Latest Insight

Last Look: Oil snaps its two-week losing streak, finishing $1.63 higher this week

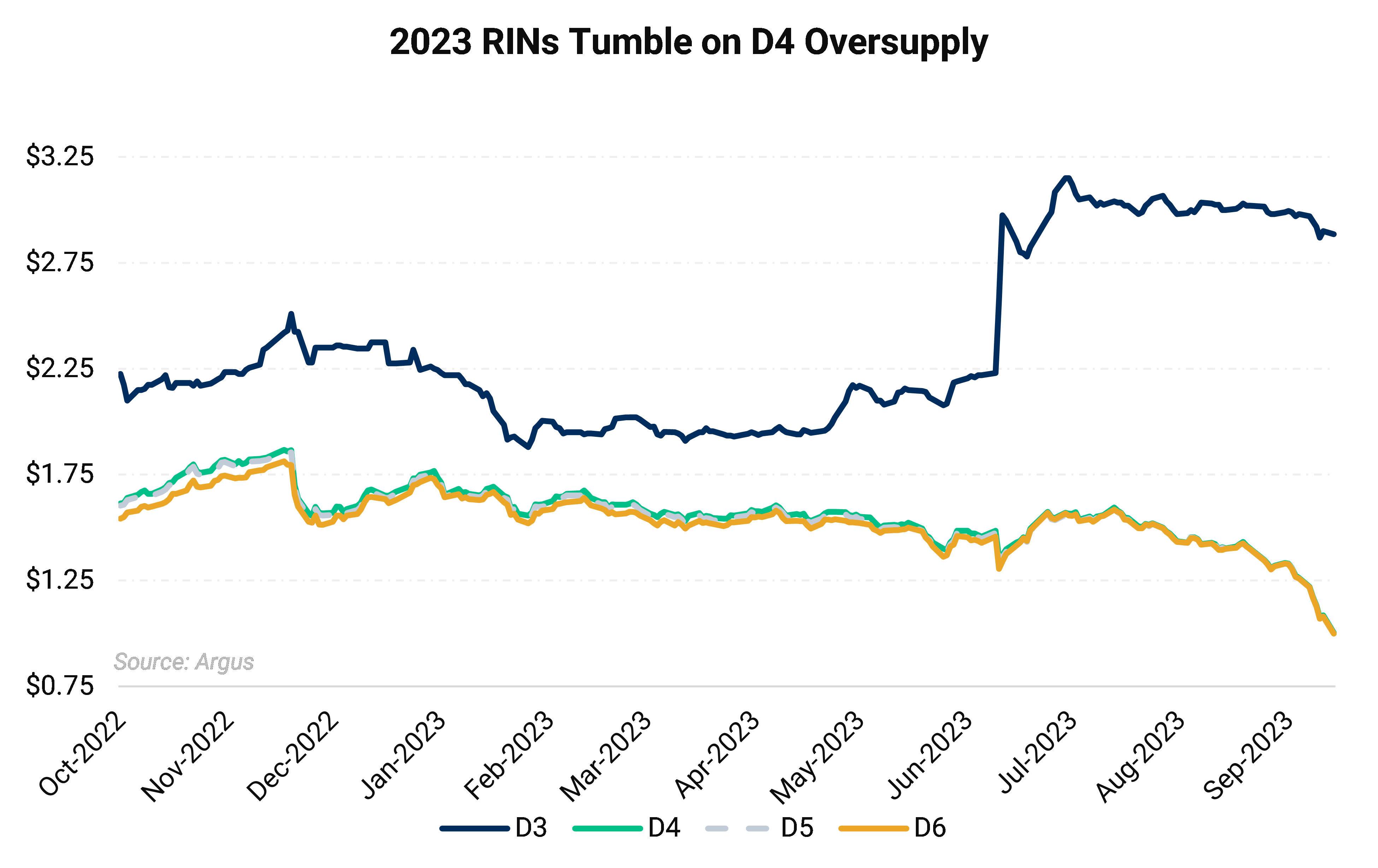

RIN prices fell to the lowest levels since December 2020 as an acute oversupply of D4 RINs and diesel strength pressured credits over the course of September.

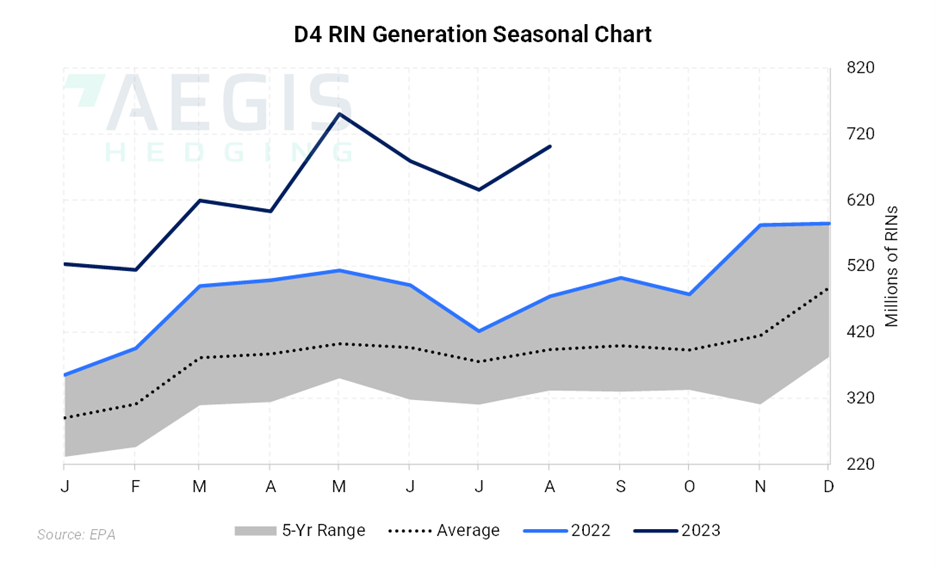

Selling was particularly heavy ahead of the September 21 release of the August RIN generation report which showed that total 2023 D4 generation is enough to satisfy more than 98% of the 2023 total advanced mandate.

Heavy losses in soybean oil alongside diesel strength saw the soybean oil-to-heating oil (BOHO) spread narrow to the lowest level in four months at $1.11/gallon on September 21. A narrower BOHO spread implies stronger biodiesel margins which are bearish the D4 RIN all else equal.

The D4 RIN rout saw renewable diesel margins tumble to the lowest levels in over two months. Despite the headline-grabbing RIN news, diesel strength in the first half of September underpinned historically healthy margins for both renewable diesel and biodiesel, carving out room for D4 RINs to post further losses.

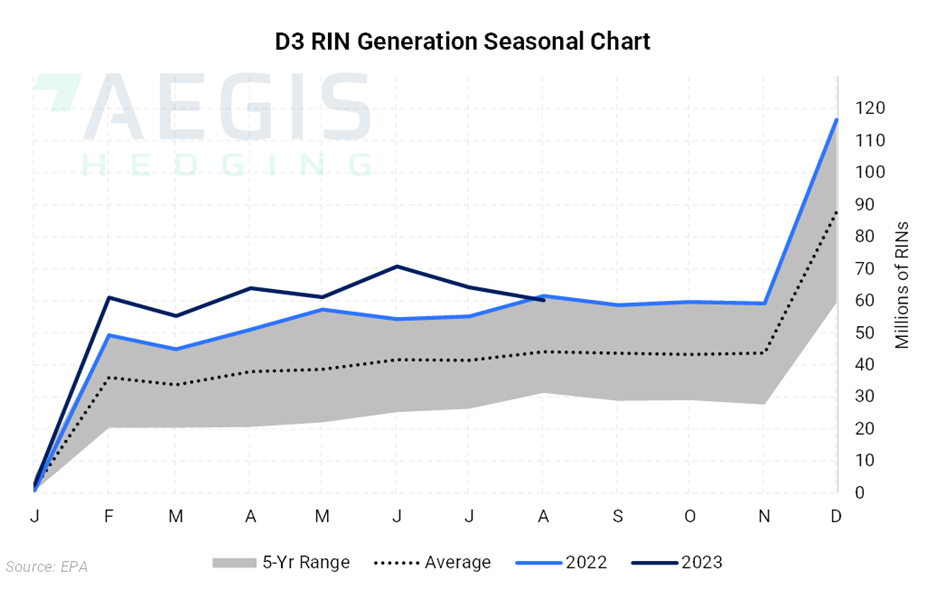

D3 losses were less pronounced as insufficient RIN generation, and the lack of a Cellulosic Waiver Credit (CWC) continued to buttress the market. Total D3 RIN generation is running 23% short of the cellulosic mandate. Average D3 output is up 17% on year-ago levels against a 25% year-over-year growth rate target set by the EPA.

Calendar:

Relevant News:

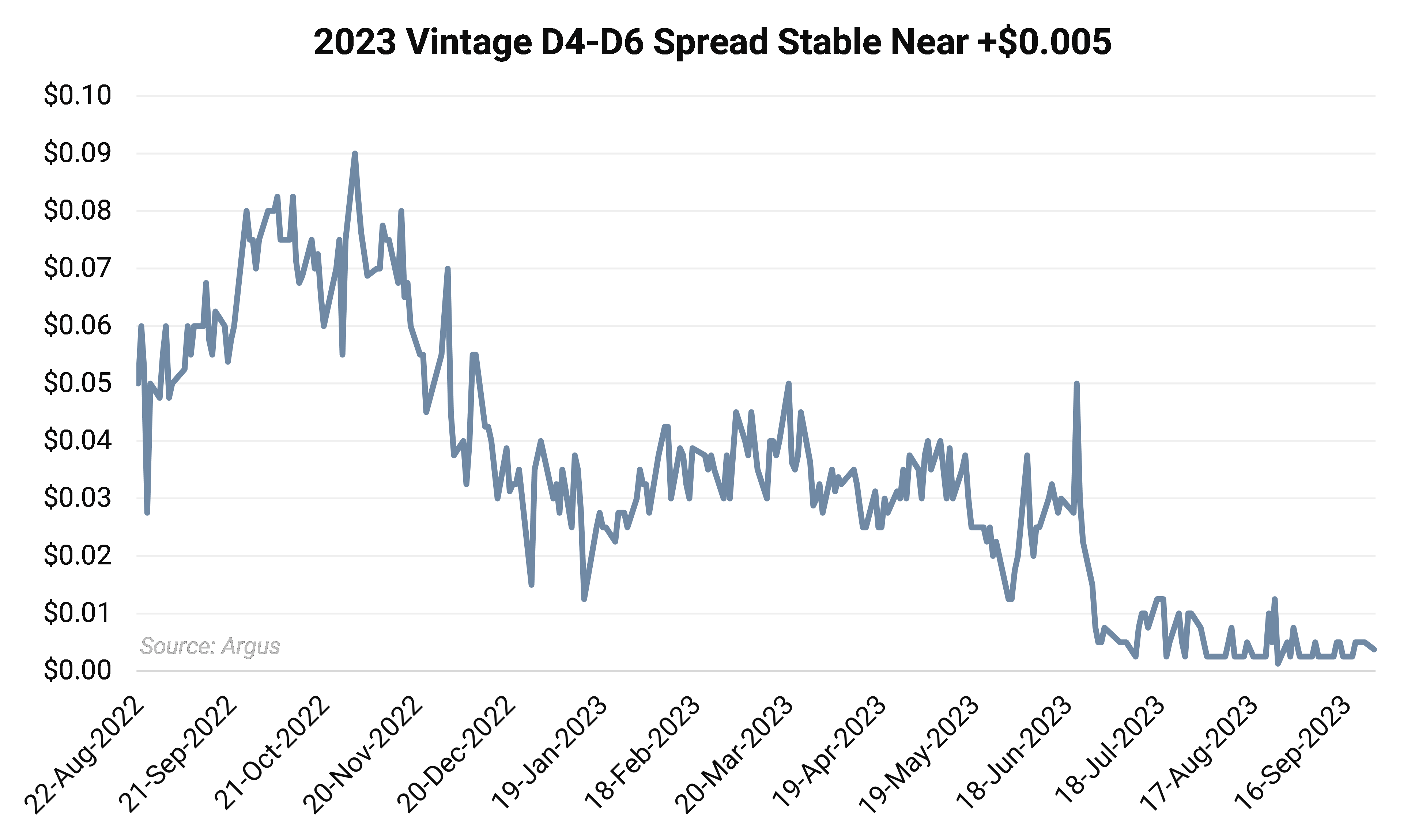

RIN markets tumbled to the lowest levels since December 2020 as a glut of D4 credits and a narrower BOHO spread spurred heavy selling late in the month. Diesel strength underpinned renewable diesel margins despite weaker D4 credits, carving out room for D4 credits to shed further value. Current year vintage D4 RINs shed 50c/RIN, or 33% since the start of August. The D6 market tracked the D4 rout with the D4/D6 spread spending the bulk of the month at 0.5c/RIN.

A narrower D4/D6 spread indicates tightness in D6 supply. In the absence of a sufficient supply of D6 credits, D4 and D5 credits from the advanced category can be used to satisfy compliance obligations.

We expect this spread to trend lower and even reach flat on occasion as the D4 RIN will play an increasing role in compliance with the total renewable fuel mandate.

Current D4 RIN generation is on pace to exceed the advanced mandate by 2.51 billion credits, while D6 generation is on pace to fall 511 million credits short of the mandate. Barring an upward adjustment to the advanced category, D4 RINs will make up an increasing proportion of the RIN bank moving forward.

The 2023 vintage D4 market reached as low as $1.004/RIN as oversupply weighed on markets. The BOHO bottomed out at $1.11/gallon on September 21 after starting the month at $1.89/gallon. The BOHO spread reached $2.66/gallon on July 25, the widest spread in 14 months.

The D6 market shed 50c/RIN, or 33%, while the D4/D6 spread narrowed to just 0.4c/RIN. D6 RIN generation remains on pace to fall more than half a billion credits short of mandated volumes, though ample D4 RINs are available to cover the D6 compliance shortfall which will keep the D4/D6 spread near parity.

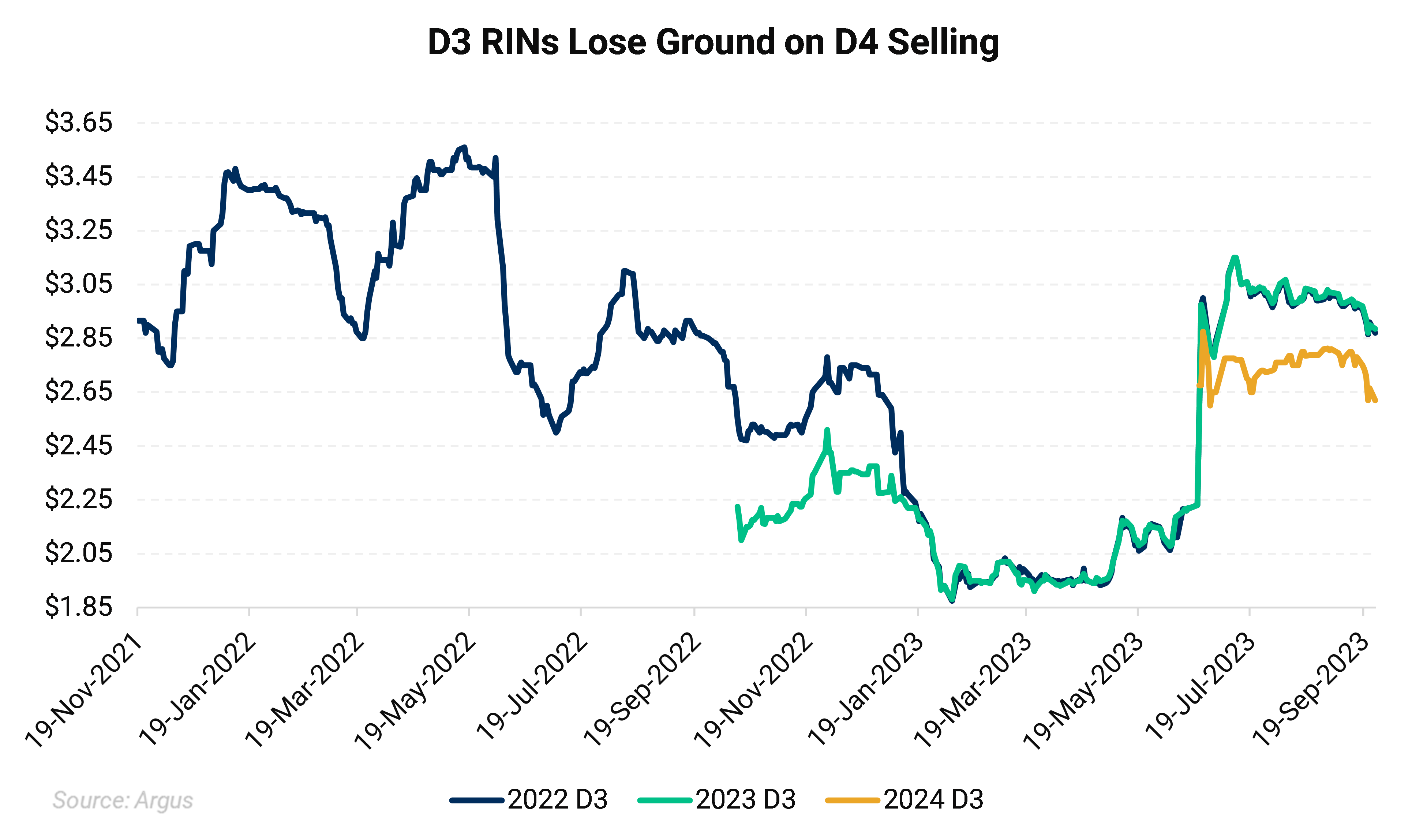

Losses were less pronounced in the D3 market as tight supply and the lack of a CWC continued to underpin markets. The 2023 vintage D3 RINs shed 10.5c/RIN since the start of August to as low as $2.885/RIN by September 25. The C23/C24 spread widened to 26.5c/RIN by late September after reaching as narrow as 19c/RIN in August.

D3 RIN generation held over the upper limit of the five-year average in August yet was running 23% short of the 840-million-gallon 2023 mandate. Current D3 generation is on pace to fall 181 million credits short of the final mandate. With no Cellulosic Waiver Credit in place and a record low RIN bank, we expect D3 RINs to remain at elevated levels barring an early implementation of eRINs and/or the issuance of a CWC under the EPA’s waiver authority.

The 2022 vintage market proved volatile over the course of September as an approaching compliance deadline saw spurts of heavier buying. Despite mounting demand the 2022 market saw more pronounced losses than the 2023 market, narrowing inter-vintage RIN spreads.

The 2023 D4-D6 spread spent the bulk of September at 0.5c/RIN and averaged 0.4c/RIN, unchanged from August. The D4 market entered freefall at midmonth as traders did not want to hold onto length heading into the September 21 release of the August RIN generation report. Diesel strength and soybean oil weakness made for healthy renewable diesel and biodiesel margins despite the heavy losses, allowing for ample room for further losses.

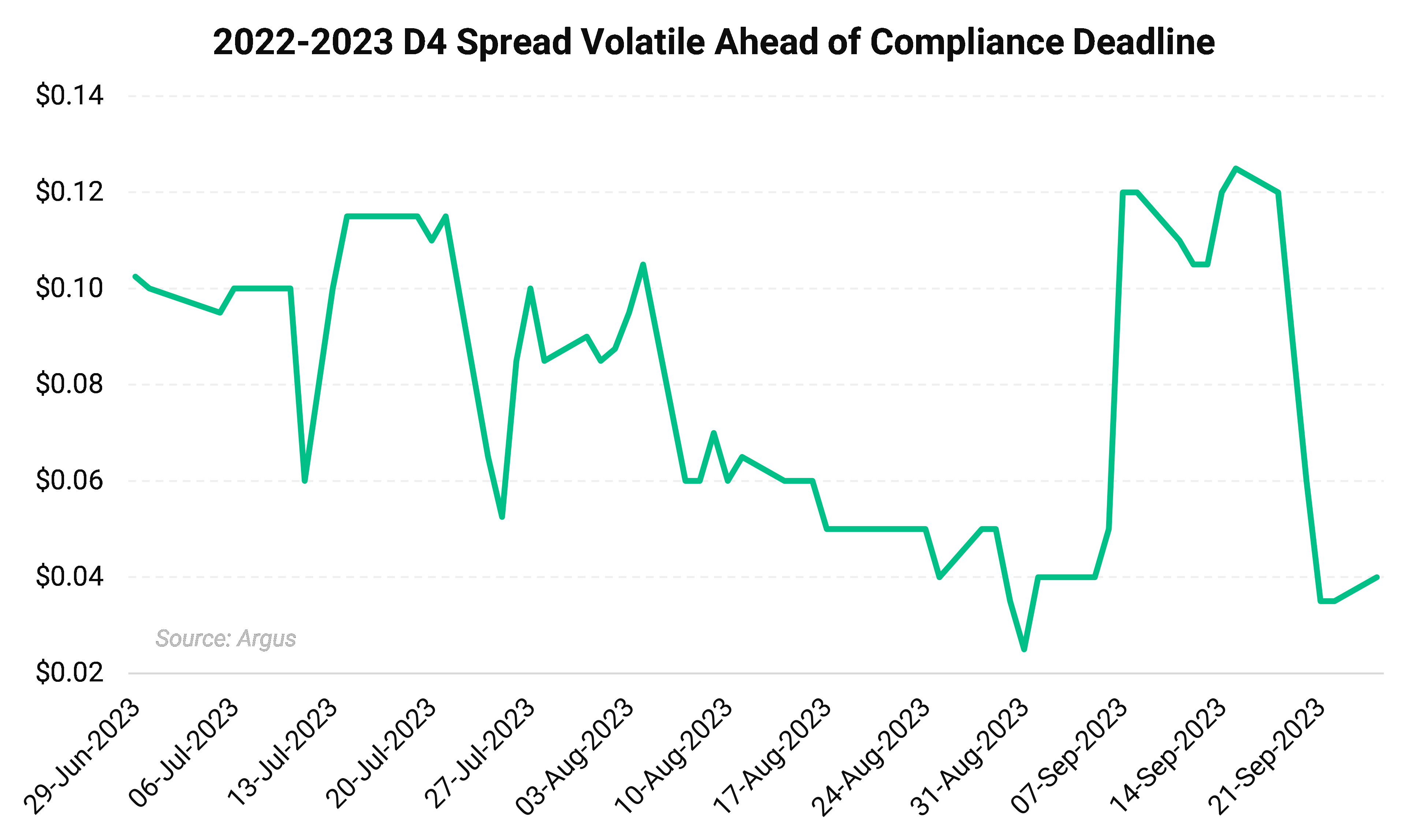

A wider D4-D6 spread implies a looser D6 supply as the D4 credit is the next vehicle of compliance in the absence of sufficient D6 RINs or the ability to use carryover credits. Conversely, a narrow D4-D6 spread implies a tight supply of D6 RINs. The theoretical cap on the spread is parity though D6s have traded at modest premiums to D4 credits in extreme circumstances.

The inter-vintage D4 RIN spread proved volatile over the course of September amid brief periods of demand for prior year credits ahead of December compliance. The spread blew out to 12.5c/RIN before tumbling to 3.5c/RIN at the peak of the RIN selloff.

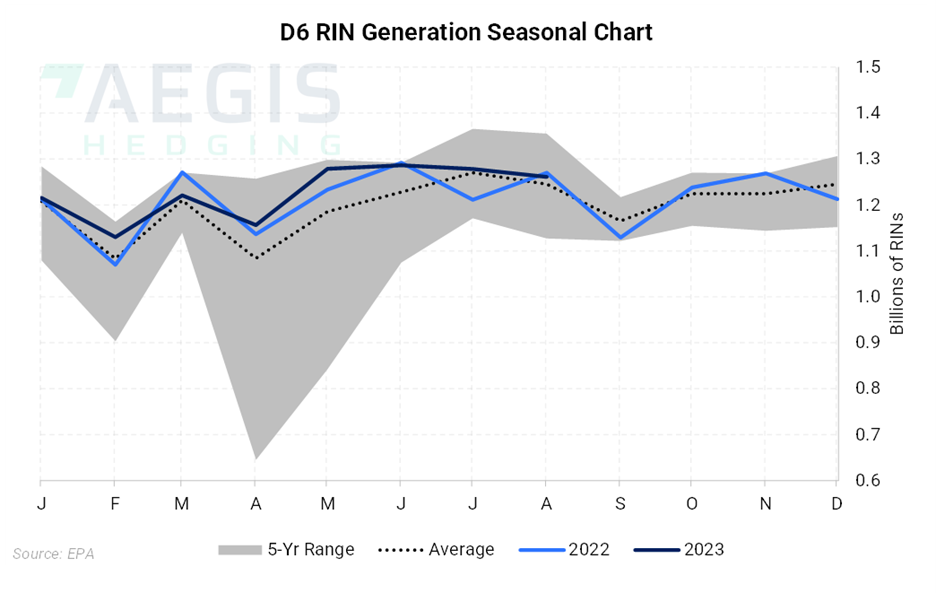

August D4 RIN generation of 701.3 million credits was up 65.8 million credits, or 13%, from July levels. We expect further diesel strength throughout the fourth quarter to support renewable diesel and biodiesel margins despite losses in credit markets, driving higher RIN generation, particularly among a slew of Q4 startups.

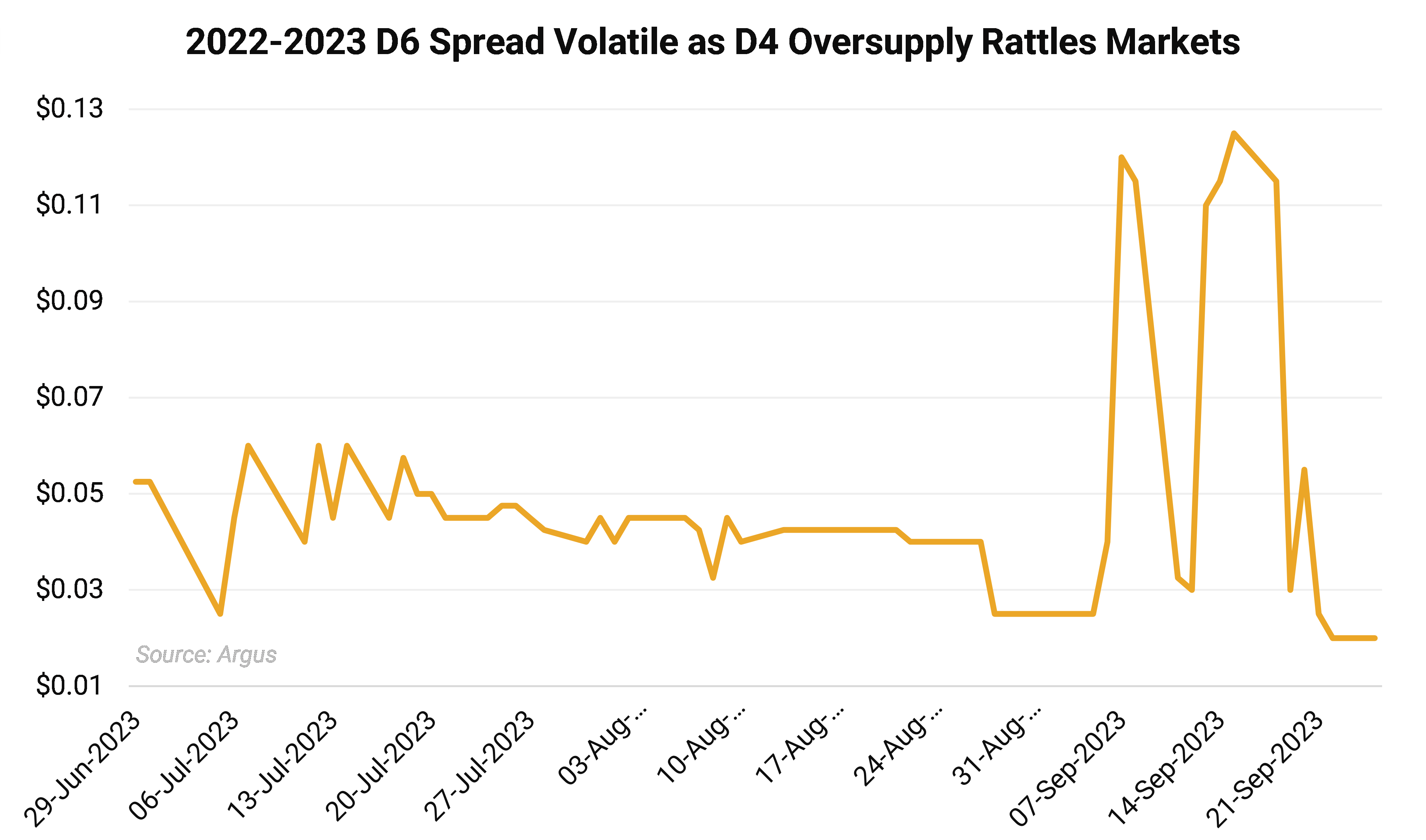

The 2022-2023 D6 spread followed a similar volatile pathway, widening to 12.5c/RIN before collapsing to 2c/RIN by September 22.

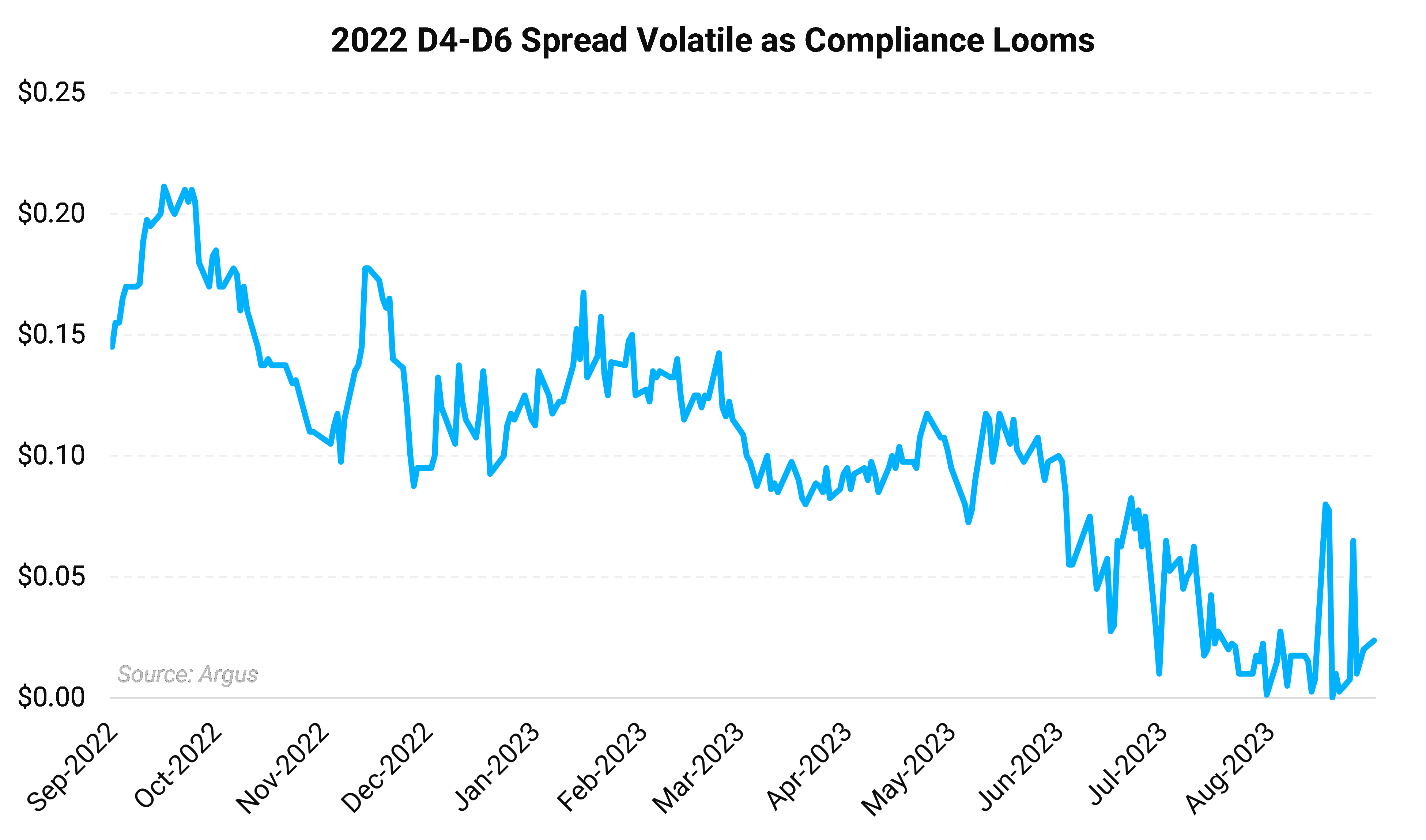

The 2022 D4-D6 spread seesawed narrowing to as little as 0.2c/RIN before widening out to 8c/RIN briefly. The spread reached 2.4c/RIN by September 25. The spread averaged 2.4c/RIN in August, 5.5c/RIN in July, 9.6c/RIN during the month of June, and 9.8c/RIN during the month of May.

Green indicates change