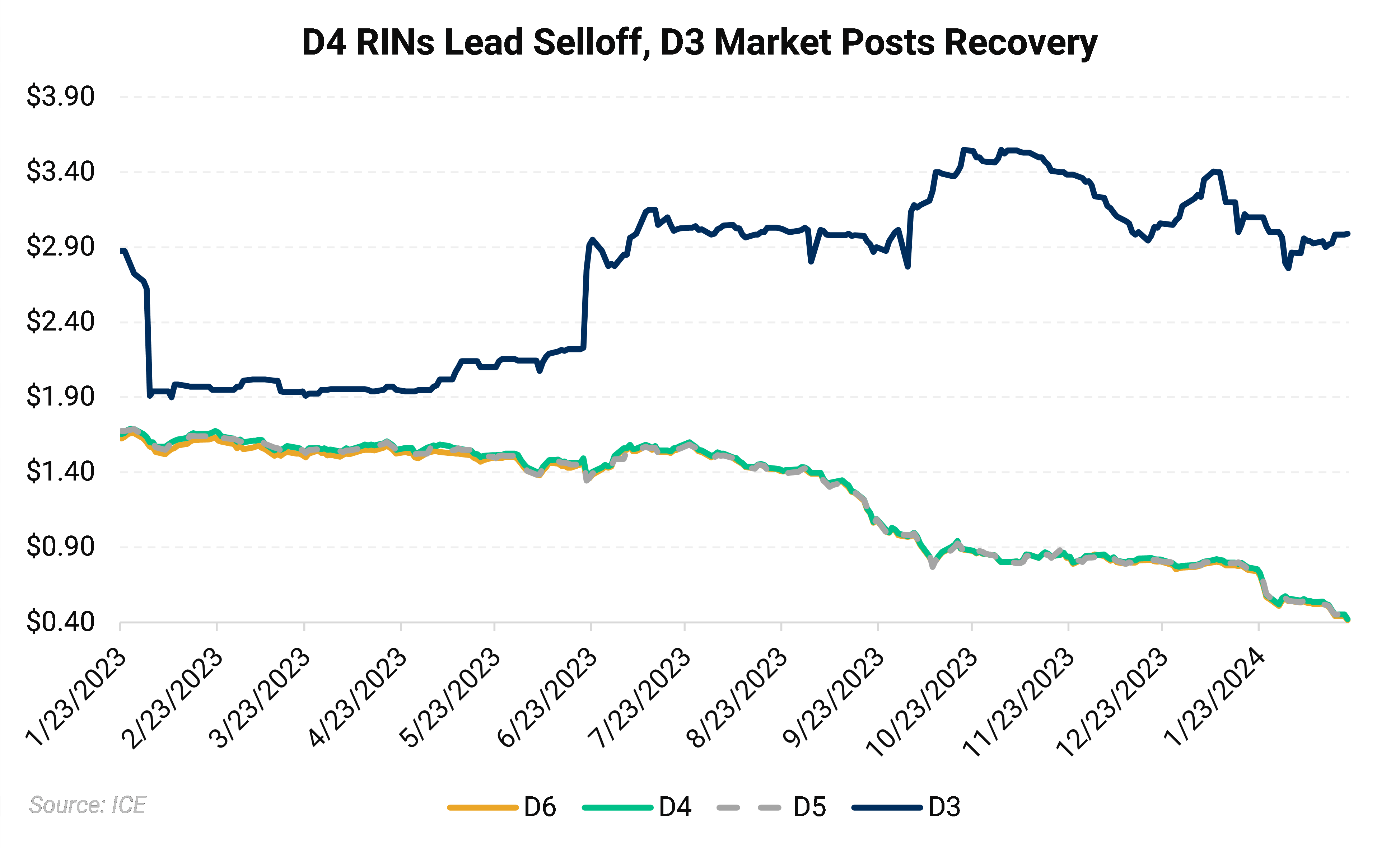

RIN prices tumbled to the lowest levels in over four and a half years as robust January D4 production and expanding renewable diesel capacity drove heavy selling. D4 prices shed nearly a quarter of their value over the course of the first three weeks of February, with the D6 market posting identical losses. The D4 market has lost 46% of its value since the start of the year.

Margins failed to keep pace as diesel strength sputtered out in the second week of February and losses in RIN markets failed to abate. Diesel strength peaked on February 9, which saw the soybean oil-heating oil (BOHO) return to $0.58/gallon—a four-year low briefly reached in late January. A narrower BOHO spread implies stronger biodiesel margins, which is bearish the D4 RIN all else equal.

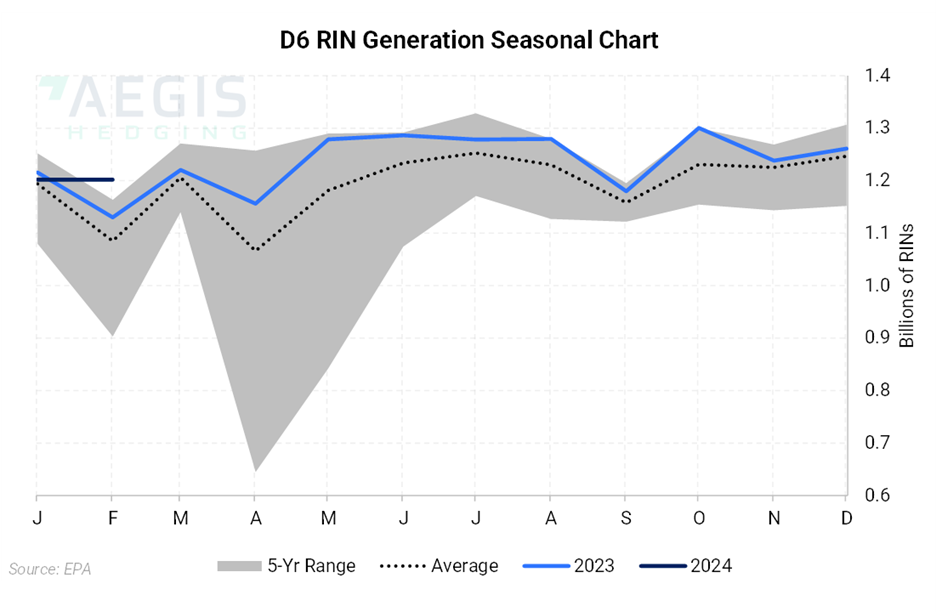

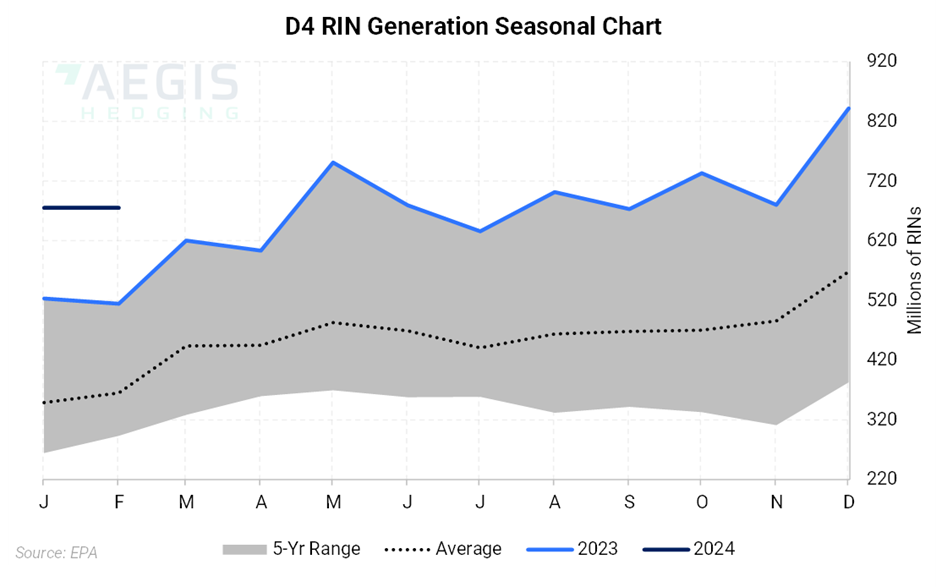

The February 15 release of January 2024 RIN generation showed 1.89 billion credits generated, down 16% from the previous month’s record of 2.17 billion credits but up nearly 8% on prior year levels. A 29% increase in D4 generation accounted for the bulk of the year-over-year gain. D4 generation accounted for nearly 36% of all credits generated during the month of January, down from 39% the month prior.

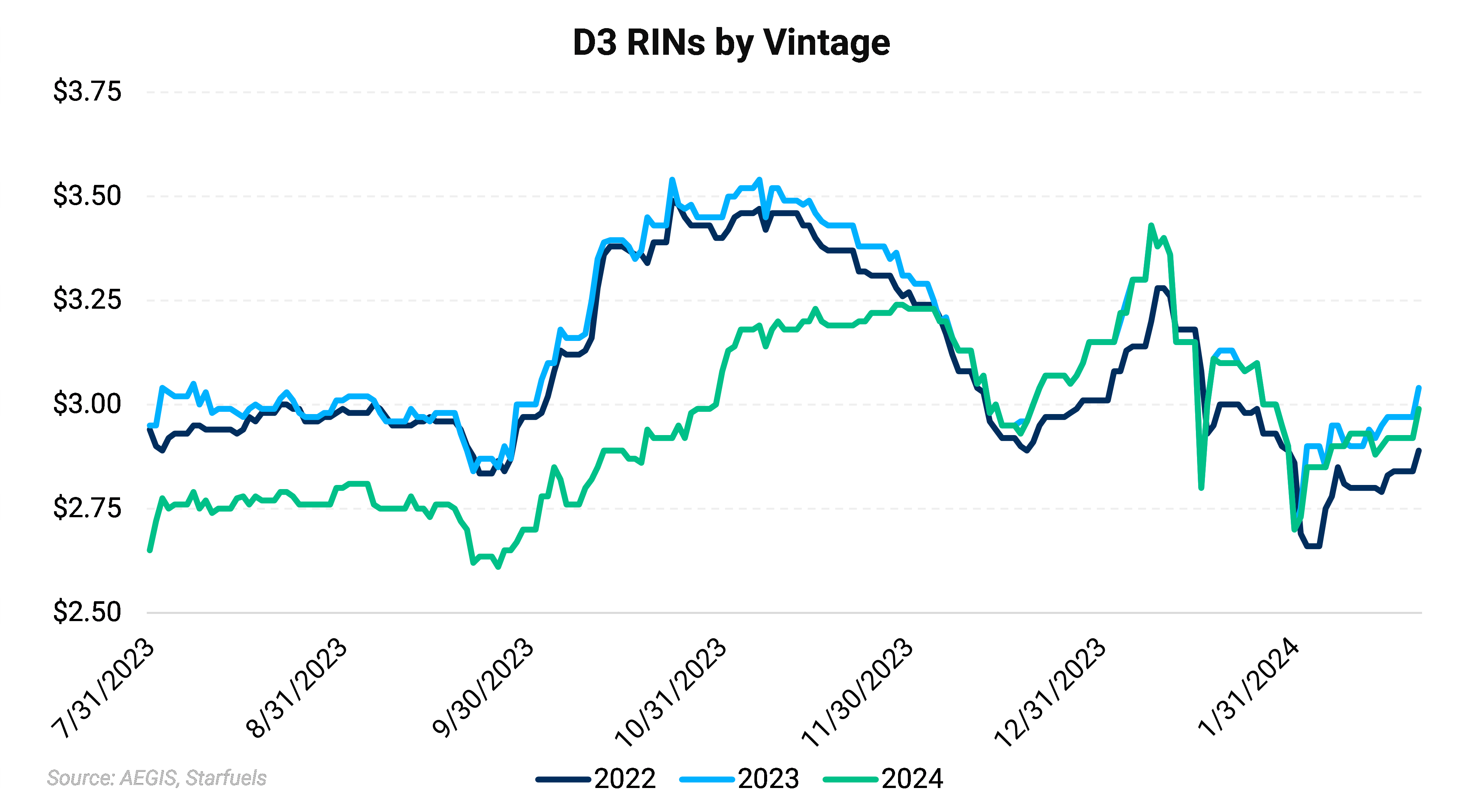

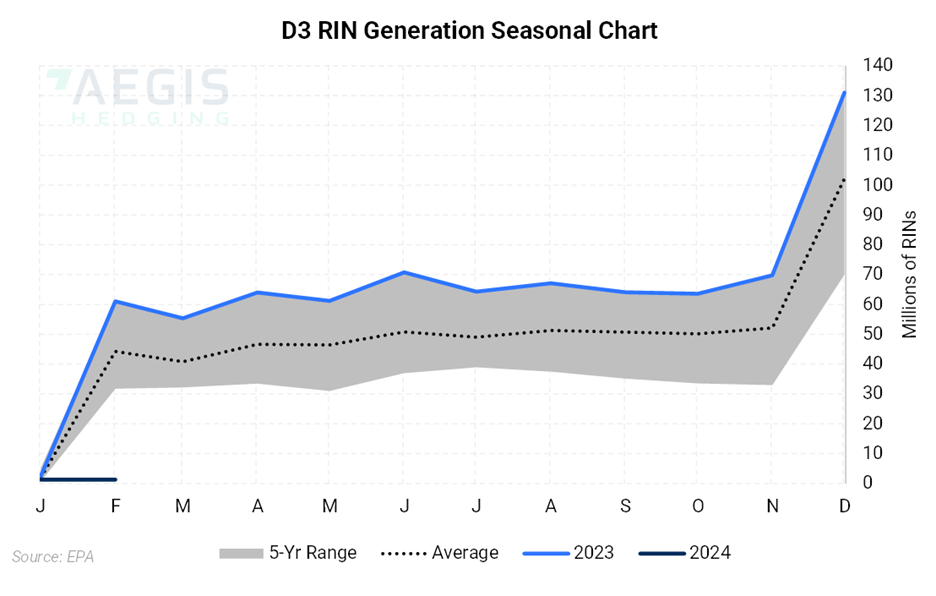

The D3 market halted a two-month selloff which saw prices reach as low as $2.74/RIN as fresh EPA data showed total 2023 D3 and D7 generation more than 773 million credits, or 8%, short of the mandated 840 million gallons. The shortfall increases the likelihood that the EPA will need to turn to its waiver authority and issue Cellulosic Waiver Credits (CWC) for 2023.

Insufficient RIN generation and the lack of a Cellulosic Waiver Credit (CWC) had been supporting the 2023 market, yet the market began to price in the increased likelihood of deferred 2023 compliance and increasing expectations of a CWC. While the EPA could act as soon as Q3, AEGIS views it unlikely the EPA will address this matter until after the election.

- January total RIN generation came in at 1.89 billion credits, down 16% from the previous month’s record 2.17 billion credits, but up nearly 8% on year-ago levels.

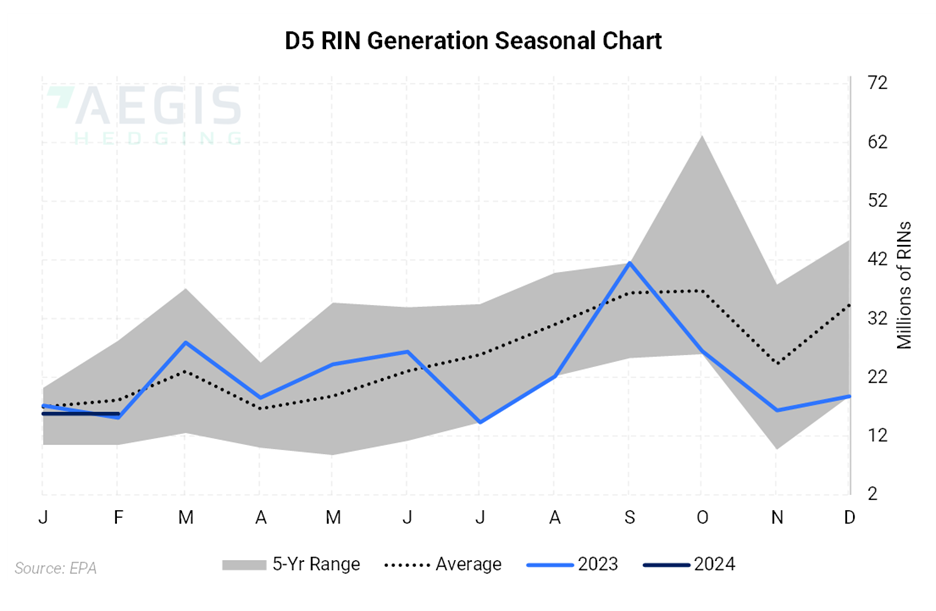

- D4 generation retreated to 675 million credits, down nearly 20% from the previous month’s record 840 million credits, yet up 29% on year-ago levels. Domestic renewable diesel production accounted for 56% of total D4 output, up from 54% the month prior. Domestic renewable diesel production accounted for 49.5% of total D4 output in November and 47% in October. Foreign renewable diesel production made up 6% of total D4 generation down from 9.7% from the previous month and 11% in November. Domestic and imported biodiesel accounted for 36% of the January total, up from 35% the month prior, but down from 39% in November and 41% in October. A record 15 million D4 credits were generated across domestic and foreign SAF production, accounting for 2.2% of the January total. Foreign SAF accounted for 91% of total SAF credits.

- D3 and D7 RIN generation totaled 1.3 million credits of which the bulk represent 2023 vintage credits due to delays from book and claim. Total cellulosic RIN production came in at 774.8 million credits, 65 million credits, or 7.7%, short of the final cellulosic mandate. The EPA used an aggressive 25% growth rate to set the 2023 final cellulosic mandate.

- January RIN generation data housed a minor upward revision to 2022 D6 generation for the month of December totaling 255,368 credits. The prior month saw minor upward revision to 2022 and 2023 D6 totaling 198,203 credits from November 2022 and January 2023.

- D4 RIN upward revisions totaled 1,321,353 spanning from May 2022 through December 2023. May 2022 generation was revised higher by 113,279 credits, while 2023 upward revisions totaled 1,208,074, with December accounting for 97% of the total. The month prior saw D4 RIN generation for the month of November 2023 revised 42,204 higher.

- D5 upward revisions totaled 3,622,169 spanning from September 2022 to December 2023. The month prior saw D5 generation revised 4,439,893 higher.

- D3 upward revisions totaled 70,498,439 credits ranging from December 2022 through December 2023. December 2023 was revised 70,478,217 higher, accounting for preponderance of the gain.

- The EIA trimmed its 2024 and 2025 renewable diesel production and consumption forecasts. US production was projected at 226,000 Bbl/d in 2024, down 1.3% from the December outlook. EIA trimmed its 2025 production outlook by 1.4% to 290,000 Bbl/d. Demand for 2024 was projected at 249,000 Bbl/d, down 1.2% from the previous month’s estimate, while 2025 demand was cut by 1.6% to 304,000 Bbl/d. RD imports for 2024 are estimated to average 24,000 Bbl/d, up 4.3% from December projections, while imports for 2025 were unchanged at 14,000 Bbl/d.

- EPA Fuel Program Center Director, Paul Machiele, said the oversupply of D4 credits is not currently a concern at the EPA as the agency’s primary driver in setting the 2023-2025 mandates was feedstock availability, according to Carbon Pulse. Machiele noted that the surge in imported feedstock was not taken into account when considering the final Set Rule, speaking at the OPIS RFS, RINs and Biofuels Forum in Chicago. Changes to exiting mandates are unlikely to be taken up during an election year. President of Advanced Biofuels Association, Michael McAdams, cited an unnamed source that the earliest the EPA would take action is 2026.

- EPA officials indicated that the next opportunity for addressing the adoption of the contentious eRIN pathway would be when the agency considers blending targets for 2026, according to EPA Fuel Programs Center director Paul Machiele when speaking at the Argus North American Biofuels, LCFS, & Carbon Markets Summit in mid-September.

Calendar:

- January 31, 2024: Three-year Registration Update

- March 31, 2024: EPA Expected Deadline for 2023 Compliance

- June 1, 2024: Attest Engagement Reporting Deadline for 2022

- March 31, 2025: EPA Expected Deadline for 2024 Compliance

Relevant News:

- The Biden administration is set to announce more stringent greenhouse gas modeling for corn-based ethanol, which will cut potential credit value for ethanol and ethanol-to-SAF, according to Reuters. The adjustment to the Department of Energy’s GREET model aims to ensure crediting for farming practices which reduce environmental impact like cover crops and no-till farming. A bipartisan letter urged the Biden administration to issue SAF guidance by the March 1 deadline.

- PBF reported 12,000 BBl/d of RD production during the fourth quarter 2023, down from 17,000 Bbl/d in the third quarter due to a catalyst change. St. Bernard Renewables (SBR) is a 50:50 joint venture with Italian major ENI located at PBF’s Chalmette, Louisiana, refinery. The facility has a nameplate capacity of 20,000 Bbl/d, meaning SBR was running at just 60% of capacity during the fourth quarter.

- Diamond Green Diesel’s Q4 operating income fell by 68% amid lower RD margins. RD sales averaged 3.8MM gal/d in Q4 2023, up 52% from the same period last year. Valero said its 470MM gal/y Port Arthur SAF expansion is on schedule for completion by Q1 2025.

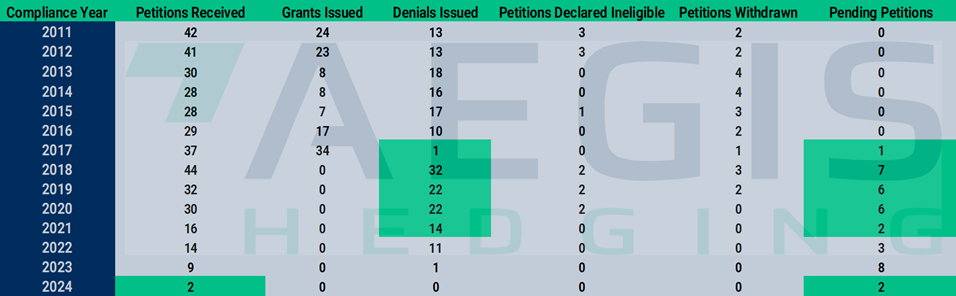

- The 5th US Circuit Court of Appeals turned down a request to reconsider its November 22, 2023, decision to block SRE denials for six small refineries. Biofuel industry groups Growth Energy and Renewable Fuel Association sought a rehearing on the grounds that the denials should be brought before the DC Circuit Court. The EPA has received 12 SRE petitions since the 5th Circuit’s November ruling.

- The US Court of Appeals for the 11th Circuit dismissed a SRE challenge by Hunt Refining on January 11, saying the case should be heard by the US Court of Appeals for the DC Circuit. Biofuel industry group Growth Energy welcomed the decision as CEO Emily Skor responded “EPA’s denials of these SRE petitions were ‘nationally applicable’ and have nationwide effect, and challenges to the denials should only have been brought in the DC Circuit.”

- The 5th US Circuit Court of Appeals ruled to block denials of SREs for six refineries on November 22, 2023. The SREs cover Calumet’s 57,000 Bbl/d Shreveport, Louisiana refinery, Placid Refining’s 75,000 Bbl/d Port Allen, Louisiana refinery, Ergon Refining’s 26,500 Bbl/d Vicksburg, Mississippi refinery, Ergon’s 23,000 Bb/d West Virginia refinery, CVR’s 74,500 Bbl/d Wynnewood, Oklahoma refinery, and Allegiance Refining’s 21,000 Bbl/d San Antonio refinery. The court’s decision said the EPA’s blanket SRE rejection was “impermissibly retroactive; contrary to law; and counter to the record evidence.” The decision will add a bearish undertone to an already oversupplied marketplace, save for D3 credits.

- The US Treasury Department issued guidance on December 15, 2023, clarifying how SAF will be eligible for tax credits worth as much as $1.75/gallon under the Inflation Reduction Act. The SAF tax credit is only issued to fuels which reduce lifecycle GHG emissions 50% below petroleum-derived jet fuel. The Treasury Department plans to calculate emissions intensity using a modified version of the GREEET model planned for March 1, 2024. The adjusted GREET model could open the door for corn-based ethanol to contribute to SAF supply.

- California postponed a hearing on proposed LCFS amendments originally scheduled for March 21. CARB aims to hold a workshop in April. The 45-day public comment period is still scheduled to conclude on February 20. The move comes after the state’s Environmental Justice Advisory Committee (EJAC) urged the Board to delay its LCFS vote until July 2024 as the current plan relies too heavily on biofuels and out-of-state biogas.

- Recent fires at Marathon’s Martinez refinery triggered a federal investigation by the Chemical Safety and Hazard Investigation Board (CSB). Fires on November 11 and November 19 at a hydrodeoxygenation (HDO) unit led to spills of RD. Marathon aims to achieve 48,000 Bbl/d of production at its Martinez, California facility by year-end.

- Federal judges defended the EPA’s approach to setting the 2020-2022 blending mandates. US refiners have complained blend requirements were too high based on how the EPA adjusted blending targets to account for projected Small Refinery Exemptions (SREs). The EPA is also facing a separate lawsuit for its 2022 cellulosic biofuel requirement, with biofuel groups arguing that targets were set too low based on projections of actual production and not accounting for the availability of carryover credits for compliance. Refiners have also filed a series of lawsuits in the DC Circuit court challenging the EPA’s move to reject all outstanding SREs this year.

- Calumet plans to add 3,000 Bbl/d of capacity to its 15,000 Bbl/d, Great Falls, Montana Renewables refinery by 2025. The Great Falls plant is currently undergoing repairs to a steam recovery system and moved forward a turnaround originally planned for 2024 to November. Calumet is mulling plans to ultimately maximize SAF production at the Great Falls facility.

RIN markets fell to the lowest levels in over four and a half years, with D4 and D6 RINs tumbling 24% and 23% respectively over the course of February. D4 RINs have shed 36c, or 46% since the start of the year.

Renewable diesel margins shed between 25-39c, or 11-28%, month over month as diesel turned bearish in the second week of the month and RIN losses persisted. UCO remained the strongest returning feedstock at $2.17/gallon by months close, followed by BFT markets at $1.54/gallon. SBO margins dipped under the $1.00/gallon mark several times, reaching $0.99/gallon by February 20, down 28% over the course of the month.

Diesel strength early in the month saw the soybean oil-heating oil (BOHO) spread to return to $0.58/gallon on February 9—a four-year low briefly reached in late January. Diesel turned downward the following session driving the BOHO spread to $0.67/gallon, up by 9c/gallon, or 16% over the course of just six trading days. RIN markets refused to respond to a wider BOHO spread, sagging under the weight of mounting supply, 2024 RD capacity additions, and viable margins. D4 RINs shed 13.25c, or nearly 24% over the first three weeks of February. A narrower BOHO spread implies stronger biodiesel margins, which is bearish the D4 RIN all else equal.

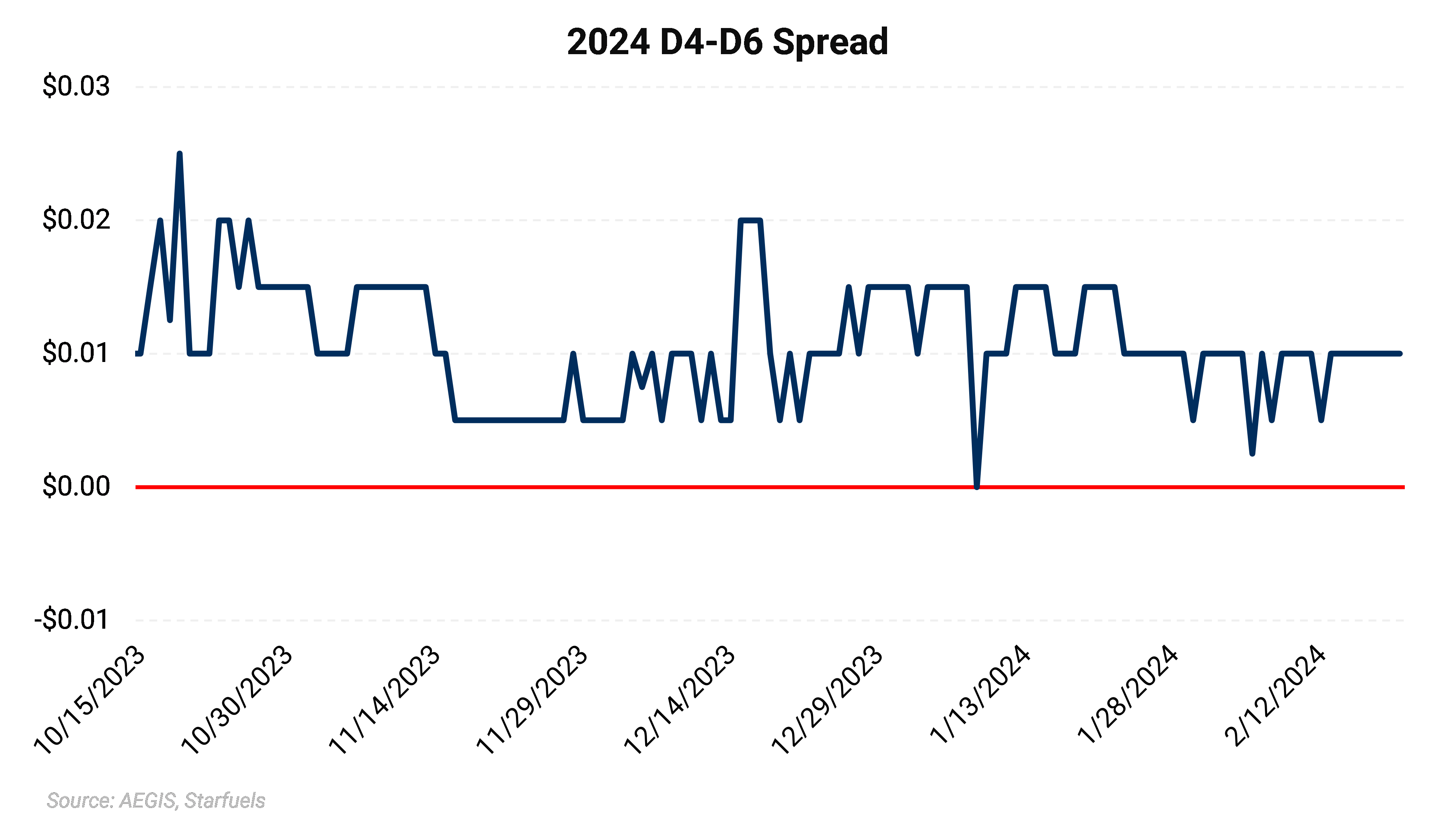

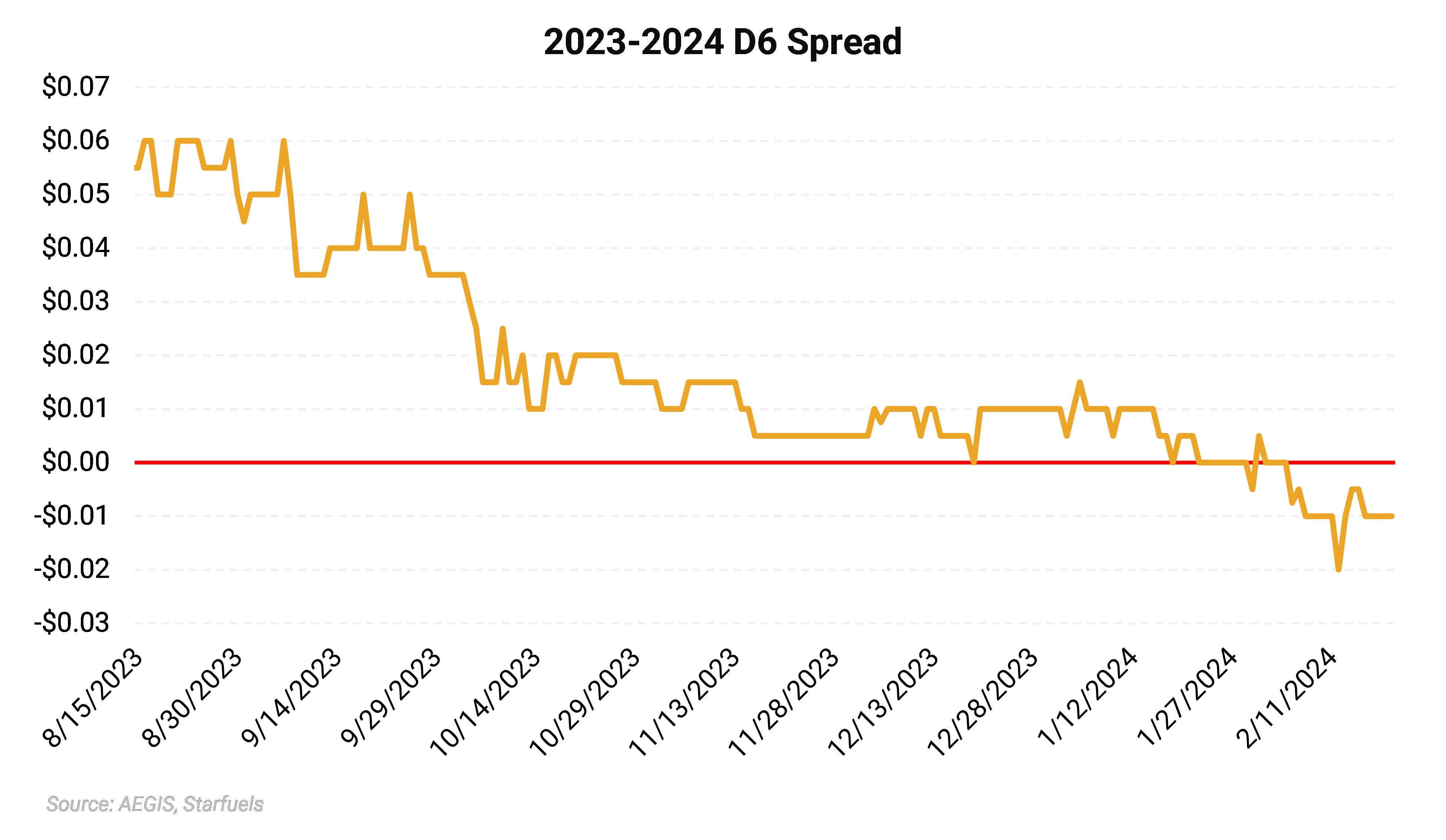

The D6 market posted similar losses over the same period with the D4/D6 spread narrowing to 0.75c from 1.5c at the start of the month as D6 RINs shed 12.5c, or 23%, over the first three weeks of February. We believe the premium for D4 RINs relative to D6 despite relative oversupply is reflective of the added value for the D4 RIN to fulfill multiple obligations relative to the D6 RIN which can only meet the renewable fuel requirement. The lack of a supplemental standard for 2024 and 2025 compliance is also bearish the D6 relative to the D4.

A narrower D4/D6 spread indicates tightness in D6 supply. In the absence of a sufficient supply of D6 credits, D4 and D5 credits from the advanced category can be used to satisfy compliance obligations.

Total 2023 D6 RIN generation came in at 14.825 billion credits, 425 million credits, or 2.8%, short of mandated volumes, through ample D4 RINs are available to cover the D6 compliance shortfall which will lead the 2023 D4/D6 RIN spread to trend toward parity.

The D3 market saw the halt of a two-month selloff as buying returned to the market in the face of a shortfall of 2023 vintage D3 credits relative to federally mandated obligations. D3 prices rose 23c, or 8%, over the first three weeks of February, breaching the $3.00 mark by February 21. Mounting expectations that the EPA may need to apply its waiver authority for the cellulosic obligation and/or issues a Cellulosic Waiver Credit (CWC) weighed on the marketplace. A petition by the American Fuel and Petrochemical Manufacturers (AFPM) for a partial 2023 waiver heightened bearish sentiment.

The C23/C24 spread widened to 5c/RIN on February 20 after starting the month at 2c/RIN.

We expect bullish 2023 D3 RIN generation to balance against bearish waiver expectations at least until February RIN generation data is available. Current tightness in the 2023 vintage D3 market should see 2023 D3 credits maintain premiums to 2024 vintage credits.

Total D3 and D7 RIN generation totaled 774.8 million credits when including January data, 65 million credits, or 7.7% short of the 840-million-gallon mandate. D3 generation had been running 16% short of the mandate prior to a material upward revision in December generation and strong January levels which largely represent 2023 production.

With no Cellulosic Waiver Credit in place and a record low RIN bank, we expect D3 RINs to remain at elevated levels barring an early implementation of eRINs and/or the issuance of a CWC under the EPA’s waiver authority.

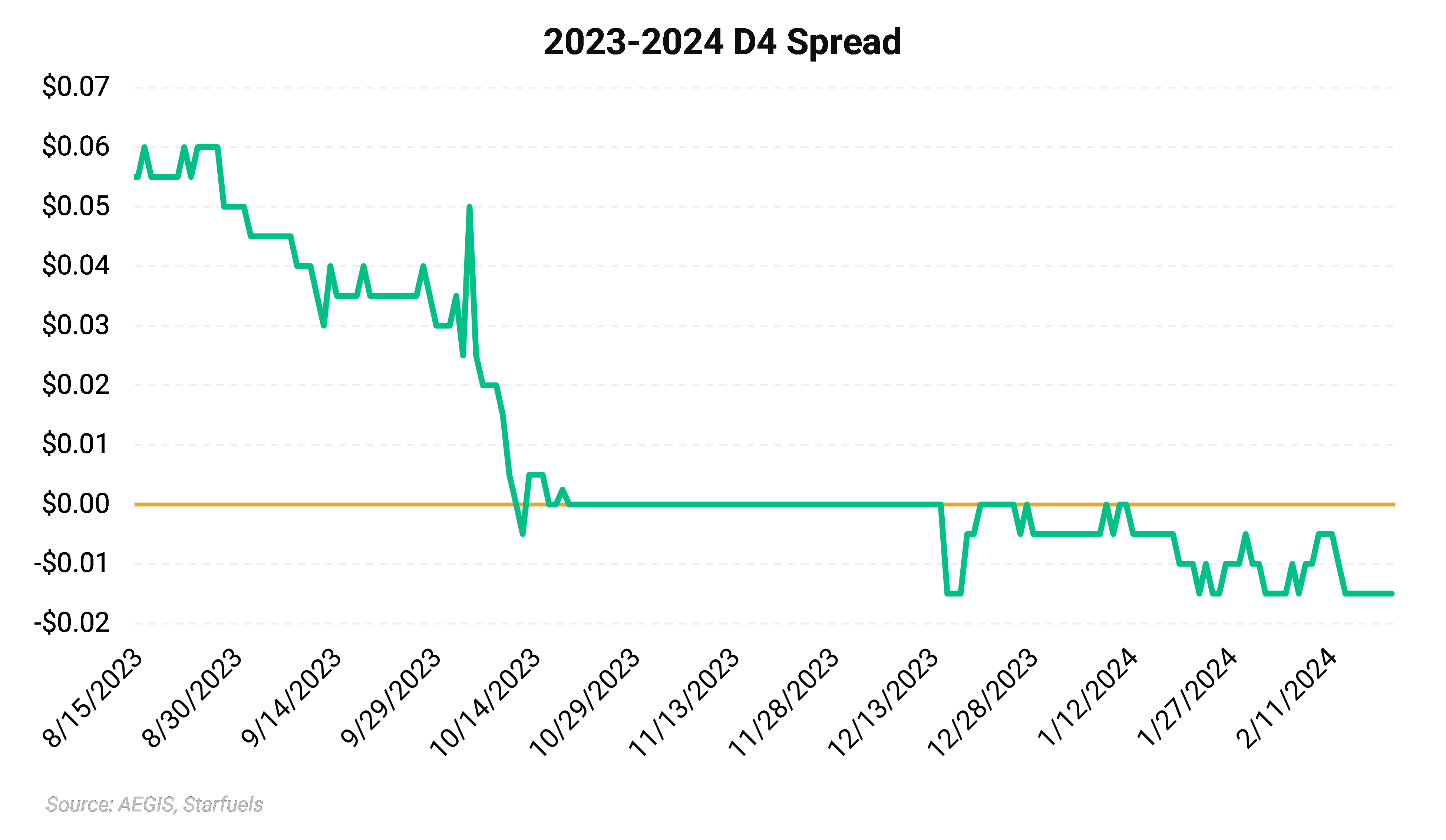

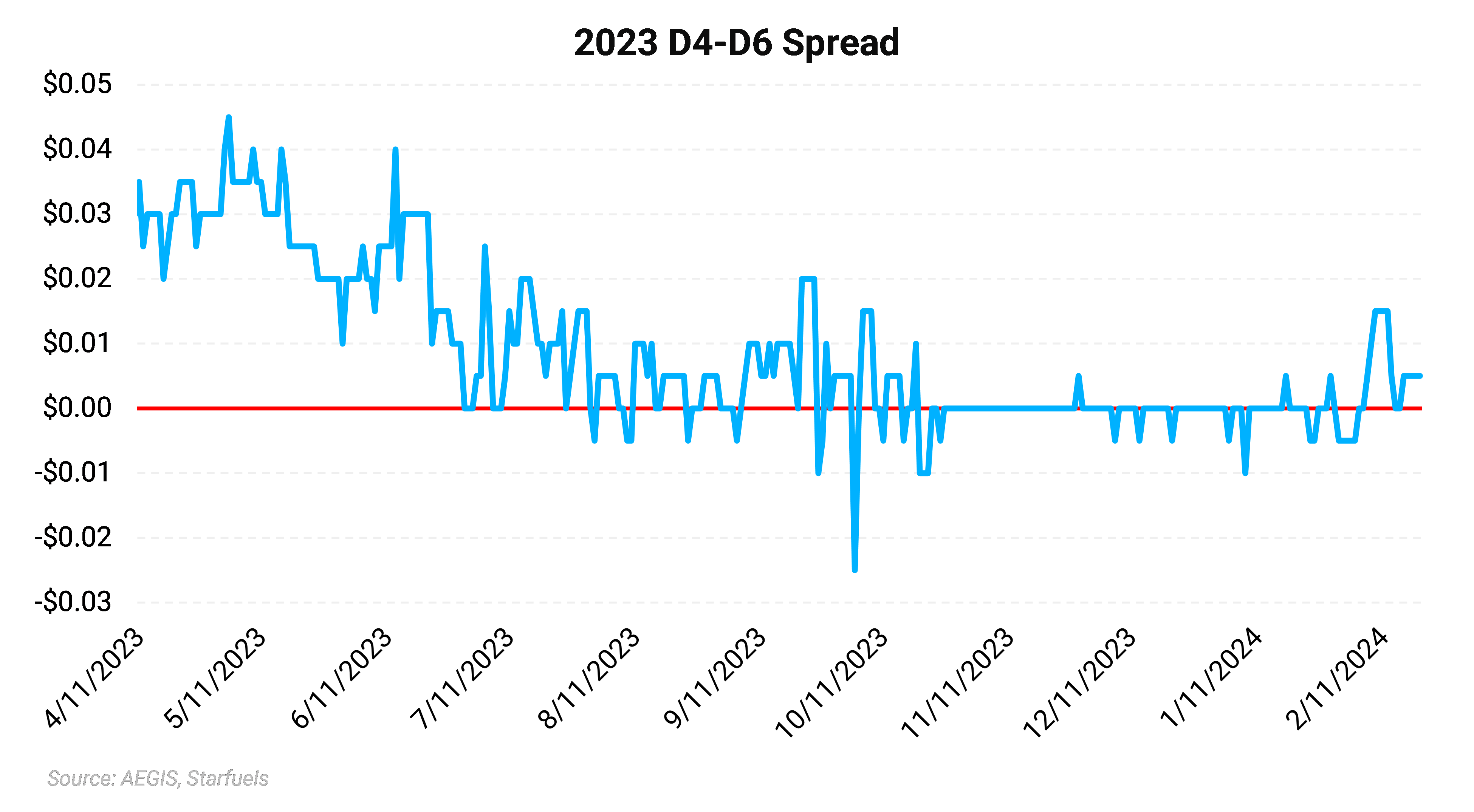

The 2023-2024 D4 RIN spread remained inverted as traders eyed a deteriorating margin environment. The spread spent the bulk of the month at -1.5c/RIN, firming up to -50pt during the second week of the month before widening out to -1.5c.

AEGIS noted in earlier reports that diesel would be the main driver of credit markets as RINs are the most responsive component of the credit stack for buttressing renewable diesel margins.

Persistent RIN losses despite recent diesel weakness show expectations of D4 oversupply and increasingly driving RIN markets to the severe detriment of RD margins. Current metrics suggest that D4 RINs could fall as low as the 25c/RIN mark before driving production cuts. We anticipate heavy production from both the RD and BD industry despite worsening margins as producers strive to take advantage of the final year of the BTC and more favorable economics for soybean oil-based production.

We expect RIN generation to remain at elevated levels should diesel strength persist and as long as feedstock pricing remain under pressure from imports. We maintain a bullish fundamental outlook for US diesel. D4 RIN prices have not fallen to sufficient levels to curb biodiesel or renewable diesel production, particularly given strength in the BOHO spread. Diesel strength and favorable weather conditions in South America underpin BOHO dynamics.

First half 2024 startups are planned to run at half capacity and should start to pressure RIN markets more materially in the second half of the year.

Given prevailing diesel prices, there is ample room for D4 credit prices to fall before producers trim runs, conduct maintenance, or shutdown. We see the 25c/RIN level as the current floor for D4 markets, though renewed diesel strength could undoubtedly see lower levels matriculate.

The 2023-2024 D6 spread inverted to -1c/RIN after starting the month at flat. The inter-vintage spread spent the bulk of the month of February at -5pt. The spread has averaged just under -1c since the start of the year after averaging flat during the fourth quarter of 2023.

EPA RIN Generation Data as of February 15:

EPA Small Refinery Exemption (SRE) Data as of February 15:

Green indicates change

Some of the price and regulatory risk in the development of the renewable fuels markets is controllable through hedging or pre-selling. Other risks require constant monitoring of pending changes to regulations and programs. AEGIS can help with both.

Interested in receiving these updates directly to your inbox?