Latest Insight

Last Look: Oil snaps its two-week losing streak, finishing $1.63 higher this week

To quickly access the page content, please click on the links below:

|

|

||

|

|

||

|

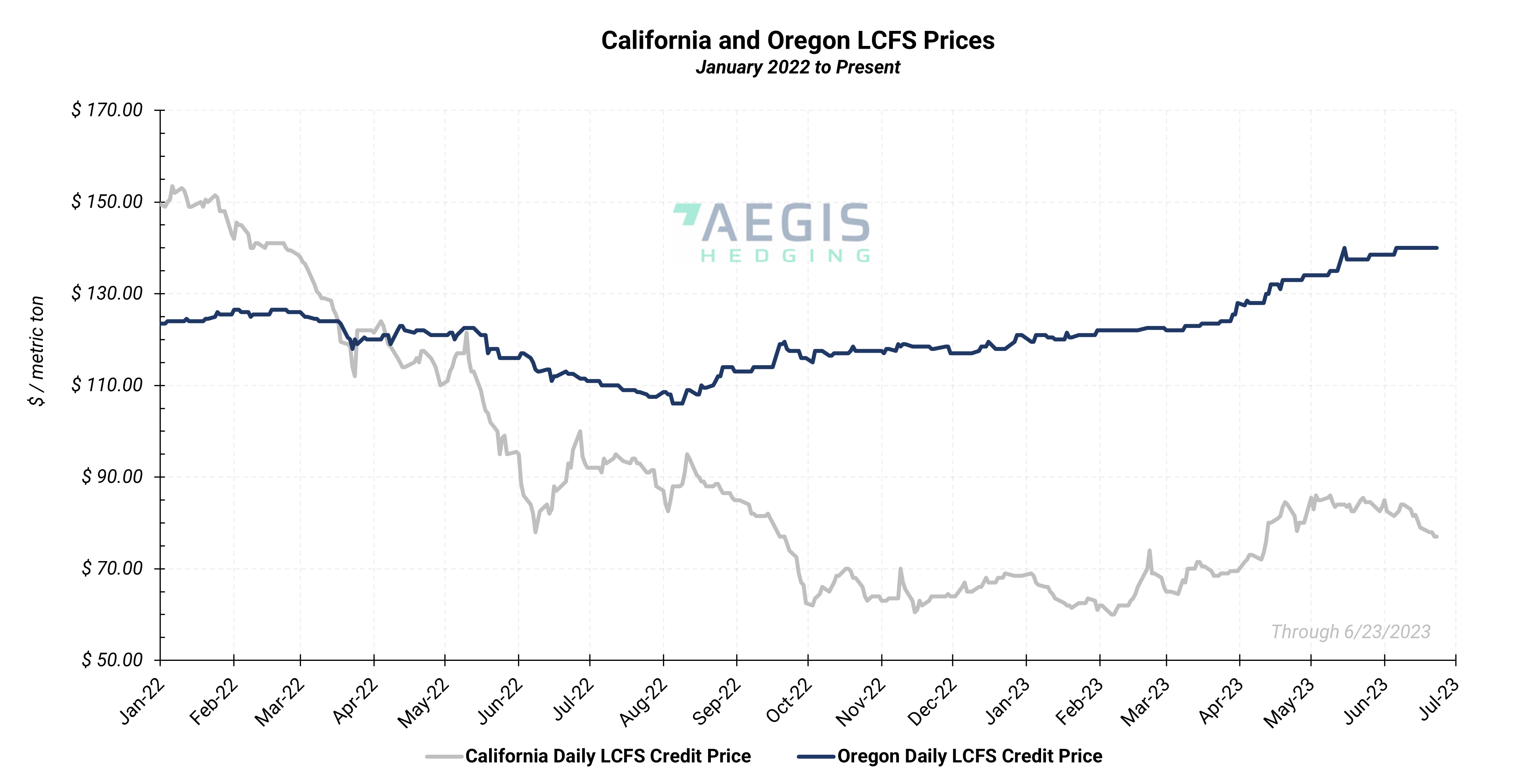

LCFS Spot Contract |

California LCFS |

Oregon LCFS |

|

Price June 23rd, 2023 |

$ 77.00 |

$ 140.00 |

|

Avg. Weekly Price June 20th - June 23rd, 2023 |

$ 77.50 |

$ 140.00 |

|

Average Monthly Price June 2023 |

$ 81.08 |

$ 139.72 |

|

|

|

|

|

LCFS Futures Contract |

Pricing |

|

|

Dec. '23 |

$ 78.00 |

|

|

Dec. '24 |

$ 83.60 |

|

|

Dec. '25 |

$ 89.80 |

|

The California Low Carbon Fuel Standard (LCFS) credit market posted material losses across the forward curve last week. Prompt credits shed $3.65/t, or 4.49%, to average $77.50/t, last week. June credit prices ended the week at $77.00/t, marking the lowest levels since mid-April. The prompt market had been in a choppy holding pattern since early May before entering a downward trend in early June.

LCFS strength had been driven by trader buying and strength in futures markets as the credits become more attractive options ahead of the California Air Resource Board’s new, more stringent scoping plan.

The forward structure flattened for the remainder of 2023 with a modest contango reemerging during the first two quarters of 2024.

The California’s Air Resource Board’s (CARB) last workshop discussed an “auto-acceleration mechanism” as unused LCFS credits rose to record highs. During the workshop California regulators indicated that the final scoping plan may not take effect at the start of the new year much to the disappointment of stakeholders. The regulatory body indicated that the acceleration mechanism would likely not take effect until 2H 2025.

|

||||

|

RIN Spot Contract |

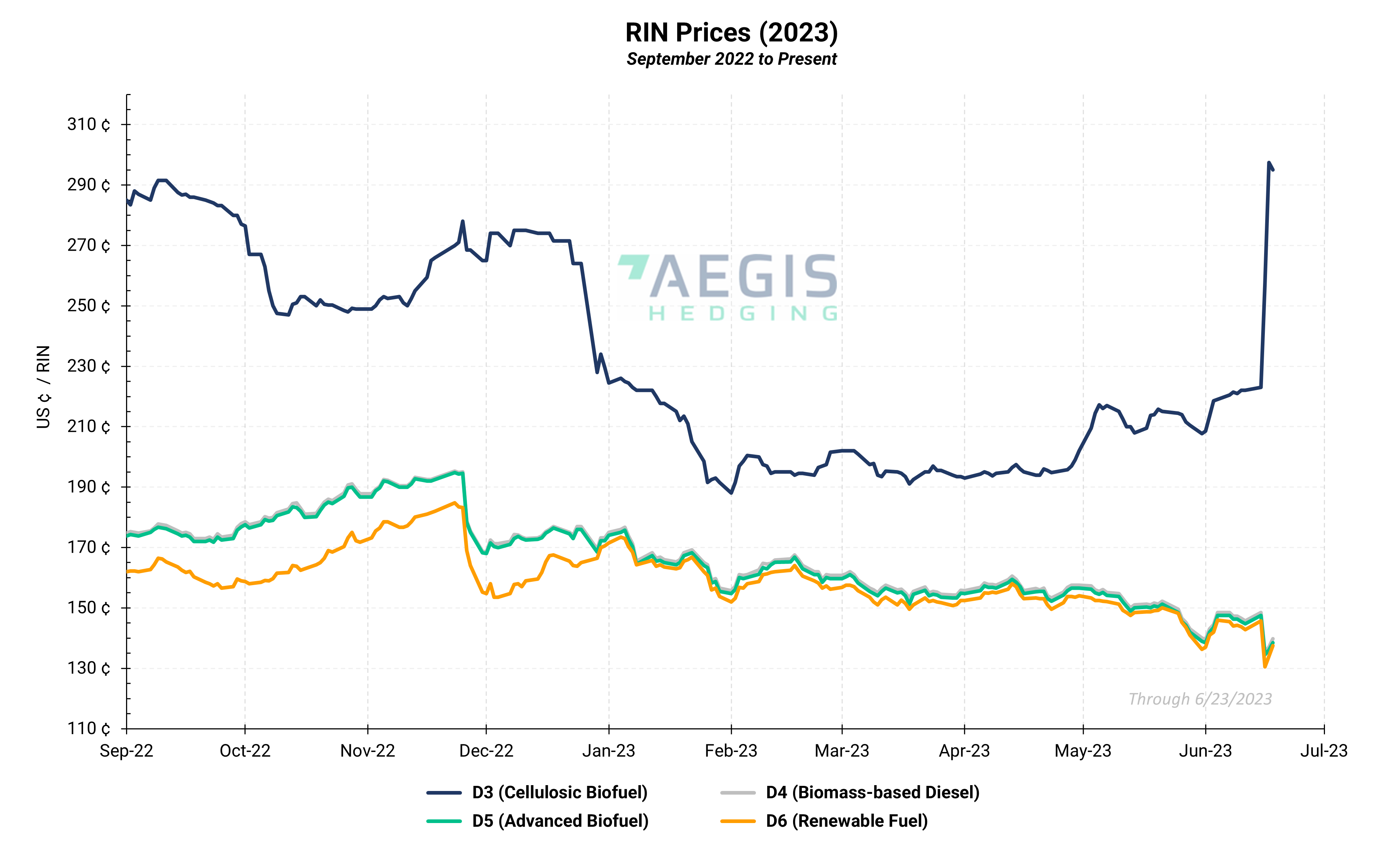

D3 |

D4 |

D5 |

D6 |

|

Price June 23rd, 2023 |

$ 2.95 |

$ 1.40 | $ 1.39 | $ 1.38 |

|

Avg. Weekly Price June 20th - June 23rd, 2023 |

$ 2.68 |

$ 1.40 | $ 1.39 | $ 1.37 |

|

Average Monthly Price June 2023 |

$ 2.29 |

$ 1.44 | $ 1.43 | $ 1.41 |

Current year vintage D4 RINs shed $0.07/RIN, or 4.66%, on average last week. The market ended the week as high as $1.398/RIN after bottoming out at $1.355/RIN on June 21 following the official release of the EPA final ‘Set Rule.

The historic ruling set the demand curve for renewable fuel use during crucial expansion years for the rapidly growing renewable diesel (RD) and sustainable aviation fuel (SAF) industry well short of current and future production, dealing a blow to RD, SAF and BD industries.

The ‘Set Rule’ greatly underestimated the impact of surging renewable diesel growth, with the decision driven primarily by concerns over feedstock supply. In a glimmer of hope for the renewable diesel industry, the EPA left the door open for adjustments to the final ruling by taking into consideration a wide-ranging list of indicators.

The EPA slashed the cellulosic requirements after cutting the eRIN program from the final rules, yet in doing so, still carved out multi-year expansions for cellulosic fuels. The EPA will continue to pursue the eRIN program and is seeking further comment.

The cellulosic volumes were set based on the assumption that the EPA would not need to issue a cellulosic waiver. In other words, the EPA sought to mandate volumes achievable by the existing cellulosic pathways. Based on the market reaction, these volumes erred on the high side and will prove supportive of expansion in the renewable natural gas (RNG) space.

The D3 cellulosic biofuel market—the credits mainly representing biogas production—reached record highs trading from $2.40/RIN to as high as $3.00/RIN. A market for 2024 vintage D3s developed between $2.60 and $2.75/RIN.

The issue of SREs still overhangs the market, yet it is unlikely any will be approved under the Biden administration.

In February, United Refining was denied its SRE hardship waiver by the Third Circuit court, a move which would lead to additional demand to the marketplace. Trade organization Growth Energy entered comments in support of enforcing SREs in its case against the EPA. A full denial of all SREs would represent more than 1.6 billion RINs.

Prior to this, the approval by a federal court of a SRE for Calumet Special Products 30,000 b/d refinery in Montana provided bearish undertones to RIN markets.

SREs were carved out in the Renewable Fuel Standard (RFS) for refiners producing 75,000 b/d or less which could prove compliance with the RFS—i.e., purchasing RINs—resulted “undue economic hardship.”

The EPA retroactively overturned 69 Trump-Era SREs starting in April of last year by denying 31 SRE waivers for 2018 and then denying all SRE petitions for 2016 through 2020. Denying SREs is bullish for RINs markets as refiners must enter the marketplace to purchase RINs to cover compliance obligations which were originally waived.

A court ruling earlier this month halted compliance obligations for two refineries with existing SRE petitions taking issue with the retroactive nature of the SRE denial.

If approved the SRE ruling will prove very bearish for the wider RIN marketplace as participants will view the decision as a shift in the EPA’s approach to granting SREs. Notes from the court were strongly in favor of granting the SREs, as the court made it clear it intends to handle SREs as originally intended by the RFS—i.e., waive RFS compliance if undue hardship can be demonstrated—and to allow waivers which were issued in an “unlawful retroactive application.”

Questions? Contact our team for more information: environmental@aegis-hedging.com