Renewable Diesel Margins Decline on Diesel Losses, Weak Credit Markets

- US renewable diesel (RD) margins lost ground as easing Mideast tensions drove diesel losses late in the week. Lower feedstock prices limited losses, while weaker LCFS and RIN prices eroded returns.

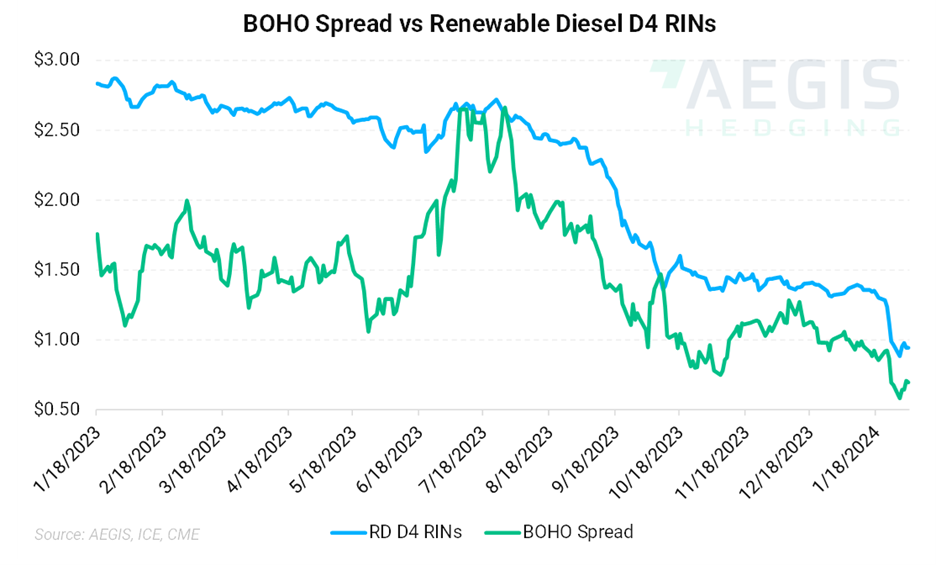

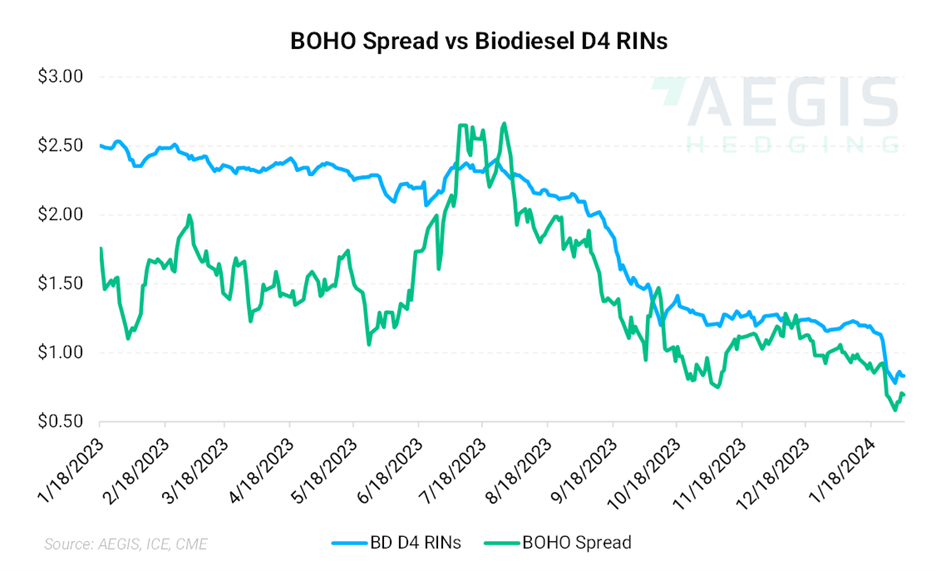

- The Bean Oil-Heating Oil (BOHO) widened off the lowest level in nearly four years to $0.69/gallon to close the week, firming $0.02/gallon, or 2.7%, from $0.68/gallon the week prior.

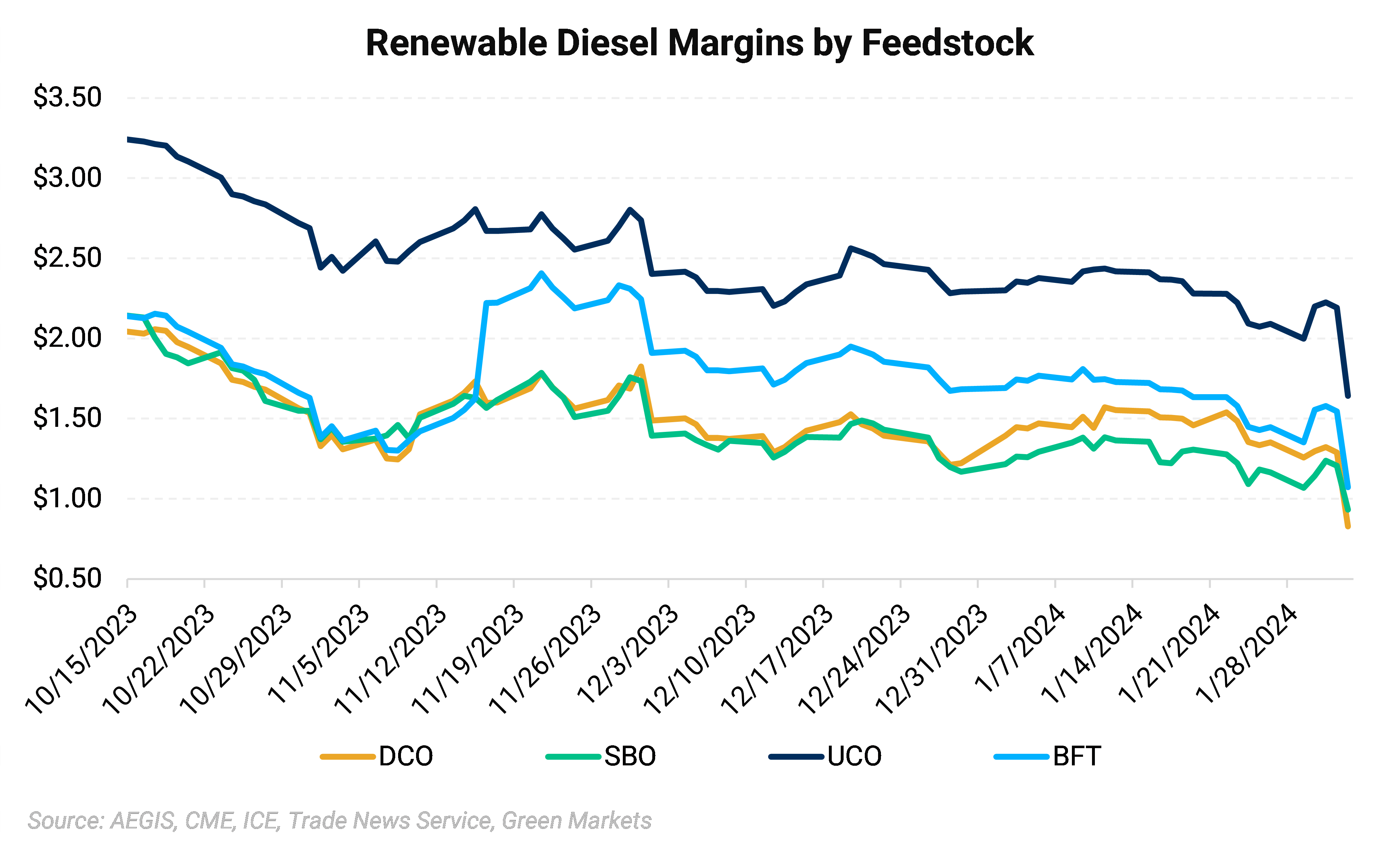

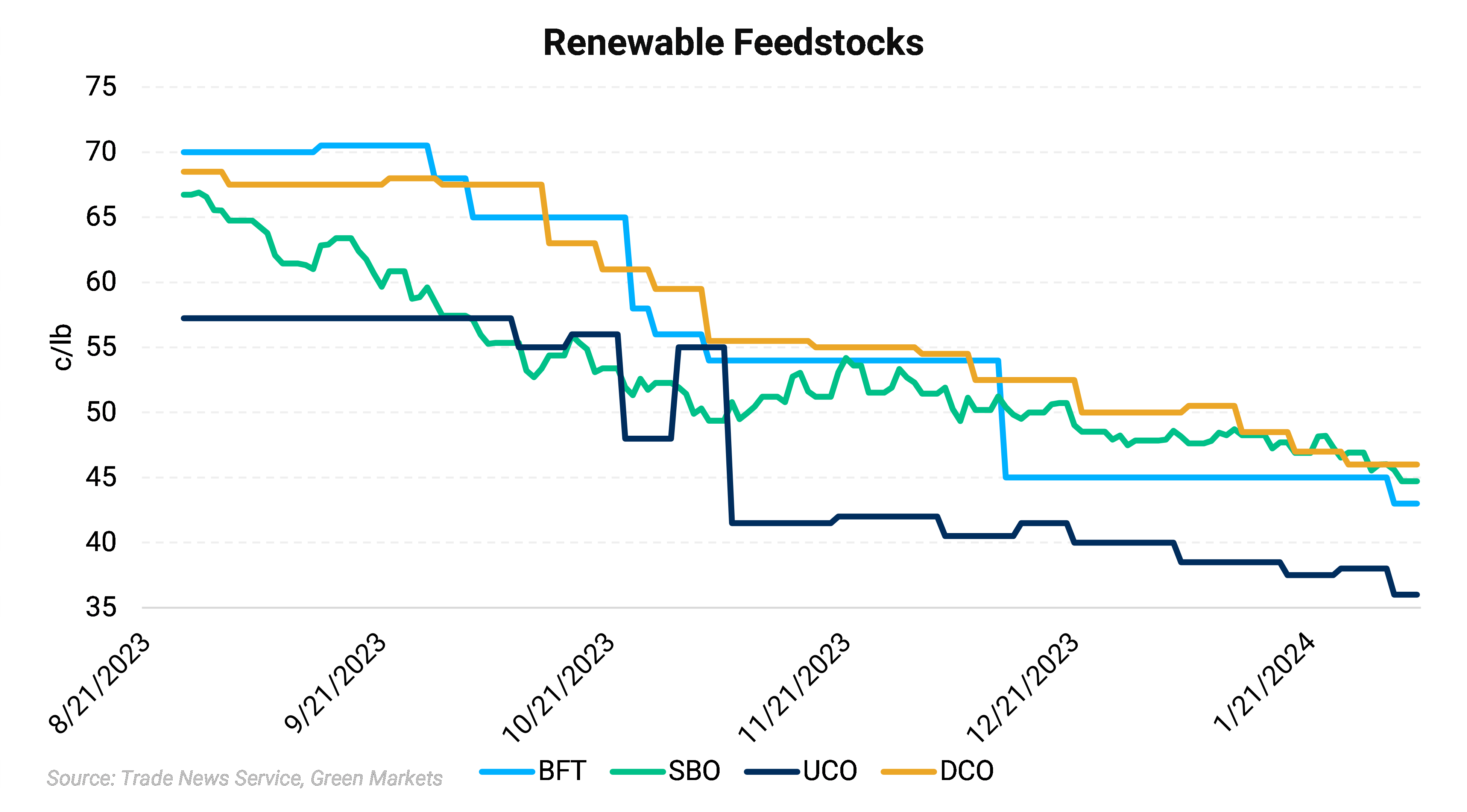

- Used Cooking Oil (UCO) remained the highest returning feedstock at $1.64/gallon, falling under the $2.00/gallon mark for the second time this year. UCO imports have tempered US UCO prices despite mounting demand, yet UCO imports appear to be slowing for the month. Tallow margins remained the second-best performing feedstock at $1.07/gallon on average last week. Mounting tallow imports have helped preserve US Gulf coast BFT margins.

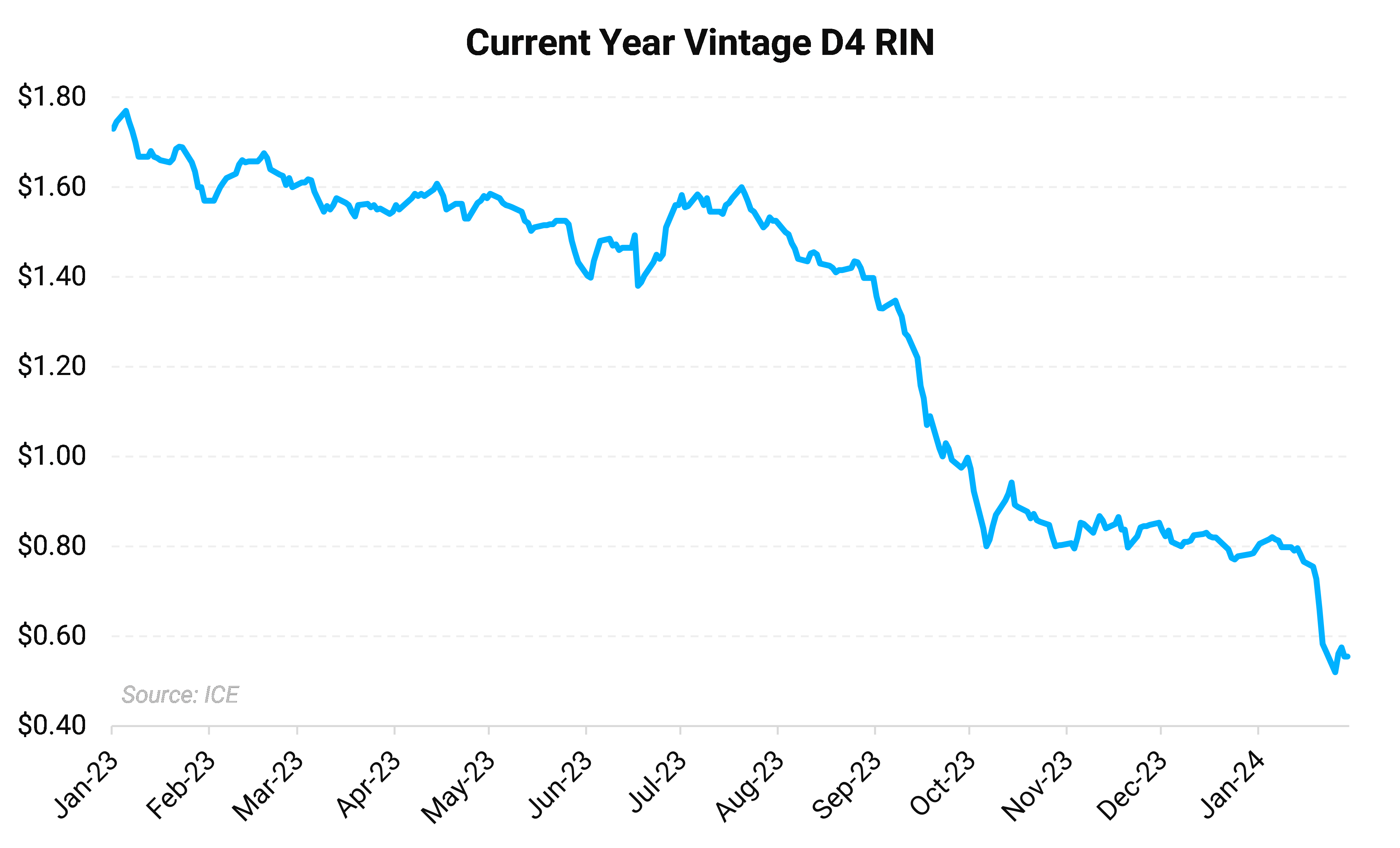

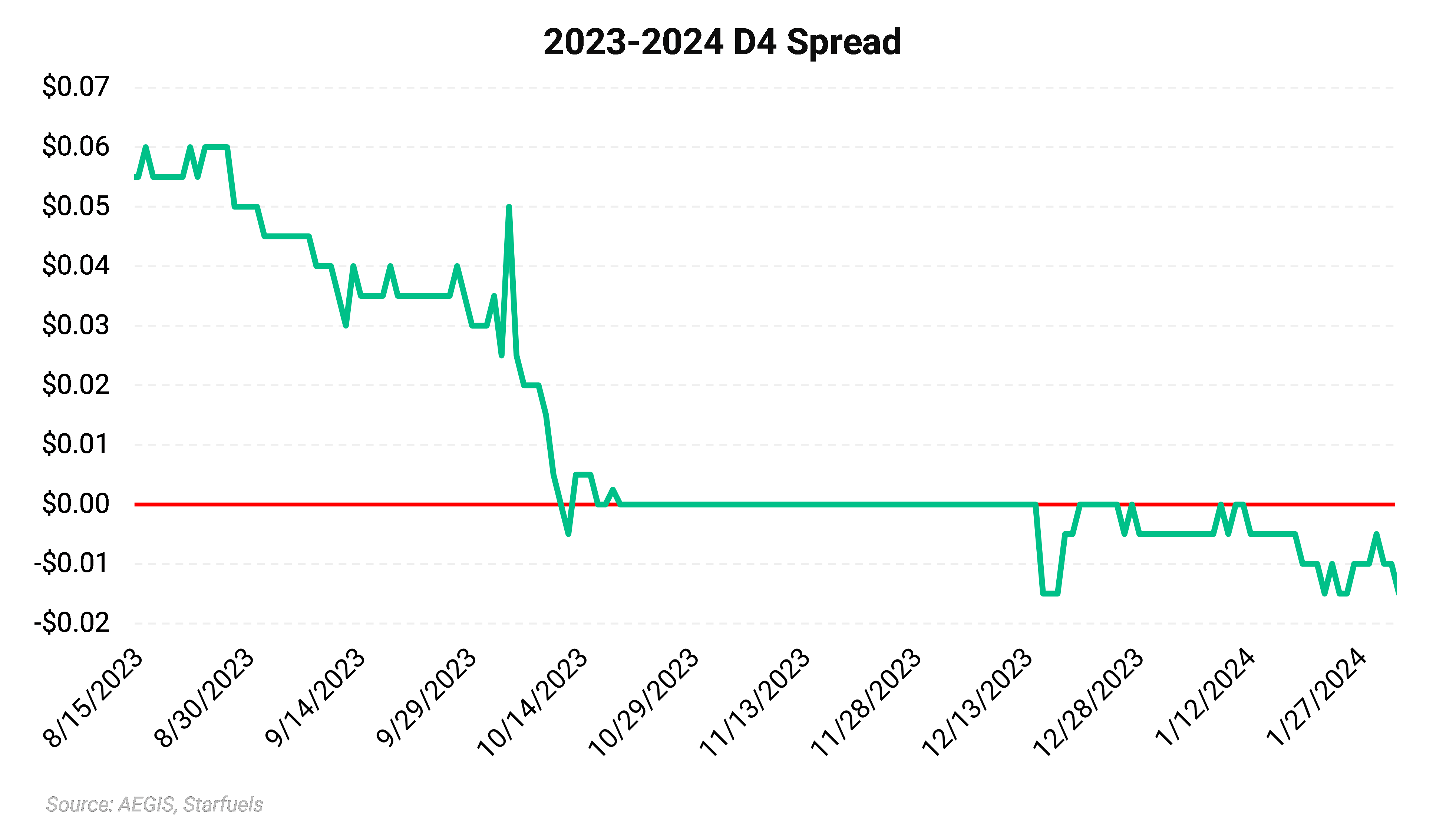

- RINs posted modest week-over-week losses even as the BOHO spread widened over the course of the week. Current year vintage D4 credits shed just over $0.01/RIN to close the week at 55.50c/RIN. The 2023 vintage market slumped $0.02/RIN, with the inter-vintage spread widening to -1.5c.

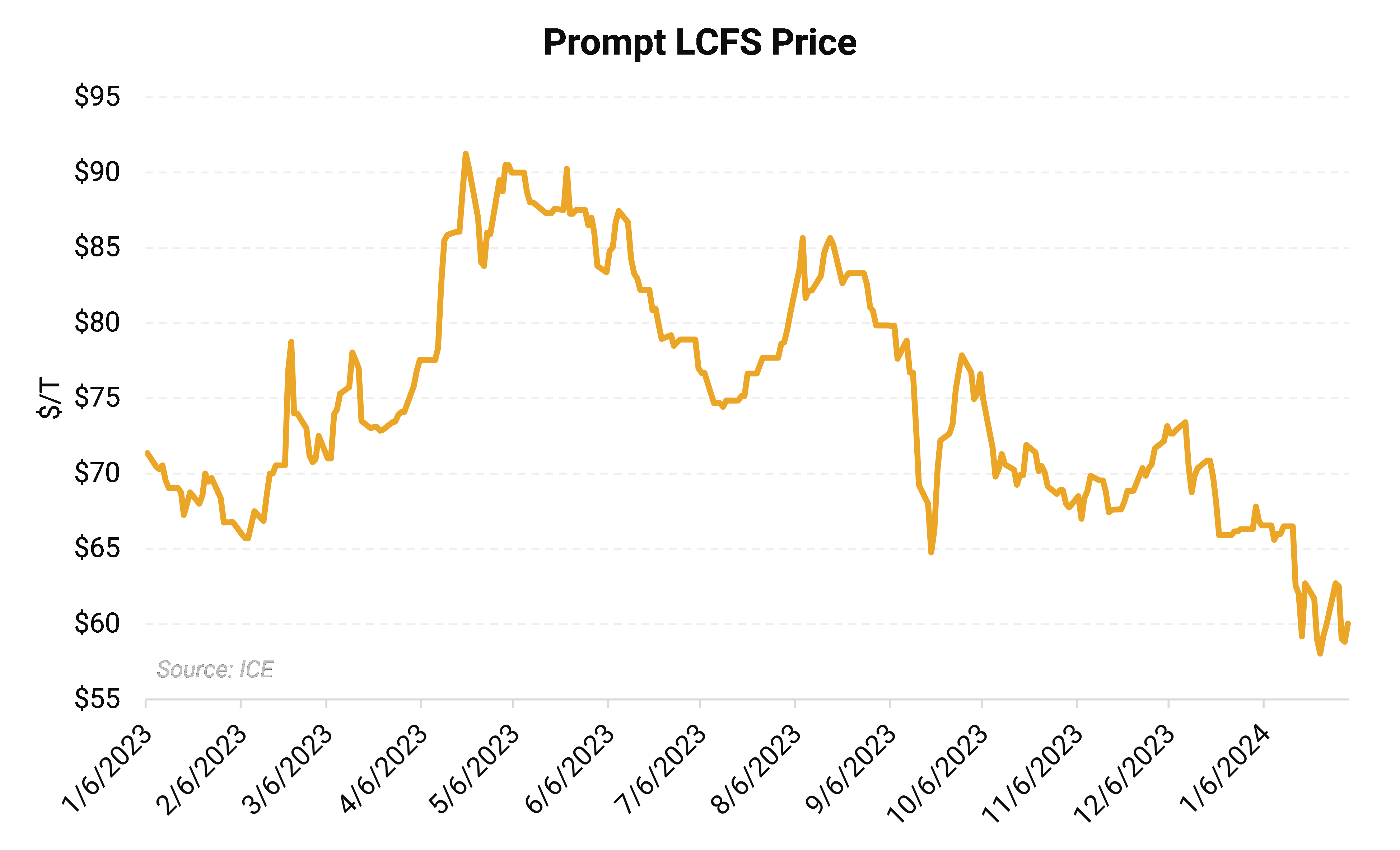

- California Low Carbon Fuel Standard (LCFS) markets remained bearish as a fresh record build in unused credits spurred selling. Prompt credits fell $2.7/t, or 4.3%, to $60.00/t. The forward structure showed $2.00/t of contango heading into December 2024, up from $1.3/t the prior week.

- The February lineup shows three Singaporean RD vessels booked for California delivery, according to preliminary Vortexa data. A 253,000 Bbl vessel arrived in Los Angeles, California on February 3. A 323,000 Bbl vessel is set to make delivery in Los Angeles, California, on February 21, followed by a 178,000 Bbl cargo arriving in San Francisco, California, on February 26.

- At least three RD bookings were reported for January delivery in California totaling 629,000 Bbl. The month of January saw Oregon emerge as an alternative destination for both domestic and foreign RD production as higher Oregon LCFS prices improved RD returns in the state. A 317,000 Bbl vessel arrived in Portland, Oregon, on January 20 after departing the US Gulf Coast. A 320,000 Bbl Singaporean vessel discharged in Portland, Oregon, on January 23.

- At least three RD bookings were reported for December 2023 delivery in California totaling 541,000 Bbl. At least four RD bookings were reported for November delivery totaling 650,000 Bbl. Three RD vessels originating from US Gulf coast locations arrived in California during November totaling more than 1,000,000 Bbl.

- The pace of Gulf coast feedstock imports appeared to slow in the first week of February. At least one Chinese UCO cargo was set for first week February arrival, according to preliminary Vortexa data. No tallow cargos were on the line up thus far. The US took at least four tallow cargos in January, evenly split between California and Louisiana.

- The US Gulf coast typically imports five to six cargoes of UCO each month, primarily from China, but also Vietnam and South Korea. A Chinese UCO vessel is set to reach New Orleans, Louisiana, on February 3, according to preliminary Vortexa data.

- The 5th US Circuit Court of Appeals turned down a request to reconsider its November 22, 2023, decision to block SRE denials for six small refineries. Biofuel industry groups Growth Energy and Renewable Fuel Association sought a rehearing on the grounds that the denials should be brought before the DC Circuit Court. The EPA has received 12 SRE petitions since the 5th Circuit’s November ruling.

- The US Court of Appeals for the 11th Circuit dismissed a SRE challenge by Hunt Refining on January 11, saying the case should be heard by the US Court of Appeals for the DC Circuit. Biofuel industry group Growth Energy welcomed the decision as CEO Emily Skor responded “EPA’s denials of these SRE petitions were ‘nationally applicable’ and have nationwide effect, and challenges to the denials should only have been brought in the DC Circuit.”

- December total RIN generation came in at a record 2.17 billion credits, up 9% from the previous month when total RIN generation reached just over 2.00 billion credits. D4 generation reached a record 840 million credits, up 24% from the previous month and surpassing the previous record of 751 million credits set in May 2023 by 12%. Domestic renewable diesel production accounted for 54% of total D4 output, up from 49.5% the month prior and 47% in October. Foreign renewable diesel made up 9.7% of total D4 generation, down from 11% the month prior. Domestic and imported biodiesel accounted for 35% of the month’s share, down from 39% the month prior and 41% in October. Just 3.8 million D4 credits were generated across domestic and foreign SAF production, accounting for less than one percent of the month’s share.

- The EIA trimmed its forecasts for US renewable diesel production and demand. Domestic production was projected at 229,000 Bbl/d, down 3% from the December Short-Term Energy Outlook. US RD demand was estimated at 252,000 Bbl/d, down 3% from the prior months’ outlook. RD imports for 2024 were cut by 4% to 23,000 Bbl/d. Fresh 2025 forecasts came in at 294,000 Bbl/d for production, 309,000 Bbl/d for demand and 14,000 Bbl/d for imports.

- Zenith Energy received approval for three 12-inch pipelines to transport RD, SAF, or BD to its Portland, Oregon, terminal. Storage at the facility is slated to reach 1.5MM Bbl by 2027. The pipelines will transport fuels from the Willamette River inland pending additional zoning permits and monitoring by the city’s Bureau of Development Services.

- Bakersfield Renewable Fuels (BKRF) is aiming for a first quarter start-up of its 15,000 Bbl/d RD facility. Commercial operations are due to begin in the second quarter. BKRF is a subsidiary of Global Clean Energy Holdings.

- On December 19, California’s Air Resources Board (CARB) released a preliminary LCFS proposal laying out amendments which nearly mirrored those in the Standardized Regulatory Impact Assessment released in September. CARB proposed a 30% reduction in carbon intensity by 2030, including a 5% step-down in 2025. This marks a 50% increase in carbon targets over the original 20% reduction target for 2030. Reductions increase to 90% by 2045 compared to a 2010 baseline. The proposal contained an automatic acceleration mechanism (AAM) which would advance stringency for a given year when unused credits more than triple average deficit generation by advancing the carbon reduction target by two years. Amendments included eliminating the exemption for intrastate jet fuel beginning in 2028 and new tracking requirements for crop-based and forestry-based feedstocks to their point of origin. CARB expects to kick off the required 45-day public comment period in January, with a public hearing set for March 21, 2024.

- The US Treasury Department issued guidance on December 15, 2023, clarifying how SAF will be eligible for tax credits worth as much as $1.75/gallon under the Inflation Reduction Act. The SAF tax credit is only issued to fuels which reduce lifecycle GHG emissions 50% below petroleum-derived jet fuel. The Treasury Department plans to calculate emissions intensity using a modified version of the GREEET model planned for March 1, 2024. The adjusted GREET model could open the door for corn-based ethanol to contribute to SAF supply.

- CARB regulators are still aiming for a Q1 2024 board vote on amendments despite missing deadline to release formal program updates the week ended December 15. The program updates are required for a 45-day public comment period prior to a board vote. The next CARB board meeting is scheduled for January 25-26, 2024, with the following set for February 22-23, 2024.

- Recent fires at Marathon’s Martinez refinery triggered a federal investigation by the Chemical Safety and Hazard Investigation Board (CSB). Fires on November 11 and November 19 at a hydrodeoxygenation (HDO) unit led to spills of RD. Marathon aims to achieve 48,000 Bbl/d of production at its Martinez, California facility by year-end.

- Calumet restarted its 15,000 Bbl/d Great Falls, Montana, facility following a November turnaround. The plant is currently running at 12,000 Bbl/d, a 20% reduction on nameplate. Calumet reported no plans for 2024 maintenance and aims to add 3,000 Bbl,d of capacity in 2025. Lower runs leading up to the turnaround allowed Calumet to build up inventories of renewable feedstock. The facility runs beef tallow, SBO, canola oil and camelina oil. Calumet has a multi-year SAF offtake agreement in place with Shell.

- The 5th US Circuit Court of Appeals ruled to block denials of SREs for six refineries. The SREs cover Calumet’s 57,000 Bbl/d Shreveport, Louisiana refinery, Placid Refining’s 75,000 Bbl/d Port Allen, Louisiana refinery, Ergon Refining’s 26,500 Bbl,d Vicksburg, Mississippi refinery, Ergon’s 23,000 Bbl,d West Virginia refinery, CVR’s 74,500 Bbl/d Wynnewood, Oklahoma refinery, and Allegiance Refining’s 21,000 Bbl/d San Antonio refinery. The court’s decision said the EPA’s blanket SRE rejection was “impermissibly retroactive; contrary to law; and counter to the record evidence.” The decision will add a bearish undertone to an already oversupplied marketplace, save for D3 credits.

- Oregon released second quarter Clean Fuel Program (OCFP) showed renewable diesel as the top-credit generating fuel at 35 percent of total OCFP credit generation, taking quarterly generation to a fresh record. Renewable diesel and biodiesel combined made up 25 percent of the state’s diesel pool, demonstrating the increasing penetration of RD into Oregon. OCFP credits shed nearly $60/t ahead of the release of the report yet continue to trade at hefty premiums to California LCFS credits, making Oregon an economically advantaged destination depending on freight and logistics costs.

- Federal judges defended the EPA’s approach to setting the 2020-2022 blending mandates. US refiners have complained blend requirements were too high based on how the EPA adjusted blending targets to account for projected Small Refinery Exemptions (SREs). The EPA is also facing a separate lawsuit for its 2022 cellulosic biofuel requirement, with biofuel groups arguing that targets were set too low based on projections of actual production and not accounting for the availability of carryover credits for compliance. Refiners have also filed a series of lawsuits in the DC Circuit court challenging the EPA’s move to reject all outstanding SREs this year.

- Montana Renewables refinery by 2025. The Great Falls plant is currently undergoing repairs to a steam recovery system and moved forward a turnaround originally planned for 2024 to November. Calumet is mulling plans to ultimately maximize SAF production at the Great Falls facility.

- Louis Dreyfus aims to build a 1.5 t/year soybean processing plant in Upper Sandusky, Ohio with construction to begin in early 2024. The plant is expected to be completed by 2026 and will have a capacity to produce 320,000 t/yr of RBD soybean oil. Earlier this year, Louis Dreyfus said it will double the capacity of its canola crushing plant in Yorkton, Saskatchewan.

- A California judge ruled that P66’s 67,000 Bbl/d RD Rodeo facility may not operate until permitting issues are resolved. The largest RD refinery conversion in the country is allowed to continue construction. The original permitting work for the plant took nearly a year to complete in May 2022. P66 aims to begin RD production at Rodeo by Q1 2024.

- EPA Fuel Program Center Director, Paul Machiele, said the oversupply of D4 credits is not currently a concern at the EPA as the agency’s primary driver in setting the 2023-2025 mandates was feedstock availability, according to Carbon Pulse. Machiele noted that the surge in imported feedstock was not taken into account when considering the final Set Rule, speaking at the OPIS RFS, RINs and Biofuels Forum in Chicago. Changes to exiting mandates are unlikely to be taken up during an election year. President of Advanced Biofuels Association, Michael McAdams, cited an unnamed source that the earliest the EPA would take action is 2026.

- EPA officials indicated that the next opportunity for addressing the adoption of the contentious eRIN pathway would be when the agency considers blending targets for 2026, according to EPA Fuel Programs Center director Paul Machiele when speaking at the Argus North American Biofuels, LCFS, & Carbon Markets Summit in mid-September.

- CVR Energy Inc. aims to start up the pretreatment unit (PTU) at its Wynnewood, Oklahoma, refinery by the end of 2023. The plant has been running soybean oil and treated corn oil until the PTU enters service. A catalyst change during the second quarter saw throughput drop to 17.8 million gallons, down from 22.4 million gallons consumed during the first quarter. CVR estimates Q3 throughput of 17-22 million gallons.

- Parkland Corp. announced its decision to halt its renewable diesel project in British Columbia, Canada. The company had been coprocessing at its Burnaby Refinery with plans to build a 273,000 gallons/yr RD facility, set to come online in 2026. The company cited rising feedstock costs and advantages to US producers afforded by new credits carved out in the Inflation Reduction Act (IRA). The move could be a harbinger of slowing momentum for the RD industry which has increasingly worried about rising feedstock costs, while the numerous advantages of the US market are likely to open export markets soon.

- The Washington State Senate passed a Sustainable Aviation Fuel (SAF) tax credit, following actions from the state of Illinois which issued its own SAF credit with additional tax advantages for the fuel. Washington aims to establish a $1/gallon credit with a $2/gallon cap as additional value can be earned for fuels with lower carbon emissions. The Illinois SAF credit is set at $1.50/gallon and will run from June 1, 2023, through June 1, 2033, making the state the highest returning market for SAF.

Renewable Diesel

US Gulf coast RD margins tumbled as diesel losses coupled with weakness in credit markets. Softer feedstock prices limited losses. Feedstock imports appeared to be slowing in February according to preliminary shipping data.

UCO remained the highest returning feedstock, averaging a return of $2.05/gallon. Margins tumbled under the $2.00/gallon mark amid material diesel losses on February 2. Spot UCO prices at the US Gulf coast shed 2c, or 5%, to 36c/lb as at least one import vessel reached the region in the first week of February.

BFT margins averaged $1.41/gallon, falling as low as $1.07/gallon to close the week. BFT prices shed 2c/lb, or 4%, week-over-week to 43c/lb. At least two tallow vessels reached the US Gulf coast in January. This follows on at least one vessel in December and two in November. Seven tallow import vessels reached the US Gulf coast over the course of October.

DCO margins averaged $1.20/gallon, reaching as low as $0.83/gallon to close the week. Spot DCO prices shed 1c/lb, or 2%, to 46c/lb.

SBO margins reached as high as $1.24/gallon at midweek before collapsing to $0.93/gallon. Spot SBO price shed 2.2c/lb, or 4.7% over the course of the week to 44.70c/lb.

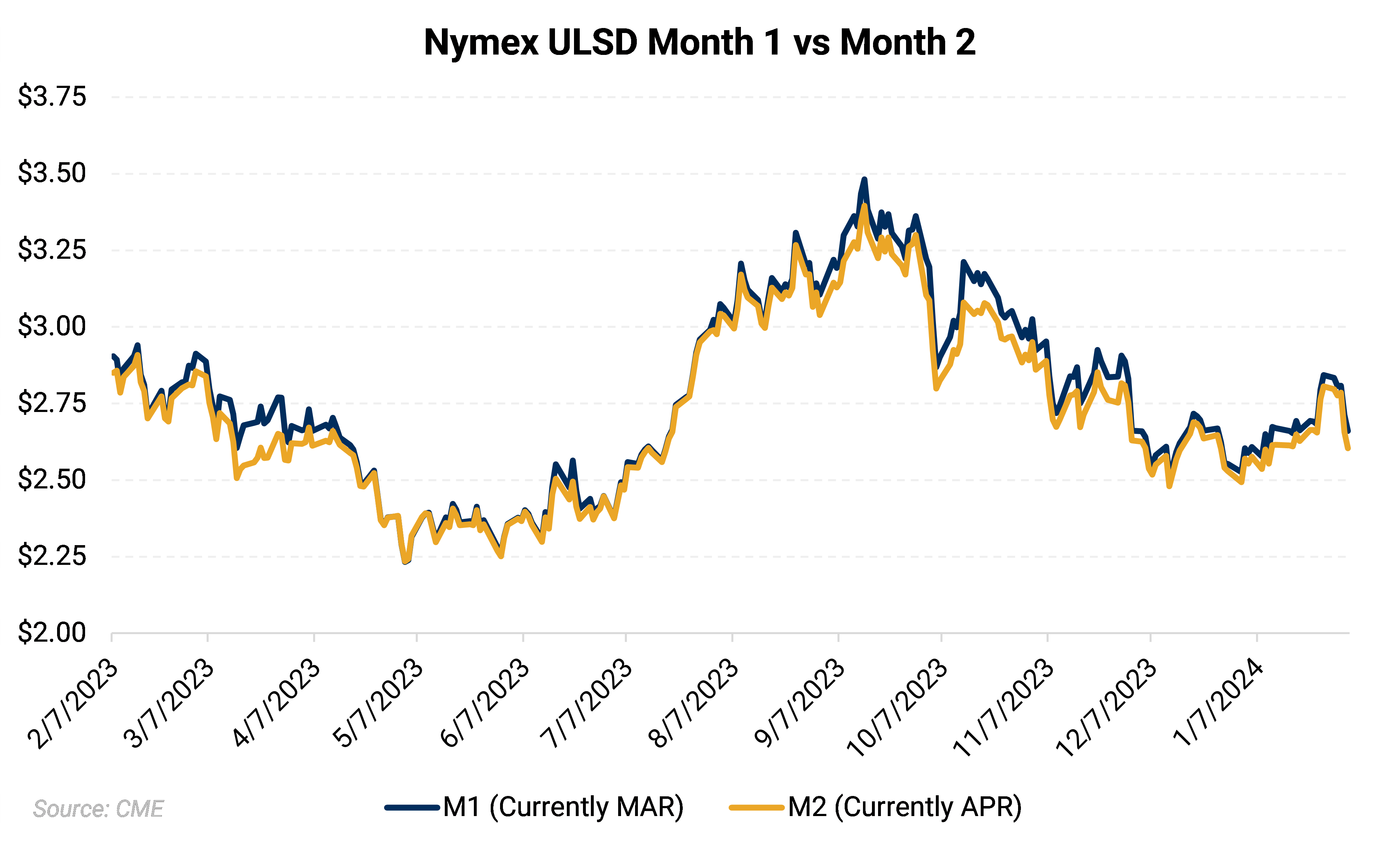

To recap: The week ended January 26 saw RD margins lose ground as significant RIN losses were only modestly offset by diesel strength. D4 RINs shed 25c, or 43%, week-over-week, trimming nearly $0.42/gallon out of RD margins on RIN value alone. Nymex diesel firmed $0.18/gallon, or 6.8%, over the same period. Lower LCFS credit prices acted as a further headwind to the margin environment, while feedstocks were little changed.

The week ended February 2 saw RD margin press lower as diesel losses built on persistent weakness in credit markets. D4 prices have shed 23c, or 29%, since the start of the year, reaching as low as 52c/RIN on January 29, before recovering to 55.50c/RIN on diesel weakness. Lower feedstock prices limited further losses on returns. Diesel losses saw the BOHO spread widen off the lowest level in nearly four years to end the week at $0.69/gallon.

Biodiesel margins, as measured by the soybean oil-to-heating oil (BOHO), reached the lowest level in nearly four years to start the week at $0.58/gallon. The BOHO spread widened to $0.69/gallon by the close of the week, up $0.02, or 2.7%, from the prior week’s level.

D4 RINs shed 1.25c, or 2.2%, week-over-week. The credits started the week as low as 52c/RIN before widening to 55.50c/RIN on diesel weakness. The premium for renewable diesel RINs to the BOHO spread narrowed to 25c/gallon, down 4c, or nearly 14%, from the week prior.

The wider the BOHO spread, the weaker the margin as the main input cost for biodiesel producers, soybean oil, is more costly than the petroleum-based diesel fuel it competes with, compressing margin though the D4 RIN can contribute significantly toward making up for BOHO weakness.

The BOHO spread is a simplistic breakdown of the pulse of the biodiesel industry and is in widespread use by the industry. The BOHO spread does not account for operational costs which can vary drastically from plant to plant, nor the additional margin value afforded by credits and/or the sale of byproducts such as glycerin.

Environmental Credit Markets

RIN markets continued to shed value as market participants grappled with oversupply of D4 credits and the narrowest BOHO spread in nearly four years. Diesel losses late in the week prompted a modest rebound in credit prices.

The 5th US Circuit Court of Appeals turned down a request to reconsider its November 22, 2023, decision to block SRE denials for six small refineries. Biofuel industry groups Growth Energy and Renewable Fuel Association sought a rehearing on the grounds that the denials should be brought before the DC Circuit Court. The EPA has received 12 SRE petitions since the 5th Circuit’s November ruling.

The 5th US Circuit Court of Appeals ruled on November 22, 2023, to block denials of SREs for six refineries. The court’s decision said the EPA’s blanket SRE rejection was “impermissibly retroactive; contrary to law; and counter to the record evidence.” The decision will add a bearish undertone to an already oversupplied marketplace, save for D3 credits.

December total RIN generation came in at a record 2.17 billion credits, up 9% from the previous month when total RIN generation reached just over 2.00 billion credits.

D4 generation reached a record 840 million credits, up 24% from the previous month and surpassing the previous record of 751 million credits set in May 2023 by 12%. Domestic renewable diesel production accounted for 54% of total D4 output, up from 49.5% the month prior and 47% in October. Foreign renewable diesel made up 9.7% of total D4 generation, down from 11% the month prior. Domestic and imported biodiesel accounted for 35% of the month’s share, down from 39% the month prior and 41% in October. Just 3.8 million D4 credits were generated across domestic and foreign SAF production, accounting for less than one percent of the month’s share.

The EPA received four new SRE petitions for 2023 and two new petitions for 2022, bringing the total pending to eight.

The EPA denied 26 small refinery exemptions covering the 2016-2018 and 2021-2023 compliance years on July 14. The move was consistent with the EPA’s blanket SRE denials under the Biden Administration. The two remaining SREs are for the 2018 compliance year.

In February, United Refining was denied its SRE hardship waiver by the Third Circuit court, a move which would lead to additional demand to the marketplace. Trade organization Growth Energy entered comments in support of enforcing SREs in its case against the EPA. A full denial of all SREs would represent more than 1.6 billion RINs.

Prior to this, the approval by a federal court of a SRE for Calumet Special Products 30,000 b/d refinery in Montana provided bearish undertones to RIN markets.

SREs were carved out in the Renewable Fuel Standard (RFS) for refiners producing 75,000 b/d or less which could prove compliance with the RFS—i.e., purchasing RINs—resulted “undue economic hardship.”

The EPA retroactively overturned 69 Trump-Era SREs starting in April of last year by denying 31 SRE waivers for 2018 and then denying all SRE petitions for 2016 through 2020. Denying SREs is bullish for RINs markets as refiners must enter the marketplace to purchase RINs to cover compliance obligations which were originally waived.

A court ruling earlier this year halted compliance obligations for two refineries with existing SRE petitions taking issue with the retroactive nature of the SRE denial.

Notes from the court were strongly in favor of granting the SREs, as the court made it clear it intends to handle SREs as originally intended by the RFS—i.e., waive RFS compliance if undue hardship can be demonstrated—and to allow waivers which were issued in an “unlawful retroactive application.”

On June 21, 2023, the EPA issued a historic ruling establishing the demand curve for renewable fuel use for 2023-2025. This marks the crucial expansion years for the rapidly growing renewable diesel (RD) and sustainable aviation fuel (SAF) industry and fell well short of current and future production, dealing a blow to RD, SAF and BD industries.

The ‘Set Rule’ greatly underestimated the impact of surging renewable diesel growth, with the decision driven primarily by concerns over feedstock supply. In a glimmer of hope for the renewable diesel industry, the EPA left the door open for adjustments to the final ruling by taking into consideration a wide-ranging list of indicators.

LCFS Pricing

California Low Carbon Fuel Standard (LCFS) credit markets remained bearish as another record quarterly build in unused credits spurred selling.

Prompt credits shed $2.7/t, or 4.3%, to $60.00/t week-over-week. Losses were more muted along the forward curve.

The forward structure showed a $2.00/t contango heading into December 2024.

On December 19, California’s Air Resources Board (CARB) released a preliminary LCFS proposal laying out amendments which nearly mirrored those in the Standardized Regulatory Impact Assessment released in September.

CARB proposed a 30% reduction in carbon intensity by 2030, including a 5% step-down in 2025. This marks a 50% increase in carbon targets over the original 20% reduction target for 2030.

Reductions increase to 90% by 2045 compared to a 2010 baseline.

The proposal contained an automatic acceleration mechanism (AAM) which would advance stringency for a given year when unused credits more than triple average deficit generation by advancing the carbon reduction target by two years.

Amendments included eliminating the exemption for intrastate jet fuel beginning in 2028 and new tracking requirements for crop-based and forestry-based feedstocks to their point of origin. CARB expects to kick off the required 45-day public comment period in January, with a public hearing set for March 21, 2024.

Prior to this proposal the prompt market had been in a choppy holding pattern since early May yet initiated a material downtrend starting in early June.

LCFS strength had been driven by trader buying and strength in futures markets as the credits become more attractive options ahead of CARB’s more stringent scoping plan.

Buying quickly turned to selling once the workshops concluded as traders became disillusioned with the timeline for the rulemaking and deemed current measures as not stringent enough to deal with supply overhang.

LCFS prices add to margin value for product intended for California, which sets the clearing price for RD fuel in the US and Canada as California RD represents the maximum achievable price for the fuel. California consumes roughly +70% of RD produced in the US for this reason, while additional barrels are sent to Oregon which also has a LCFS program in place. Washington state credits have begun trading, with back-half 2024 WCFS credits valued around $105/t.

Final Notes

Renewable diesel and biodiesel margins reflect a complex interplay between conventional fuels, renewable feedstocks, logistics, environmental credits, and regulatory momentum. With at least 1.8 billion gallons of additional RD capacity slated to come online this year, the need for protection from margin erosion is paramount.

Hedging provides this insurance.

At the same time, established facilities conducting turnaround maintenance can benefit from locking in margins and feedstock costs. Less sophisticated facilities—for example, producers equipped to run only one or two high-cost feedstocks and lacking prime market access—stand to benefit most from AEGIS hedging and advisory functions by achieving the best price possible for their product alongside feedstock optimization strategies.

Renewable diesel and sustainable aviation fuel markets remain in revolutionary growth mode. The US Energy Information Agency projected RD capacity could more than double through 2025.

While returns narrow RD and SAF remain the highest returning products in the renewable space, rapid growth and regulatory changes will drive perpetual volatility.

AEGIS is here to help harness volatility to lock in predictable gains and prevent losses through innovative hedging strategies.

Important Disclosure: Indicative prices are provided for information purposes only and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee of the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as "edge," "advantage," "opportunity," "believe," or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.