Latest Insight

Last Look: Oil snaps its two-week losing streak, finishing $1.63 higher this week

The extent to which California’s Low Carbon Fuel Standard (LCFS) can absorb rapid growth in domestic renewable diesel (RD) production is a preeminent question among stakeholders. The nation’s longest-standing, state-based climate initiative faces an acute oversupply of LCFS credits. At the same time, uncertainty from a shifting regulatory environment looms over the RD and sustainable aviation fuel (SAF) industry, while similar state-based programs vie for product.

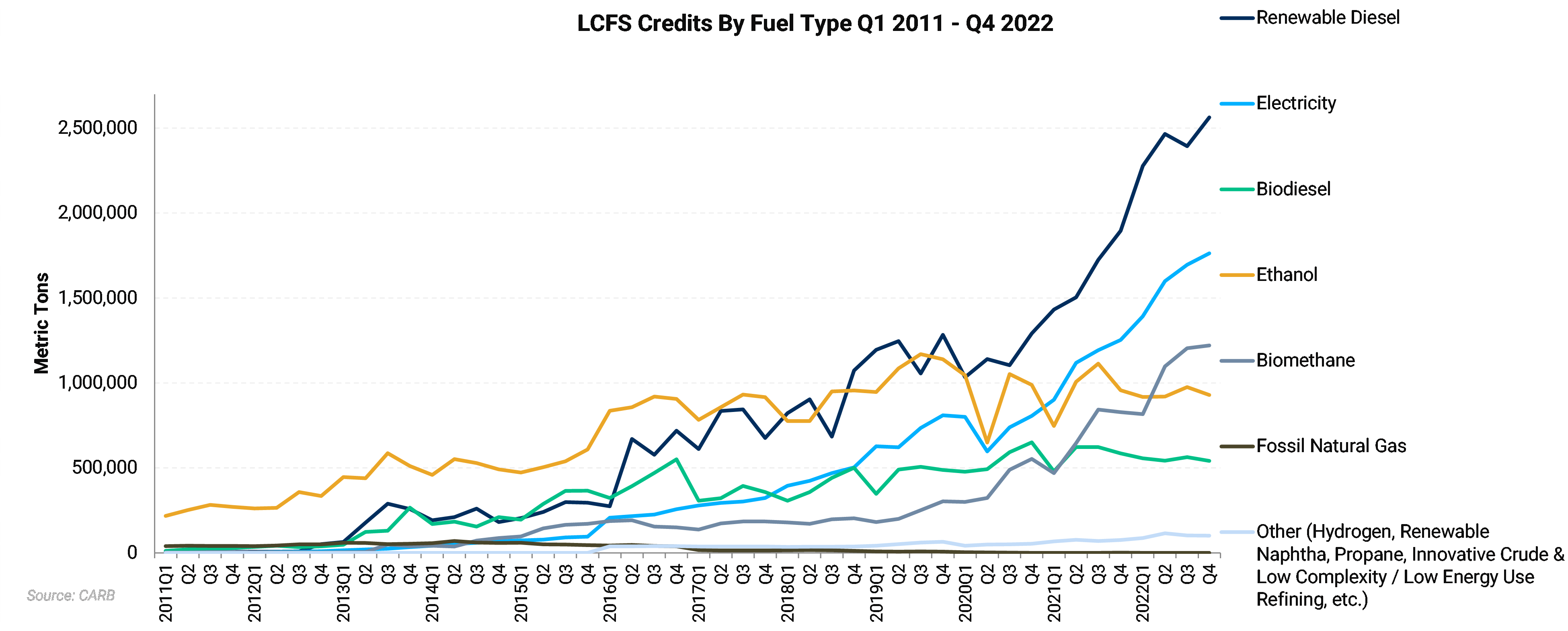

The answer holds outsized implications for the future supply and pricing of LCFS credits as the fuel is the top credit generator under the program, and rapid renewable diesel production growth has led to the development of a record credit surplus of over 15 million credits. This bank is expected to grow significantly over the coming quarters until California’s Air Resources Board (CARB) adopts measures to increase the stringency of the program.

Renewable diesel accounted for 48% of California’s LCFS credit generation in 2022. This proportion has grown swiftly since the renewable diesel revolution kicked off in 2021.

California accounted for 99% of the nation’s renewable diesel consumption in 2021, according to the EIA. Rapid growth in domestic renewable diesel production has seen California’s volumetric consumption rise even as the state’s share of total US production capacity declined to just over 74%, according to AEGIS estimates.

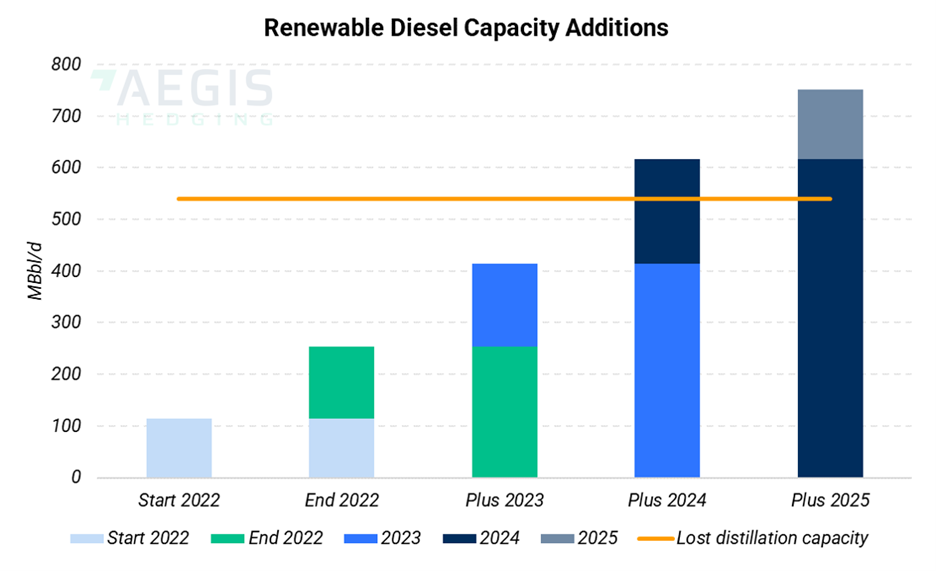

US renewable diesel production capacity surged 119% in 2022 compared to the year prior, ending the year at nearly 2.5 billion gallons/yr, and is set to rise another 41% over the course of 2023. By 2024, renewable diesel capacity will reach nearly 4.4 billion gallons, up 77% from 2022.

With its added LCFS credit incentive, California will be a prime destination for these new barrels. While higher prices for the Oregon and Washington LCFS programs could claw away volumes as the programs mature, this has not happened on a material level at this time and thus was not factored into our analysis.

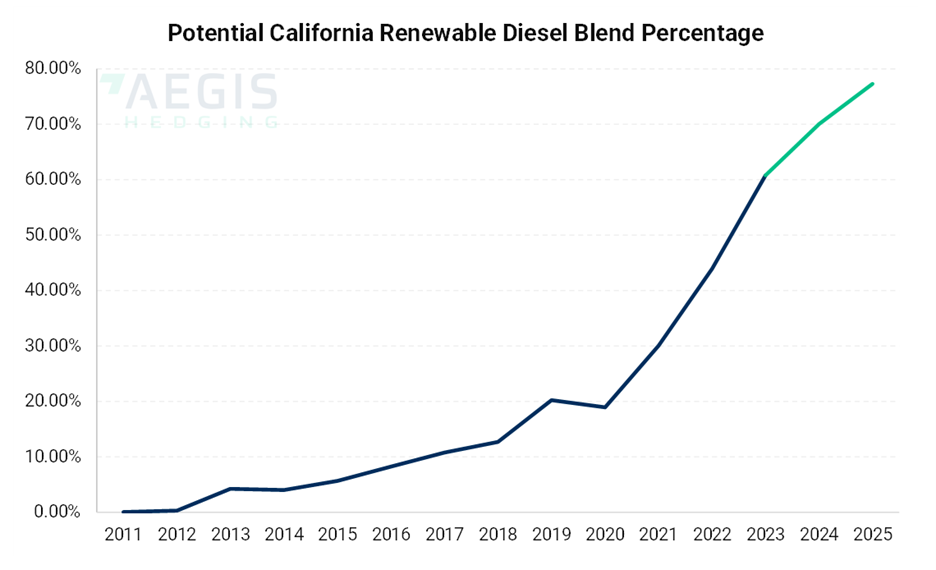

Renewable diesel comprised roughly 44% of total California diesel consumption in 2022 and is on track to account for roughly 61% this year. If California were to absorb renewable diesel at current growth rates, this blend rate could exceed 77% by 2025.

Renewable diesel generated 9.69 million LCFS credits in 2022 and is on pace to account for 13.58 million this year. By 2024, RD will add 15.85 million LCFS credits—more than the existing overhang of surplus credits. This could grow to 17.71 million credits by 2025, according to AEGIS estimates.

Yet this influx of robust credit generation will come up against the state’s more stringent scoping plan. Anticipated to come online in 2024, most expect the state regulatory body, California Air Resources Board (CARB), to aim for a 30% carbon intensity (CI) reduction by 2030. They have also stated they considering 25% and 35% CI reduction by 2030, but with the large overhang of credits, a 25% CI seems unlikely, and should be at least the 30%.

CARB also aims to grapple with the acute oversupply of credits by issuing an “auto-acceleration mechanism,” which would tighten GHG reduction goals if certain indicators are triggered.

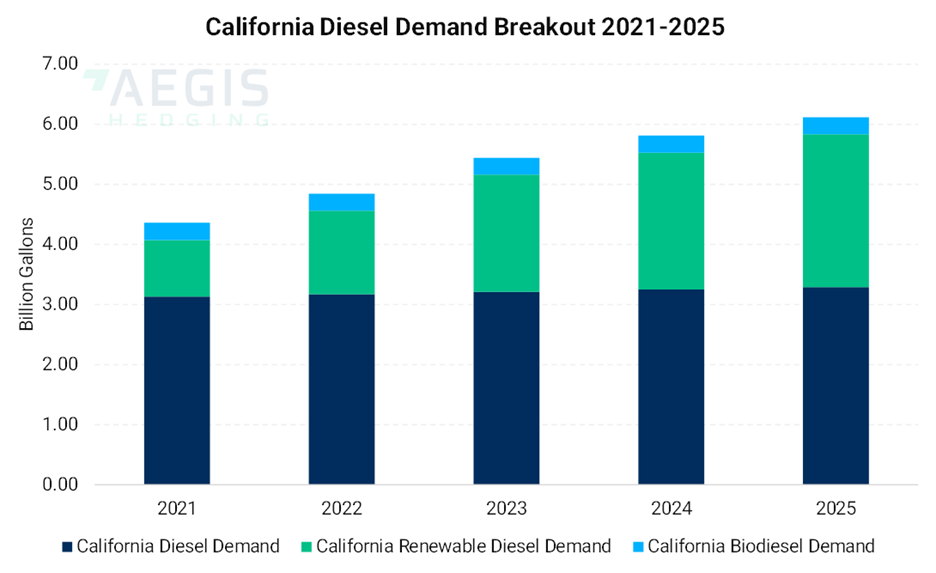

Renewable diesel clearly has the potential to displace great volumes of diesel, yet we also see California diesel demand growing over the course of this period. Renewable diesel could displace a great deal of on-road fuel demand but will also play a leading role in locomotive fuel and marine fuel demand.

Biodiesel is expected to play a declining role in California's carbon emissions goals. The fuels’ percentage of a growing blend pool could decline to around 4.6%, a development that is already playing out in California Air Resource Board (CARB) data. Soybean oil production returns are already proving increasingly dismal this year as concerns over soybean acreage and yields squeeze margins. Furthermore, biodiesel production using soybean oil and other high carbon intensity (CI) feedstocks like camelina oil is not eligible for the 45Z production tax credit under the Inflation Reduction Act, which uses a baseline of 50 CI.

This analysis assumed 10% of renewable diesel production capacity would be used to generate sustainable aviation fuel (SAF). If state-based initiatives such as Illinois’ $1.75/gallon SAF credit expand, the proportion of SAF produced may grow. Illinois’ SAF credit took effect this month and will run through 2033, making the state the most lucrative in which to consume SAF.

SAF suffers from higher production costs, a significant yield loss, and insufficient credit value to cover its added expense, requiring a sizeable state-based or federal credit to allow the fuel to outcompete RD for feedstocks and production capacity. SAF also has a higher CI score at around 38.23 gC02e/MJ compared to 36.92 gC02e/MJ for RD.

Not all the planned RD/SAF projects will come online and we have excluded those most at risk from our analysis. Others could shut or run at reduced rates should market conditions trim margins past breakeven levels for prolonged periods of time.

Here we look to the renewable feedstock market as the dictating factor given limitations on marginal supply. Increasing demand for feedstock should drive up costs and the D4 RIN will face difficulties keeping pace given mounting oversupply fears pressuring returns.

Facing a tight margin environment, the return of stronger LCFS prices will ensure California continues to attract the lion’s share of the RD produced and imported to the US. This dynamic will begin to take shape as more stringent targets are issued in 2024 and further solidified in 2025 following implementation of the state’s acceleration mechanism. The importance of monitoring regional RD and SAF margins is paramount as a complex system of renewable fuels programs sets the stage for competing emissions reductions goals, not just among states, but also corporations and countries.