Latest Insight

Last Look: Oil snaps its two-week losing streak, finishing $1.63 higher this week

The Inflation Reduction Act (IRA) signed into law on August 16, 2022, introduced several new renewable energy credits including the 45Z Clean Fuel Production Credit which supplants the $1.00/gallon Blenders Tax Credit (BTC) starting in 2025.

The 45Z CFPC is eligible to domestic producers of all transportation fuels “suitable for use in a highway vehicle or aircraft” that achieve a lifecycle emissions rate below 50 kilograms of carbon dioxide equivalent per million BTU. The CFPC is not currently eligible for imported biofuels but the IRA does not stipulate that the fuel must be consumed in the US, effectively subsidizing US exports of qualifying renewable fuels. The 45Z covers fuel produced between January 1, 2025, and sold before December 31, 2027.

Under the current regime, the $1.00/gallon BTC is earned by the blender of biomass-based diesel, renewable diesel, and sustainable aviation fuel (SAF) irrespective of carbon intensity. The shift to a broader spectrum of transport fuels opens up avenues for cellulosic ethanol, renewable natural gas (RNG), and hydrogen to earn new incentives under the IRA. The 45Z will also supplant the current 40B SAF credit available from January 1, 2023, to December 31, 2024.

The base amount of the 45Z CFPC ranges from $0.20/gallon for nonaviation fuels to $0.35/gallon for aviation fuels inflation-adjusted to 2022 dollars. If prevailing wage and apprenticeship requirements are met the base credit is increased by a multiplier of five, or $1.00/gallon for nonaviation fuels to $1.75/gallon for aviation fuels.

The 45Z is calculated by taking the maximum emissions rate of 50 kgCO2e/mmBTU less a fuel’s emissions rate (ER) divided by 50 and multiplied by base rate:

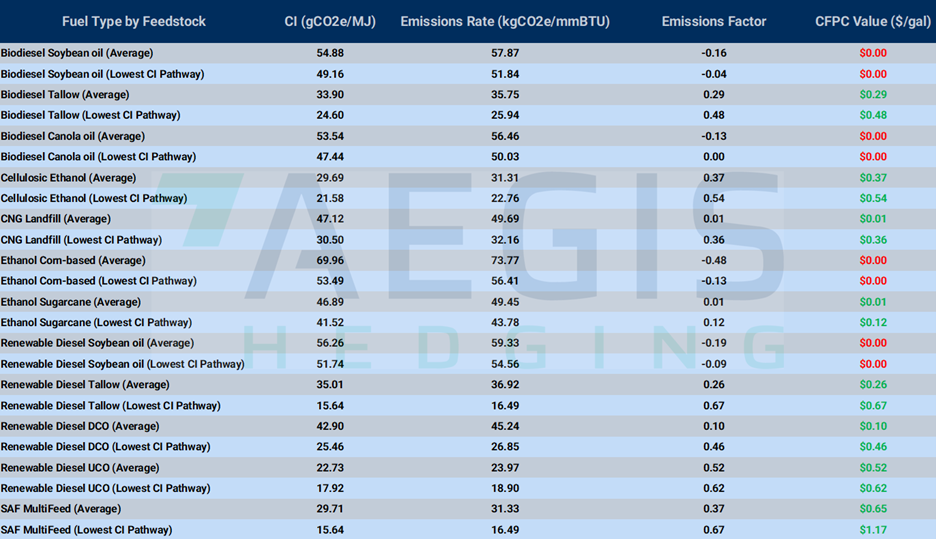

45Z CFPC = (50 – ER)/50 x Base Rate

The emissions rate is determined by the Greenhouse Gases, Regulated Emissions, and Energy use in Transportation, or GREET model, developed by the Department of Energy’s Argonne National Laboratory. The model determines the lifecycle analysis (LCA) for individual fuels and feedstocks.

The GREET model available to the public provides emissions rates (ER) by product and feedstock. GREET does not provide carbon intensity (CI) scores per pathway as done by California’s Low Carbon Fuel Standard (LCFS).

A comparison of the ERs in the publicly available 2022 edition of the GREET model showed scores considerably lower than what has been observed over the past 12 years of the California LCFS program. For this reason, AEGIS opted to analyze the performance of approved pathways under California’s LCFS. The IRS must publish a table of ERs which will allow for a precise examination at a later date.

An analysis of existing California LCFS pathways shows biodiesel produced using soybean oil (SBO) or canola oil would not be eligible for the 45Z. Nor would renewable diesel produced with SBO. No corn-based ethanol pathway exists that would be eligible for the credit. Profitable pathways exist for renewable diesel production using tallow and used cooking oil (UCO), but producers would be receiving between 30-60% less than they had under BTC. SAF outperforms renewable diesel given its larger base rate of $1.75/gallon.

We believe the D4 RIN will likely strengthen to bridge the gap between the lower values received under the 45Z and the former $1/gallon BTC, particularly if the EPA adjusts US federal blending mandates to account for the impact of the IRA.

We do not believe the 45Z will erode LCFS credit value holistically as the program’s current proposed auto-acceleration mechanism (AAM) would be triggered at some point resulting in an upward correction the following year. Other state based LCFS programs may need to adopt AAMs to account for the impact of the 45Z. Lastly, we believe the 45Z will open arbitrage opportunities for US renewable fuels to Canada and potentially Europe, while the US feedstock slate will shift away from seed oils in favor of UCO, tallow, and second-generation, non-food feedstocks. This shift is already evident in the increased imports of foreign UCO and tallow to the US since the IRA was signed into law.