Latest Insight

Last Look: Oil snaps its two-week losing streak, finishing $1.63 higher this week

The development of sustainable aviation fuel (SAF) in the US hinges on which lifecycle assessment (LCA) model will be adopted by the US Treasury Department to calculate the emissions reductions of SAF. The outcome will determine the value of lucrative tax credits earned by SAF, as well as the eligibility of alcohol-to-jet pathways.

To be eligible for the 45Z Clean Fuel Production Credit (CFPC), the IRA stipulates SAF must reduce greenhouse gas (GHG) emissions by 50% in accordance with the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) adopted by the International Civil Aviation Organization (ICAO), or “any similar methodology”, leaving the door open for alternatives.

Stakeholders and policymakers alike have urged the US Treasury to adopt the Greenhouse Gases, Regulated Emissions, and Energy Use in Transportation (GREET) model developed by the Department of Energy’s Argonne National Laboratory to determine credit eligibility for SAF.

The momentum of support behind the adoption of the GREET model has built rapidly since this summer and seems to have reached a crescendo this month as the deadline for year-end guidance looms.

In an open letter to Treasury Secretary, Janet Yellen, earlier this month, 70 industry stakeholders, including airlines, explained that the ability to attract investment to build the US SAF industry depends on how the program determines credit eligibility and valuation. The letter builds on several bipartisan bills, including the Farm to Fly Act introduced as recently as November 7.

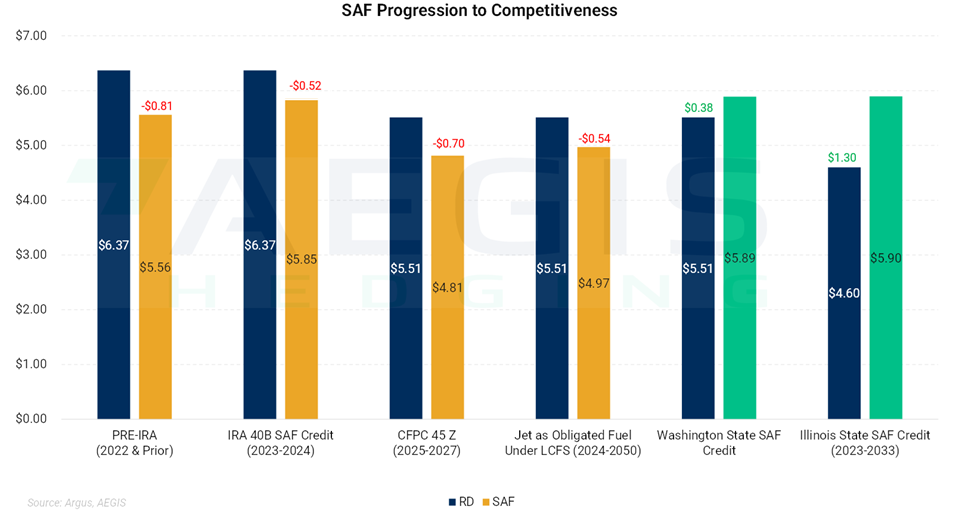

The competitive landscape for SAF is currently dictated by a complex mix of state and federal credits alongside the respective spot diesel and jet pricing. The various inputs determine the returns for producing SAF relative to producing renewable diesel (RD).

SAF production is more costly relative to RD, requiring greater hydrogen inputs and longer processing times which wears on expensive equipment like catalysts. SAF also has a greater yield loss relative to RD.

Given the significant disadvantages to producing SAF, few standalone SAF production facilities exist in the US at this time and most renewable diesel producers generate small volumes of SAF as part of normal operations. Yet changes to federal and state incentives, alongside state-based SAF credits, are poised to alter the economics dictating SAF production.

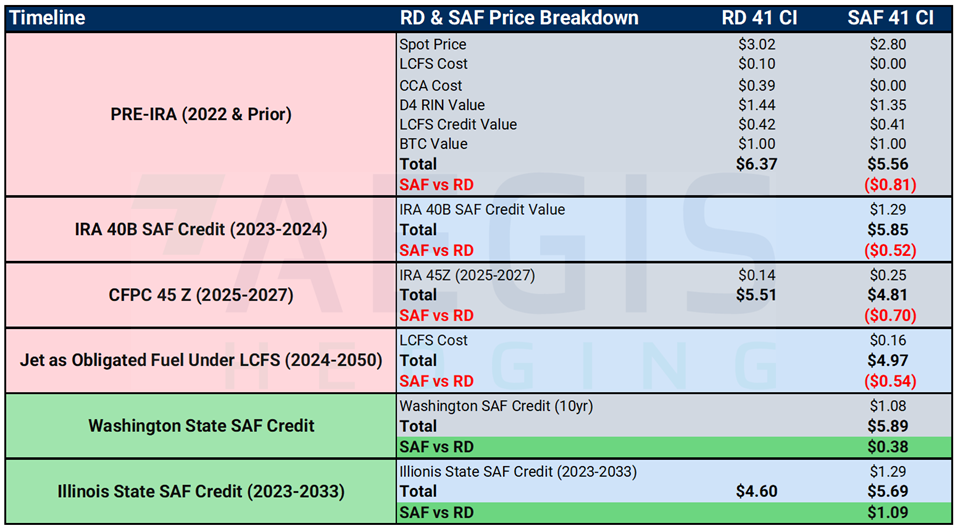

The current makeup of RD and SAF pricing includes the relative spot diesel and jet prices, the cost for diesel incurred under the California Low Carbon Fuel Standard (LCFS), and cap and trade program. Value from federal credits come in the form of the D4 biomass-based diesel RIN and the $1.00/gallon Blenders’ Tax Credit (BTC). Renewable fuels generated California LCFS credit value based on their carbon intensity (CI) relative to the petroleum-based fuels they displace.

To make an equal comparison between RD and SAF, the prevailing CI score for both fuels observed for the last four quarters under the California LCFS was averaged and rounded to 41 CI.

The breakdown for each fuel can be seen in the table below:

Source: Argus Pricing as of 11/09/23, AEGIS

Starting in 2023, SAF became eligible for the $1.25/gallon 40B SAF credit under the IRA, replacing the $1.00/gallon, 40A Blenders’ Tax Credit. The 40B credit is eligible for an additional $0.01/gallon for each percent reduction in GHG emissions that exceeds 50% up to $0.50/gallon for a total maximum value of $1.75/gallon.

Under the 40B, 41 CI SAF is eligible for $1.29/gallon of credit value as its GHG emissions reduction is compared to a baseline of 89 CI for jet fuel. The 40B narrows the gap from the pre-IRA pricing framework by $0.29/gallon for SAF relative to 41 CI RD in California.

Starting in 2024, jet fuel is set to become an obligated fuel under the current, proposed California LCFS scoping plan. This would add an LCFS cost to petroleum-based jet fuel in California, making SAF $0.16/gallon more competitive relative to renewable diesel. During the year 2024, this would narrow the gap between SAF and RD to just $0.38/gallon for a 41 CI fuel.

In 2025, SAF loses the 40B credit at which point both RD and SAF become eligible for the 45Z Clean Fuel Production Credit. RD can gain a maximum credit value of $1.00/gallon multiplied by its emissions rate, while SAF can earn a maximum value of $1.75/gallon. A CI score of 41 equates to an emissions rate of 0.14 under the IRA, generating $0.14/gallon for RD and $0.25/gallon for SAF.

Note that the lower 45Z credit value relative to the BTC drives down the cost of both fuels. This is because the BTC does not account for GHG reductions, while the 45Z is an emission-based valuation. The lowest CI pathway currently producing SAF in the US would generate a 45Z value of $1.17/gallon, with the lowest CI RD pathway earning $0.67/gallon.

Outside of increasing competitiveness through lower CI scores, SAF can outcompete RD in states with standalone SAF credits. Washington State passed a $1.00/gallon SAF credit which mandates a $0.02/gallon increase for every additional percent reduction beyond 50% not to exceed a total of $2.00/gallon. Coupled with the state’s own Clean Fuel Standard credits, 41 CI SAF can outcompete RD by $0.38/gallon with the $1.08/gallon state credit bridging the gap.

Illinois is currently the most lucrative state in which to consume SAF, even without a LCFS policy in place. The state’s SAF credit of $1.50/gallon is eligible to airlines instead of producers. At current pricing, SAF outcompetes RD in Illinois by $1.30/gallon. The Illinois SAF credit will be in place through June 1, 2033, and will only be eligible for SAF produced using domestic feedstocks starting in June 2028.

GREET & The Path to Alcohol-to-Jet

The adoption of the GREET model for determining the emissions reductions of SAF is of particular importance for ethanol-to-jet (ETJ) adoption. Utilizing corn-based ethanol, ETJ would be a boon for US farmers and airlines alike, opening the door for high-value, drop-in SAF to be produced using abundant feedstock and existing infrastructure.

Increased production of ATJ SAF would alleviate demand for conventional renewable feedstocks such as fats, oils, and greases (FOGs). The move would also bolster the US ethanol industry facing saturated federal blending limits and waning gasoline demand.

The adoption of the GREET model would serve to lock in lifecycle emissions rates for stakeholders and investors at a time when the emissions benefits of corn-based ethanol are increasingly being called into question. The EPA’s public advisory committee, Science Advisory Board (SAB), report dated September 29, 2023, questioned if corn starch ethanol reduces GHG emissions by 80% relative to gasoline. The SAB report builds on a vigorous scientific and academic debate which has not gone unnoticed by environmentalists.

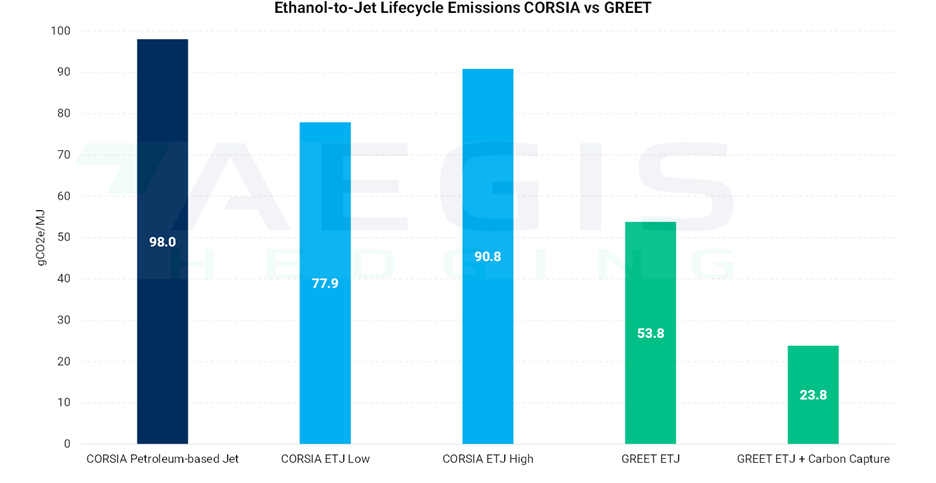

The implications for ETJ SAF are highlighted in the graph below. Recall that fuels with a CI score greater than 50 gC02e/MJ are not eligible for the 45Z CFPC.

The current scores under both CORSIA and GREET would render ETJ ineligible for the CFPC. Yet by coupling carbon capture under the GREET model, ETJ could yield a CI score of 23.8, making it eligible for nearly $0.88/gallon of CFPC. This would make ETJ cost-competitive relative to renewable diesel as well as some SAF pathways. Additional GHG reductions under GREET may also be achieved through crop and soil management.

Should ETJ prove cost competitive, the US SAF industry could see truly revolutionary growth starting in 2025 as the US ethanol industry drives surplus production toward aviation use. Cheap and abundant feedstock should insulate ETJ from feedstock constraints seen elsewhere. Ethanol capacity could increasingly shift toward ETJ as US gasoline consumption dwindles.

AEGIS sees near-universal support for the adoption of the GREET model among a variety of stakeholders and policymakers, with the only opposition originating from climate activist corners.

Some of the price and regulatory risk in the development of the renewable fuels markets is controllable through hedging or pre-selling. Other risks require constant monitoring of pending changes to regulations and programs.

AEGIS can help with both - Get Started

Important Disclosure: Indicative prices are provided for information purposes only and do not represent a commitment from AEGIS Hedging Solutions LLC ("Aegis") to assist any client to transact at those prices, or at any price, in the future. Aegis makes no guarantee of the accuracy or completeness of such information. Aegis and/or its trading principals do not offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program. Certain information in this presentation may constitute forward-looking statements, which can be identified by the use of forward-looking terminology such as "edge," "advantage," "opportunity," "believe," or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.