To quickly access the page content, please click on the links below:

News Update

- California postpones hearing on proposed LCFS amendments originally scheduled for March 21. CARB aims to hold a workshop in April. The 45-day public comment period concluded on February 20. The move comes after the state’s Environmental Justice Advisory Committee (EJAC) urged the Board to delay its LCFS vote until July 2024 as the current plan relies too heavily on biofuels, out-of-state biogas, and biogas from dairy digesters. California LCFS credit markets tracked higher on expectations CARB is pursuing very stringent CI targets and considering possible limitations to renewable fuels and biogas.

- GREET guidance delayed by weeks. GREET guidance has been delayed by a few weeks as the new greenhouse gas model awaits approval from the Treasury Department, USDA head Tom Vilsack said on March 1, according to Argus Media. The Biden administration was supposed to announce new guidance by March 1, with industry hopes pinned on a viable pathway for corn-based ethanol-to-SAF. Vilsack confirmed the model would be used to determine emissions for ethanol-to-SAF, according to Argus Media. The adjustment to the Department of Energy’s GREET model aims to ensure crediting for farming practices which reduce environmental impact like cover crops and no-till farming.

- Washington Clean Fuel Standard Posts Second Consecutive Net Credit Surplus for Q2 2023. A total of 350,219 WCFS credits were generated during the second quarter of 2023, with corn-based ethanol accounting for 57% of the total, down from 64% the prior quarter. Renewable diesel made up 22% of total credit generation, up from 12% the previous quarter. Biodiesel accounted for less than 5% of total credits, down sharply from more than 11% in the first quarter of 2023. Deficits fell by 3.6% from the first quarter to total 227,930, with declines in gasoline and diesel deficits offsetting gains in deficits from ethanol and diesel. Total Q1 credits were revised down to 270,965 credits from the 275,442 credits originally reported in the state’s inaugural quarterly report. Total Q1 deficits were revised upward to 236,489 from the originally reported 227,768. The average CI value for renewable diesel tumbled 15.43pt, or nearly 24% to 49.17. The average CI for ethanol slumped 3.06pt, or 4%, to 74.38. Biodiesel average CI was little changed at 52.29 for Q2 2023.

- EIA Trims 2024 Renewable Diesel Production and Consumption Forecast. The EIA trimmed is 2024 renewable diesel production and consumption forecasts in its latest Short-Term Energy Outlook. The agency forecast renewable diesel production of 218,000 Bbl/d in 2024, down 3.5% from the previous month’s estimate of 226,000 Bbl/d. The outlook for 2025 production was unchanged at 290,000 Bbl/d. The EIA trimmed 2024 demand to 242,000 Bbl/d from its February estimate of 249,000 Bbl/d, marking a month-over-month decline of 2.8%. The demand forecast for 2025 was lifted by 2,000 Bbl/d to 306,000 Bbl/d. Renewable diesel imports in 2024 were stable at 24,700 Bbl/d, while the 2025 outlook dropped to 16,000 Bbl/d.

- EJAC Advises Delay to LCFS Scoping Vote. The CARB’s Environmental Justice Advisory Committee (EJAC) urged the Board to delay its LCFS vote until July 2024 as the current plan relies too heavily on biofuels and out-of-state biogas. Spot LCFS prices did largely stabilized in the wake of the EJAC meeting as the comments do not represent formal recommendations. Market participants are increasingly anticipating significant delays in the implementation of much-needed amendments to the LCFS which has proved bearish for prompt credit prices.

- Former CARB Chief Cheryl Laskowski Comments on Auto-Acceleration Mechanism. Cheryl Laskowski, former CARB Chief of Transportation Fuels, issued comments on the auto-acceleration mechanism (AAM) and RNG phaseouts contained in the states’ proposed scoping plan. Laskowski noted that the AAM would address oversupply of credits in the LCFS programs by triggering two checks. The AAM would be triggered if the credit to deficit ratio is greater than one, or if the total credit bank exceeds three quarters of annual deficit. The AAM can not be implemented before 2027, according to comments by Laskowski, and could not be triggered two years in a row. Laskowski commented on the state’s proposal to phase out crediting pathways for RNG for vehicle use by 2040 saying the language was not clear enough. Laskowski said the proposal could be interpreted to allow a project certified in December 2029 to earn avoided methane credits through 2060. The proposal is under a 45-day public comment period ending February 20.

- CARB Releases Proposed LCFS Amendments Ahead of March 21 Public Hearing. On December 19, California’s Air Resources Board (CARB) released a preliminary LCFS proposal laying out amendments which nearly mirrored those in the Standardized Regulatory Impact Assessment released in September. CARB proposed a 30% reduction in carbon intensity by 2030, including a 5% step-down in 2025. This marks a 50% increase in carbon targets over the original 20% reduction target for 2030. Reductions increase to 90% by 2045 compared to a 2010 baseline. The proposal contained an automatic acceleration mechanism (AAM) which would advance stringency for a given year when unused credits more than triple average deficit generation by advancing the carbon reduction target by two years. Amendments included eliminating the exemption for intrastate jet fuel beginning in 2028 and new tracking requirements for crop-based and forestry-based feedstocks to their point of origin. The regulator proposed phasing out biogas used in transportation fuel by 2041 and by 2045 for biomethane used to produce renewable hydrogen. CARB expects to kick off the required 45-day public comment period in January, with a public hearing set for March 21, 2024.

- Washington Aims for SAF Eligibility in Rulemaking Update. The Washington Department of Ecology will begin rulemaking early 2024 to advance SAF pathways for credit generation as early as December 31, 2023. Earlier this year, Washington legislators passed a law requiring the department to accept SAF applications by the end of 2023 and accepting biomethane as a feedstock for renewable diesel and SAF. The move builds on the state’s SAF credit eligible for SAF sold on flights departing the state. The $1/gallon base credit value can reach a maximum of $2/gallon based on each percentage point in carbon reduction under 50%. Next year’s round of rulemaking will seek to establish a third-party verification program, incentives to encourage SAF production, update book-and-claim accounting requirements for electricity and methane. Washington is not adjusting current annual targets, land-use change requirements and models that set fuel carbon intensity scores.

- British Columbia Low Carbon Fuel Standard to Require SAF. The government of British Columbia on December 11 released new rules for its Low Carbon Fuels Standard, set to take effect on January 1, 2024. Under the updated regulations, SAF must make up 1% of the fuel mix by 2028, rising to 2% for 2029 and 3% for 2030 and beyond. The regulations include carbon intensity reductions for jet fuel starting at 2% in 2026, 4% in 2029, 6% in 2028, 8% in 2029 and 10% for 2030 and beyond. CI reduction requirements for gasoline and diesel start at 16% in 2024, rising to 18.3% in 2025, 20.6% in 2026, 23% in 2027, 25.3% in 2028, 27.7% in 2029 and 30% in 2030.

- Marathon Martinez Refinery Fires Trigger Federal Investigation. Recent fires at Marathon’s Martinez refinery triggered a federal investigation by the Chemical Safety and Hazard Investigation Board (CSB). Fires on November 11 and November 19 at a hydrodeoxygenation (HDO) unit led to spills of RD. Marathon aims to achieve 48,000 Bbl/d of production at its Martinez, California facility by year-end.

Market Update

- CARB reported an average California LCFS transfer price of $62.00/t in February 2024, down $7/t, or 10% from January 2024. This marks the lowest transfer price since October 2015. February saw a transfer price range of $56/t to $87/t per credit with 219 entities only selling against 29 entities only buying. February ICE futures averaged $60.38/t over the course of the month of February.

- A little over 1.9MM t of credits moved across 201 transfers, down sharply from January’s monthly record of 526 transfers. February transfers were up 25% on year-ago levels, with volumes increasing 48% over the same period. Total 2023 transfers came in at just under 40.2MM t of credits, up 31% from 2022 totals.

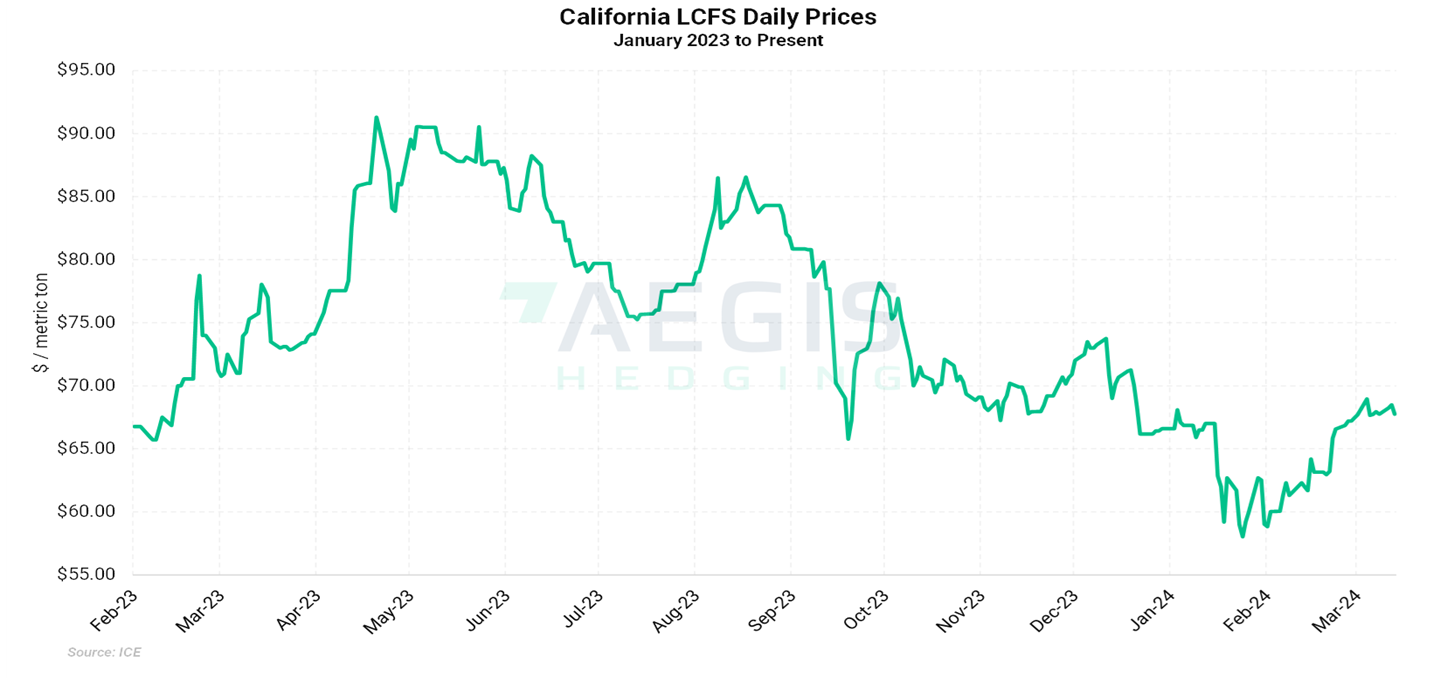

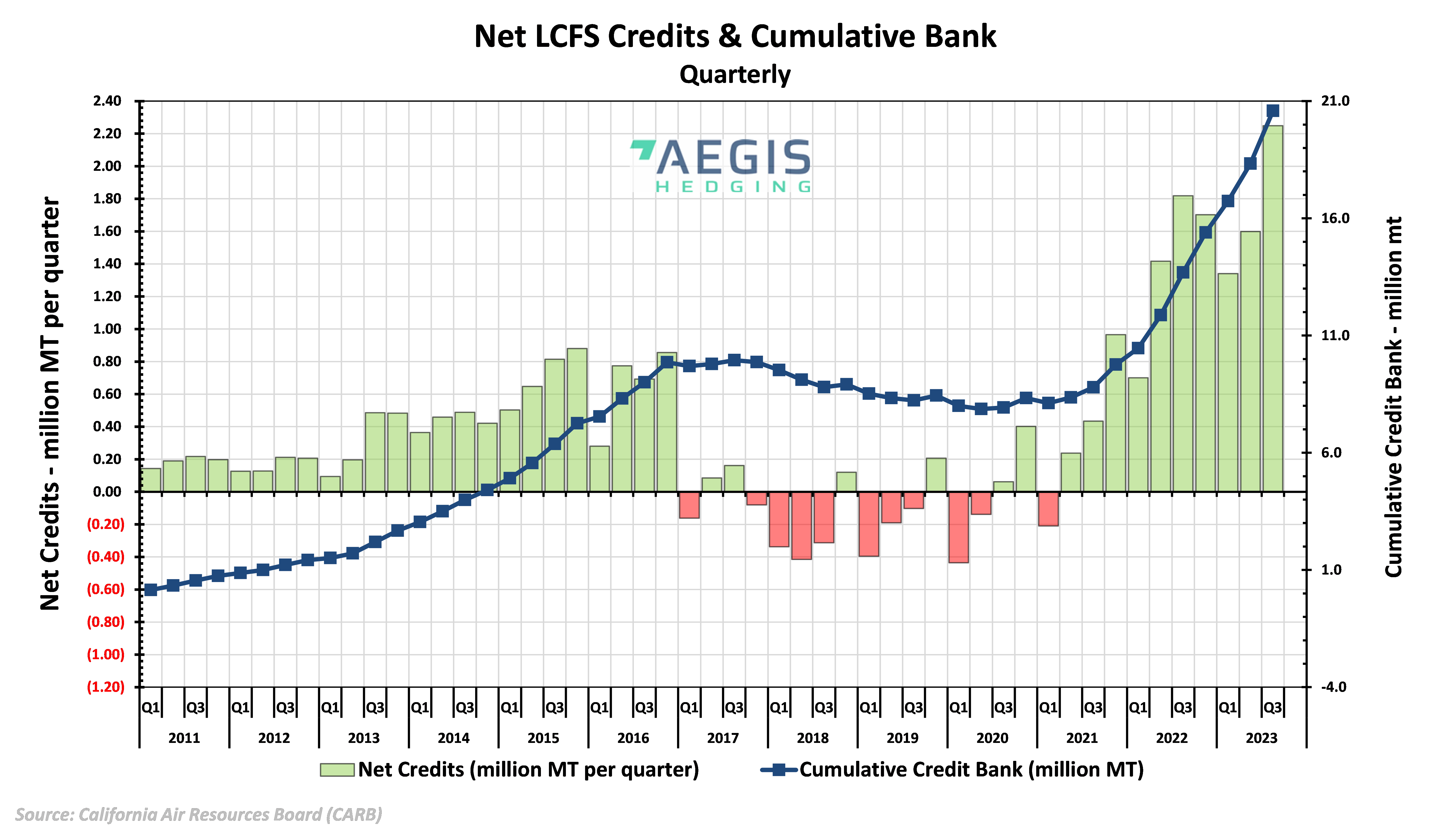

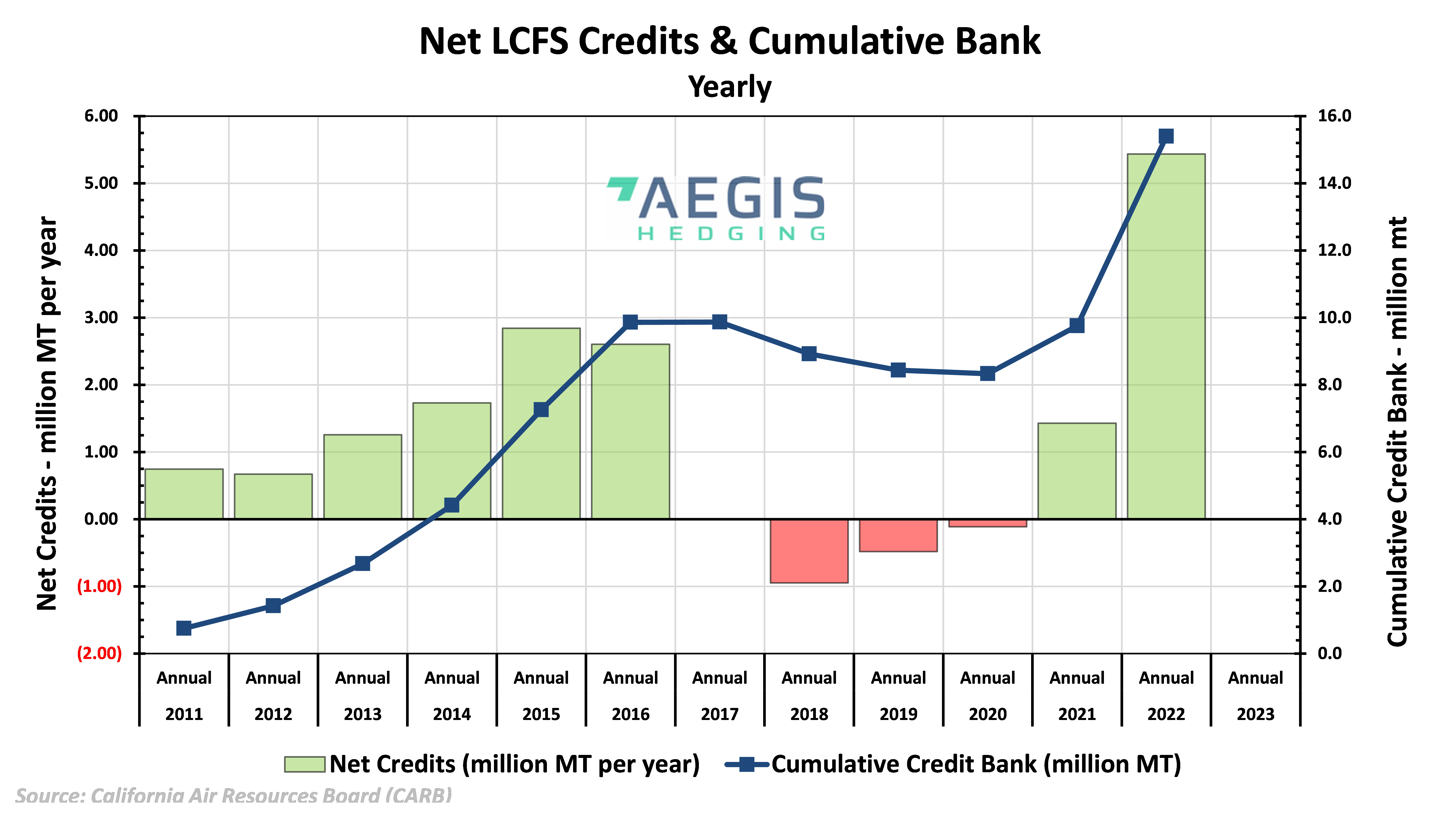

- California LCFS credits traded down to $58.71/t as Q3 data continued to weigh on markets. The market firmed to $62.28/t on news that California was postponing its hearing on reforms to consider more stringent targets and possible restrictions on renewable fuels and biogas. The market reached as high as $68.95/t by March 4. Q3 data showed a fresh record surplus of 20.6MM t of unused credits, with the bank growing by 2.2MM t, or 12%, from the previous quarter. The cumulative credit bank has grown by 6.9MM t, or 50%, over the course of the last four quarters.

- Oregon DEQ reported 237,917 metric tons across 25 transfers in February 2024. Transfers fell by 15, or 38%, while volumes increased by 35% from the month prior. February saw an averaged transfer price of $132.03/credit, up 11% from January’s price of $118.99/credit. Oregon DEQ quarterly data showed 321,791 credits generated from renewable diesel during Q3, up 33% from the previous quarter and accounting for 47% of all credits generated. Biodiesel generated 128,222 credits, up 21% from the previous quarter and accounting for 19% of all credits generated.

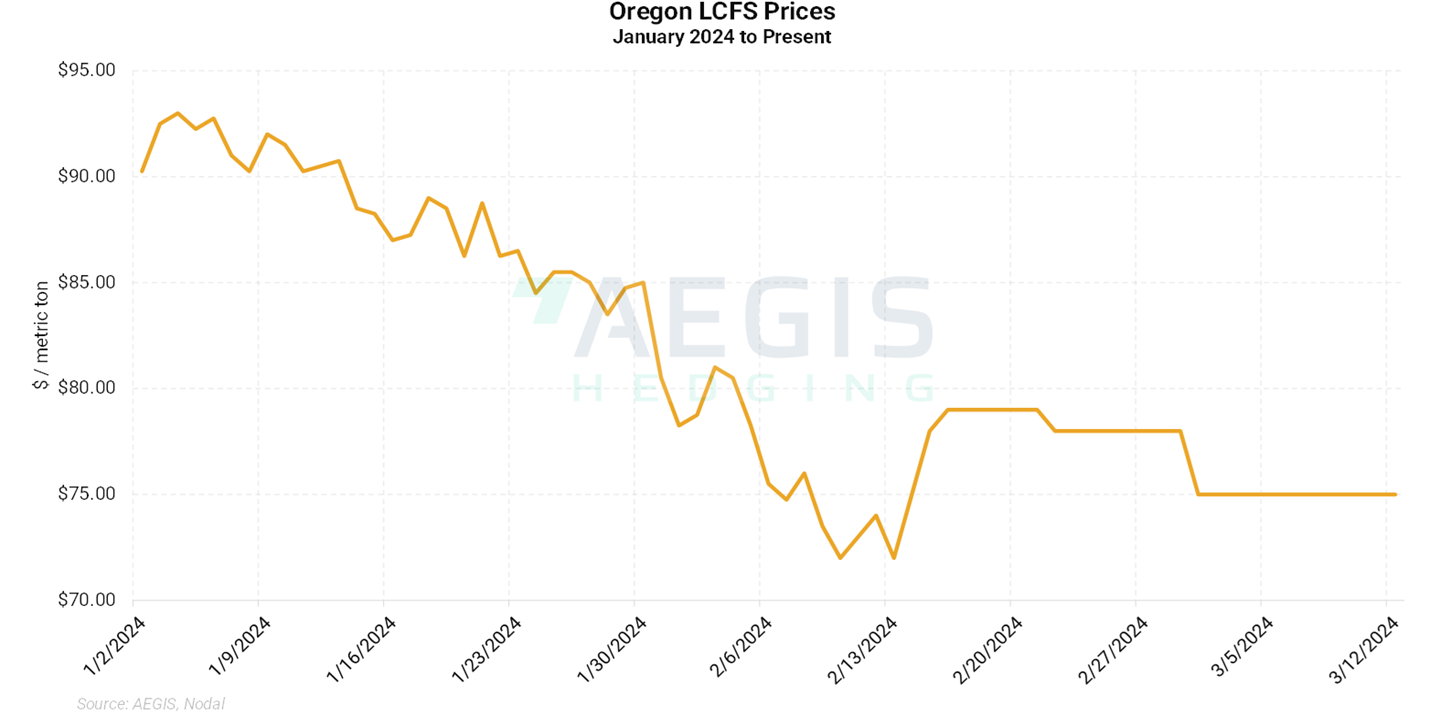

- Oregon LCFS credit prices proved choppy over the course of February, ranging from $72.00/t to $82.00/t amid a lack of direction. Prompt prices slumped to $75.00 by early March, shedding $3.25/t, or 4% since February and $15.25/t, or 17% since the start of the year. The state’s spot credit price maintains a hefty premium to California and Washington even as Oregon attracts increasing amounts of renewable diesel.

- The California LCFS market remains acutely oversupplied with the bank of available credits setting a fresh record high for the third quarter of 2023 and credits outpacing deficits by an increasing gap since July 2020. Oversupply saw prompt prices bottom at $59.00/t in 2023 and dip under $58.00/t in early 2024. The outlook for CARB to adopt more stringent CI targets alongside possible limitations to certain fuels and pathways should prove supportive in the near term. The market could find long-term support should CARB adopt an appropriately bullish stance and a timely rulemaking process.

LCFS & CFP Schedule

| Washington WCFS SAF Hearings |

February 22nd & 28th, 2024 |

|

|

|

|

|

|

|

| California LCFS Q4 Reporting Deadline |

April 21st, 2024 |

|

|

|

|

|

|

|

| CARB Public Workship |

Mid-April, 2024 |

|

|

|

|

|

|

|

|

|

|

|

|

LCFS Credit & Futures Pricing

| Credit Prices as of March 12th, 2024: |

California Futures Prices as of March 12th, 2024: |

- California - Futures: $ 68.49

|

|

- Oregon - Futures: $ 75.00

|

|

- Washington - Futures: $ 38.00

|

|

LCFS Cost for Gasoline and Diesel

|

California, as of March 12th, 2024:

|

Oregon, as of March12th, 2024:

|

- CARBOB (No Cl ethanol) - Vintage 2024: 10.18 cents per gallon

|

- E10 gasoline - Vintage 2024: 6.97 cents per gallon

|

- CARB ULSD - Vintage 2024: 11.57 cents per gallon

|

- B5 diesel – Vintage 2024: 7.94 cents per gallon

|

Monthly Credit Transfer Activity for California

|

Time

|

Transfers

|

Total Volume

|

Avg $/credit

|

|

24-Feb

|

201

|

1,911,000

|

$62

|

|

24-Jan

|

526

|

6,196,000

|

$69

|

|

23-Dec

|

422

|

6,161,000

|

$73

|

|

23-Nov

|

203

|

2,672,000

|

$70

|

|

23-Oct

|

451

|

4,661,000

|

$76

|

|

23-Sep

|

233

|

1,033,000

|

$73

|

|

23-Aug

|

168

|

2,044,000

|

$77

|

|

23-Jul

|

417

|

4,347,000

|

$75

|

| 23-Jun |

222 |

2,470,000 |

$79 |

| 23-May |

158 |

1,684,000 |

$81 |

| 23-Apr |

547 |

5,596,000 |

$74 |

|

23-Mar

|

252

|

2,702,000

|

$73

|

|

23-Feb

|

161

|

1,293,000

|

$71

|

|

CY 2023

|

3,704

|

40,186,000

|

$75

|

|

CY 2022

|

3,137

|

30,641,000

|

$125

|

|

CY 2021

|

2,664

|

25,279,000

|

$187

|

|

CY 2020

|

2,461

|

21,728,000

|

$199

|

|

CY 2019

|

1,656

|

14,146,000

|

$192

|

|

CY 2018

|

1725

|

13,334,000

|

$160

|

|

CY 2017

|

1226

|

8,875,000

|

$89

|

|

CY 2016

|

929

|

5,343,000

|

$101

|

|

CY 2015

|

578

|

2,852,000

|

$62

|

|

CY 2014

|

304

|

1,667,000

|

$31

|

|

CY 2013

|

202

|

887,000

|

$55

|

Source: https://ww2.arb.ca.gov/resources/documents/monthly-lcfs-credit-transfer-activity-reports

Monthly Credit Transfer Activity for Oregon

|

Time

|

Transfers

|

Total Volume

|

Avg $/credit

|

| 24-Feb |

25 |

237,917 |

$132.03 |

| 24-Jan |

40 |

175,832 |

$118.99 |

| 23-Dec |

45 |

353,436 |

$137.96 |

| 23-Nov |

35 |

164,936 |

$129.97 |

| 23-Oct |

34 |

188,537 |

$143.93 |

| 23- Sep |

23 |

102,570 |

$141.94 |

| 23- Aug |

29 |

188,709 |

$137.33 |

| 23- Jul |

32 |

166,522 |

$137.93 |

| 23-Jun |

28 |

123,401 |

$130.21 |

| 23-May |

30 |

121,556 |

$131.04 |

|

23-Apr

|

69

|

322,461

|

$121.73

|

|

23-Mar

|

50

|

345,944

|

$118.85

|

|

23-Feb

|

24

|

130,929

|

$119.73

|

|

CY 2023

|

442

|

2,421,140

|

$129.76

|

|

CY 2022

|

319

|

1,607,127

|

$119.01

|

|

CY 2021

|

245

|

1,035,306

|

$125.30

|

|

CY 2020

|

151

|

806,028

|

$128.08

|

Source: https://www.oregon.gov/deq/ghgp/cfp/Pages/Monthly-Data.aspx

Monthly Credit Transfer Activity for Washington

|

Time

|

Transfers

|

Total Volume

|

Avg $/credit

|

| 24-Feb |

16 |

62,672 |

$89.89 |

| 24-Jan |

12 |

80,921 |

$79.85 |

| 23-Dec |

8 |

58,288 |

$74.06 |

| 23-Nov |

- |

- |

- |

| 23-Oct |

10 |

49,930 |

$98.12 |

| 23- Sep |

20 |

51,322 |

$96.26 |

| 23- Aug |

4 |

27,055 |

$106.66 |

| 23-Jul |

0 |

0 |

- |

|

CY 2023

|

42

|

186,595

|

$91.23

|

|

CY 2022

|

-

|

-

|

-

|

|

CY 2021

|

-

|

-

|

-

|

Source: https://ecology.wa.gov/air-climate/reducing-greenhouse-gas-emissions/clean-fuel-standard/data-reports

Figure 1. California LCFS Prompt USD/mt January 2023 - Present

|

|

|

|

|

2023 Average Daily Price: $ 75.79

|

2024 Average Daily Price: $ 62.85

|

|

2023 Highest Daily Price: $ 87.00

|

2024 Highest Daily Price: $ 68.95

|

|

(May 9th, 2023)

|

(March 4th, 2024)

|

|

|

Figure 2. Oregon LCFS Prompt USD/mt January 2024 - Present

|

|

|

2024 Average Daily Price: $82.20

|

|

2024 Highest Daily Price: $93.00

|

|

(January 4th, 2024)

|

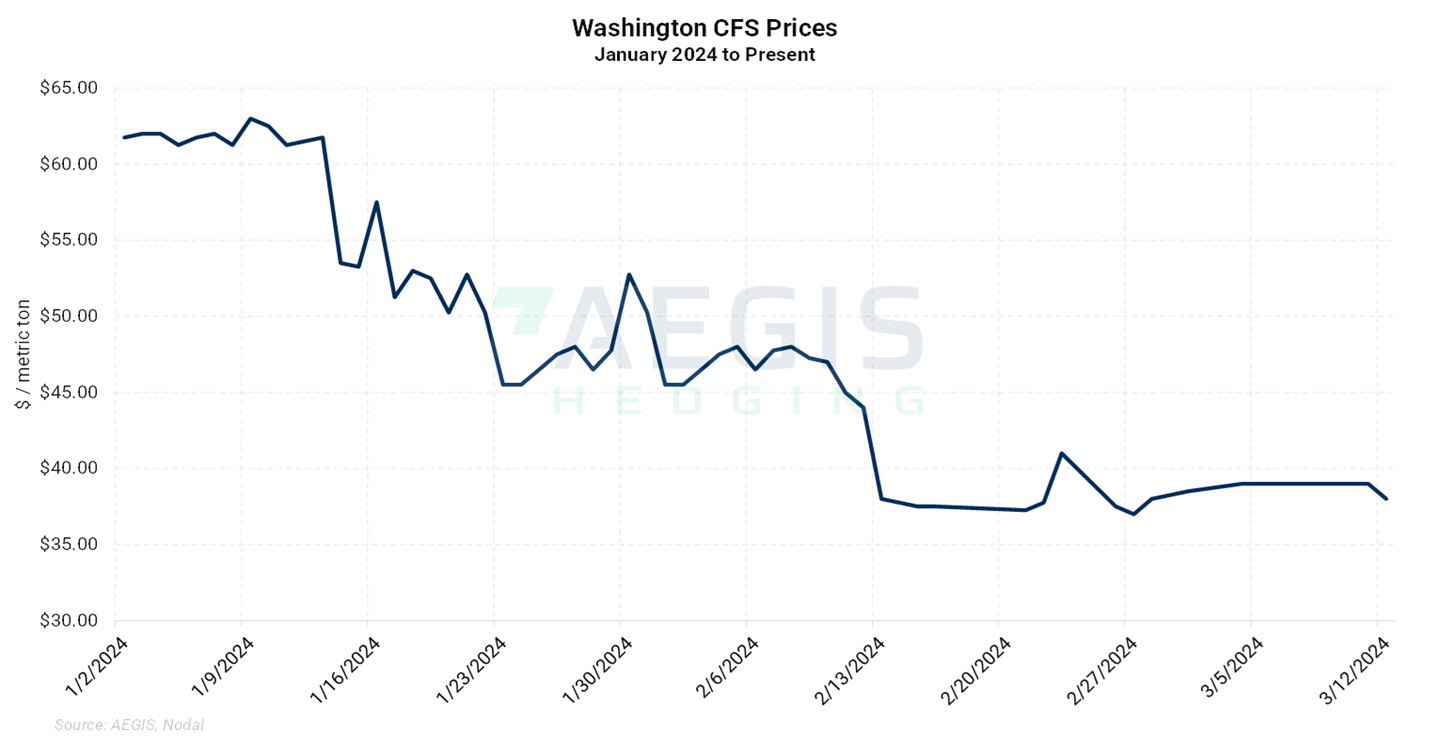

Figure 3. Washington CFS Prompt USD/mt January 2024 - Present

|

|

|

2024 Average Daily Price: $48.08

|

|

2024 Highest Daily Price: $63.00

|

|

(January 9th, 2024)

|

Figure 4. California LCFS Net Credits & Cumulative Bank Volume - Quarterly

Figure 5. California LCFS Net Credits & Cumulative Bank Volume - Yearly

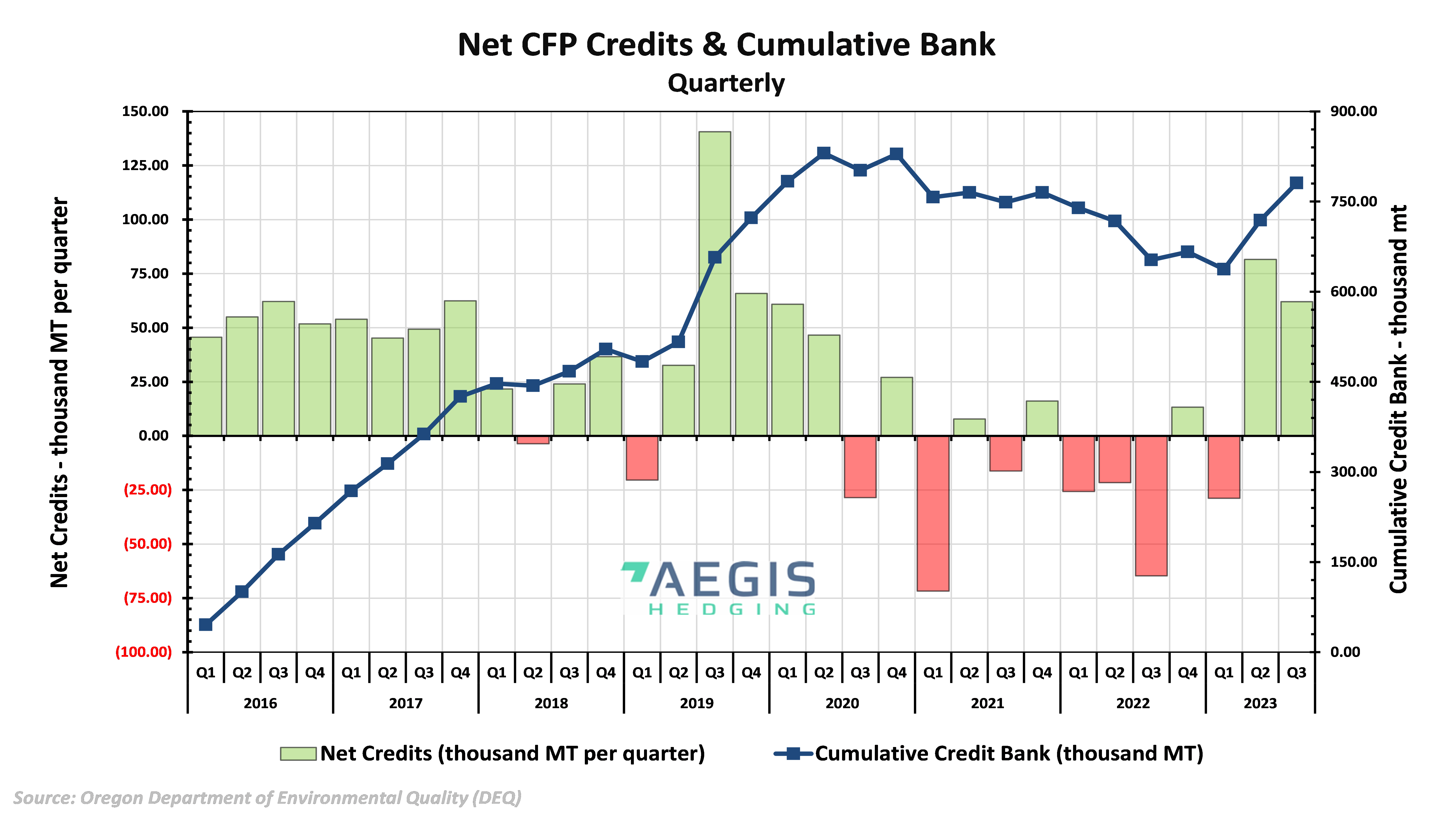

Figure 6. Oregon CFP Net Credits and Cumulative Bank Volume - Quarterly

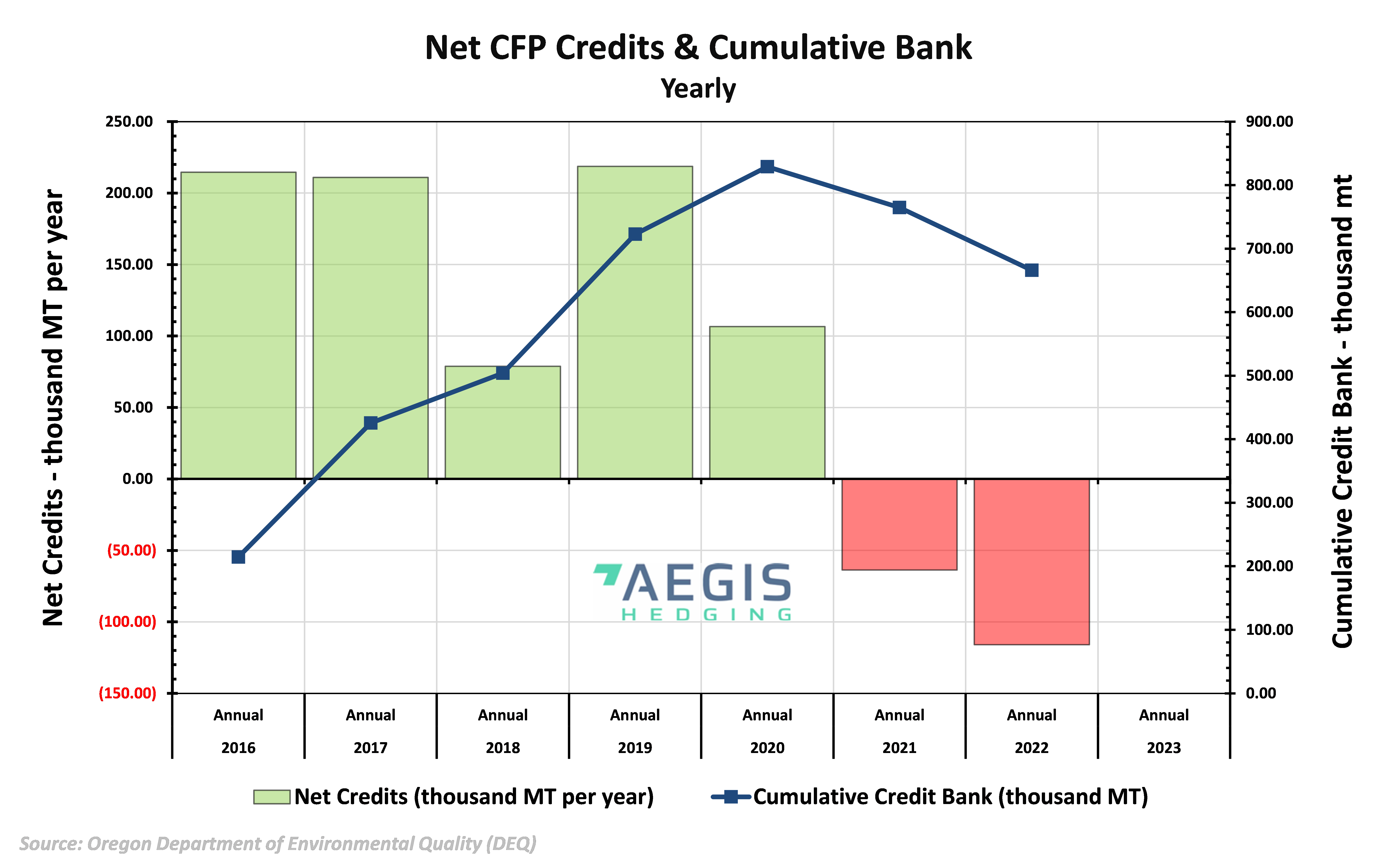

Figure 7. Oregon CFP Net Credits and Cumulative Bank Volume - Yearly

Questions? Contact our team for more information: environmental@aegis-hedging.com

CONFIDENTIAL – UNAUTHORIZED THIRD-PARTY DISTRIBUTION PROHIBITED